A storm rolls through on Friday night. By Monday morning, your desk adjusters are buried, voicemail is stacked, policyholders want answers, and managers are already asking for reserve accuracy, cycle time updates, and field availability. That’s the moment many carriers stop thinking about insurance TPA companies as a procurement category and start seeing them for what they are: operational capacity on demand.

A good TPA doesn’t just take work off your plate. It gives your claims operation a way to stay functional when volume spikes, coverage questions get messy, and field coordination starts breaking down. A weak TPA does the opposite. It adds handoffs, clouds accountability, and exposes every weak point in your vendor network.

That difference matters more than most buying teams admit. In property claims, especially after severe weather, a TPA is only as strong as the ecosystem behind it. If the field inspector is late, the photo package is thin, or the reporting doesn’t map cleanly into the claim file, the TPA’s dashboard won’t save you. True value sits at the intersection of process, technology, and field execution.

What Are Insurance TPA Companies

When claim volume is predictable, internal teams can usually keep pace. The trouble starts when volume stops being predictable. Catastrophe events, regional storms, staffing gaps, and seasonal surges can overwhelm even disciplined claims departments.

That’s where insurance TPA companies come in. A third-party administrator, or TPA, is an outside partner that handles operational functions insurers or plan sponsors would otherwise manage internally. In claims, that can include intake, triage, investigation support, field coordination, reporting, documentation management, and other administrative work that keeps files moving.

Why carriers use them

A TPA works like an extension of the carrier’s operation, but without requiring the carrier to permanently build for peak volume. That matters in property and casualty claims, where demand can swing fast and service failures become visible immediately.

The market’s growth reflects that reliance. The global insurance third-party administration market was valued at USD 413.39 billion in 2025 and is projected to reach USD 890.19 billion by 2034, according to Precedence Research's insurance third-party administration market analysis.

That growth makes sense from an operations standpoint. Carriers need flexible handling capacity, faster administrative throughput, and more reliable execution under regulatory pressure. TPAs fill that gap when they’re well selected and properly managed.

What a TPA is and what it isn't

A common mistake is treating a TPA like a staffing vendor. That’s too narrow.

A strong TPA should provide:

- Process control: intake rules, workflow routing, escalation paths, file status discipline

- Service capacity: overflow handling, field assignment coordination, communication support

- Operational visibility: reporting, file tracking, exception management

- Partner management: oversight of inspectors, adjusters, specialty vendors, and documentation standards

A TPA is not a substitute for carrier judgment. It won’t fix unclear authority limits, weak coverage guidance, or poor claim segmentation. If your internal rules are muddy, outsourcing just exports the confusion.

Practical rule: Use a TPA to extend a disciplined claims model, not to invent one in the middle of a surge.

The strategic shift

The best carriers don’t ask, “What can we outsource?” They ask, “Which parts of this workflow need flexible capacity, tighter execution, and better field coordination?”

That shift changes the relationship. A TPA stops being a back-office vendor and becomes part of your claims delivery model. In high-volume property work, that’s often the only way to protect service levels without building permanent overhead for the worst week of the year.

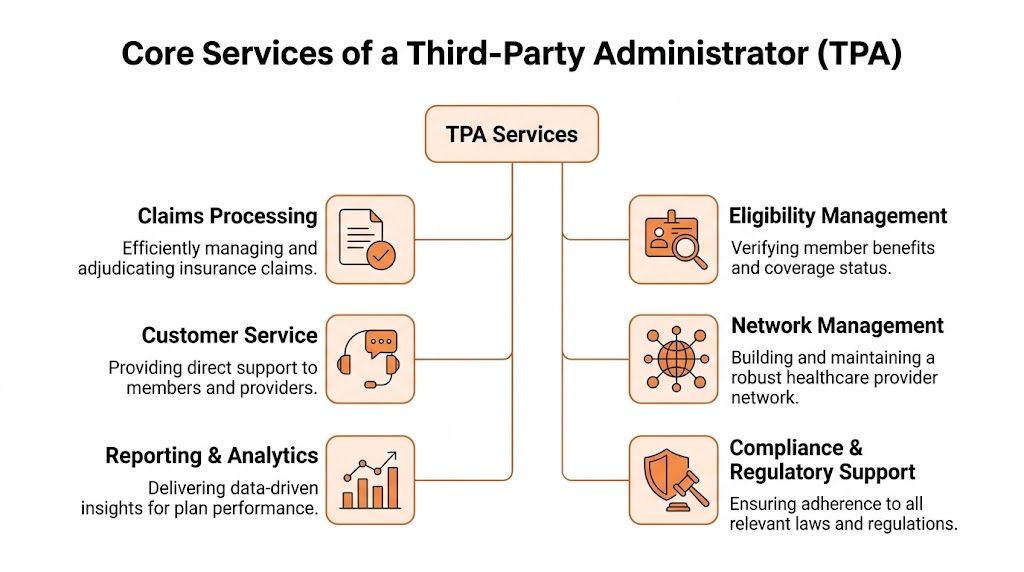

Core Services of a Third-Party Administrator

Think of a TPA as an external operations department. Not a call center. Not just a claim processor. An operations unit that can absorb workflow, enforce handling standards, and coordinate multiple moving parts without forcing the carrier to add permanent internal staff.

Claims administration

This is the most visible function. In practice, it often starts at first notice and continues through investigation support, status reporting, documentation review, and payment-related administration depending on the engagement model.

For property claims, the operational steps usually include:

- FNOL intake and setup: loss details enter the system, policy data is matched, and the claim is routed.

- Assignment management: desk adjusters, independent adjusters, or field vendors are deployed based on geography, severity, or claim type.

- Documentation control: photos, scope notes, invoices, estimates, and insured communications are gathered and tracked.

- Status reporting: carriers receive file updates, exceptions, and aging visibility.

- Resolution support: the TPA helps move the file toward a decision, settlement, or next action.

Process discipline is paramount. Fast assignment means little if the TPA allows inconsistent file notes, duplicate contact attempts, or weak follow-up.

Administrative support beyond claim files

Some TPAs also handle policy administration, billing support, member servicing, provider support, and related back-office functions. The exact scope depends on line of business and contract structure.

A few large players regularly appear in market coverage, including Sedgwick, Broadspire, Crawford & Company, Gallagher Bassett, and CGI. Their breadth is useful context, but buyers should focus less on brand familiarity and more on execution fit.

If your operation depends on field-ready documentation, practical workflow discipline matters more than broad service menus. Even something as basic as maintenance-related operational reliability has an analogy in claims. Small process failures upstream create expensive delays downstream.

Customer and provider support

A TPA often becomes the voice the claimant or service partner hears first. That can help or hurt.

Strong support teams do a few things well:

- Set expectations early: they tell the insured what happens next and when

- Route questions correctly: they don’t let simple service questions sit in adjuster queues

- Protect file momentum: they document every interaction in a way the next handler can use

- Reduce repeat contacts: they close information gaps before those gaps become complaints

Weak support creates claim drag. You see it in missed appointments, repeated calls, unclear responsibilities, and desk adjusters spending time reconstructing conversations that should already be in the file.

The file should tell the story without requiring three follow-up emails and a phone call to understand what happened.

Compliance and reporting

This area gets less attention during the sales process than it should. TPAs don’t just process work. They create records that may later support audits, coverage decisions, litigation defense, or regulatory review.

That means the TPA’s reporting standards have to be usable, not just available. A polished dashboard that doesn’t show aging by exception type or vendor performance by assignment category won’t help operations leaders run the book.

Common fee structures

Fee models vary widely, and that’s one reason TPA comparisons can get messy. In the market, you’ll commonly see arrangements such as:

- Per-claim fees: useful when volume fluctuates and scope is tightly defined

- PEPM structures: common in health-plan administration

- Hybrid pricing: administrative base fees plus charges for specialty services or overflow handling

The cheapest model often becomes the most expensive if rework, leakage, or vendor churn grows underneath it. Price only makes sense when paired with service definitions, escalation rules, and audit rights.

The Strategic Benefits of Partnering with a TPA

The business case for a TPA gets stronger when you stop viewing it as outsourced labor and start viewing it as claims capacity with operating structure.

Scalability without permanent expansion

The clearest benefit shows up during surge conditions. TPAs can absorb overflow when catastrophe volume spikes, helping carriers maintain continuity without hiring permanent staff for short-lived peaks.

According to Engle Martin's overview of what a TPA does in insurance, TPAs enhance scalability by managing high-volume surges from catastrophic events, absorbing overflow to reduce claim cycle times. That same source notes this allows carriers to avoid permanent staff hires and maintain service continuity, while preserving quality.

That’s a practical advantage, not a theoretical one. Internal teams break when every file becomes urgent at once. A TPA gives you a way to spread load before service metrics collapse.

Better use of internal talent

Most carrier teams have highly paid people doing work below their decision level. Desk adjusters chase missing photos. Supervisors triage vendor confusion. Managers reconstruct status because updates aren’t standardized.

A solid TPA partnership changes that. It moves repeatable administrative work outside the carrier while leaving authority, coverage judgment, and complex negotiation where they belong.

That kind of division of labor usually works best when the carrier remains strict about what must stay internal and what can be standardized externally.

For carriers trying to simplify operational dependencies, even unrelated procurement choices often come down to the same principle: pick solutions that are easy to maintain and practical in the field, much like teams do when selecting high-capacity whole-house filtration components instead of piecing together fragile substitutes.

Specialized expertise matters

Some TPAs know specific claim environments better than a general internal team can. That may include catastrophe intake, complex reporting requirements, multi-state administration, or specialized field coordination.

What matters is whether that expertise is usable inside your workflow. A TPA can have deep bench strength and still fail if its assignment logic is clumsy, its status reporting is late, or its field network can’t handle difficult structures.

Here’s a useful overview of the broader role TPAs can play in scaling insurance operations:

More focus on underwriting and claim judgment

Carriers shouldn’t burn core staff on preventable administrative friction. Their edge sits elsewhere: underwriting discipline, reserving quality, coverage analysis, litigation strategy, fraud detection, and customer retention.

A TPA can create room for that work if the partnership is structured correctly. If it isn’t, the opposite happens. Your team ends up managing the TPA instead of managing claims.

A TPA creates leverage only when its workflow reduces touches for your internal team. If touches go up, you bought complexity, not efficiency.

The strategic win is simple. Use the TPA to absorb variability, standardize repeatable work, and keep your experts focused on decisions that require carrier expertise.

Understanding the Risks and How to Mitigate Them

Most TPA sales conversations lean hard on efficiency. Fair enough. Efficiency is real. But the hidden costs show up in control failures, weak vendor oversight, and data exposure. Those issues don’t always appear in the first thirty days. They show up later, when a file ages badly, a policyholder escalates, or a breach forces everyone into incident mode.

Loss of control over the claim experience

The first risk is operational drift. A carrier thinks it outsourced administration, but what it really outsourced was part of the customer experience. If the TPA communicates poorly, misses service standards, or allows inconsistent file notes, the insured won’t blame the TPA. They’ll blame the carrier.

Mitigation starts with very clear file-handling rules. Don’t settle for broad service language in the contract. Define contact expectations, escalation windows, documentation standards, authority thresholds, and handoff rules in writing.

A few controls help immediately:

- Require file-level standards: every claim should show the same note structure, status cadence, and pending reason discipline.

- Create escalation lanes: severe weather claims, vulnerable customers, and reinspection disputes need named escalation owners.

- Audit interactions: review actual communications, not just dashboard summaries.

- Tie oversight to outcomes: recurring service defects should trigger corrective action, not another vendor meeting.

Cybersecurity and claimant data

The next risk is bigger. TPAs often handle sensitive claimant information, and that creates direct exposure for the carrier if controls are weak.

Insurance Business reviewed the cybersecurity trade-offs in TPA relationships and noted that TPAs can introduce significant cybersecurity risks when handling sensitive claimant data. That analysis points to mitigation steps including SOC 2 compliance, end-to-end encryption, and detailed audit trails.

That shouldn’t live in the legal appendix. It should be part of operational due diligence.

Ask for evidence of:

- SOC reports: and review exceptions, not just the cover page

- Access controls: role-based permissions, login governance, and session management

- Encryption practices: both in transit and at rest

- Audit logs: who viewed, changed, exported, or reassigned claim information

- Incident response rules: including breach notification timing and communication responsibilities

Even simple consumer products are chosen with safety and reliability in mind. Claims vendors should face no lower standard than a buyer would apply to sealed smoke detection equipment used in a protected property environment.

Security review isn't an IT courtesy. It's claims governance.

The ghost network problem

A less discussed risk is the network itself. A TPA may present a broad vendor panel, but broad and usable are not the same thing. Directories get stale. Specialty vendors may no longer serve a region. Field resources may be listed but not practically available for steep roofs, emergency tarping, or rapid-response inspections.

That’s the operational version of a ghost network. On paper, coverage looks strong. In the field, assignments stall.

This problem is easy to miss because dashboards can still look healthy until a surge hits. Then carriers discover that listed capacity wasn’t actual capacity.

How to reduce vendor network risk

Mitigation requires active validation, not trust.

Use a short control set:

| Risk area | Mitigation step |

|---|---|

| Vendor availability | Require periodic network validation by territory and claim type |

| Specialty capability | Confirm which partners can handle steep roofs, tall structures, emergency stabilization, and severe-weather deployment |

| Reporting quality | Audit actual photo packages, notes, and estimate support |

| Assignment speed | Track first-contact and on-site performance by vendor class |

| Data integrity | Verify that field outputs land directly in the claim file without manual re-entry |

The strongest TPA relationships don’t hide these issues. They surface them early and fix them fast.

How to Evaluate and Select the Right TPA Partner

A TPA selection process usually goes wrong in one of two ways. The carrier either buys on brand recognition, or it buys on admin pricing. Neither tells you enough about how the partner will perform when files get messy, volume spikes, and field conditions turn difficult.

The better approach is simple: evaluate the TPA the way you’d evaluate a claims operation. Ask how work gets assigned, how quality gets audited, how exceptions are escalated, and how field outputs become usable claim documentation.

Start with technology that supports decisions

Forget the generic promise of “advanced technology.” Ask what the system does inside a live claim.

You need to know:

- Does the platform support real-time API integration, or does it rely on delayed batch transfers?

- Can field photos, notes, and status changes populate the carrier claim file without manual copying?

- Are adjusters working from one operating view, or switching between siloed portals?

- Can supervisors see exception queues, aging, and vendor bottlenecks in real time?

If the answer is fuzzy, the workflow is probably manual in places that matter. That means more touches, slower decisions, and more avoidable leakage.

Test specialization, not just general capability

Many TPAs can handle routine claim administration. Fewer can support high-friction property claims where inspection quality directly affects coverage decisions, estimate accuracy, and customer satisfaction.

That’s why the hidden question isn’t “Do you handle property claims?” It’s “How do you handle difficult property claims when access, safety, and documentation quality become the main issue?”

A useful due diligence lens comes from Research and Markets' discussion of integration challenges with specialized property inspection partners, which notes that buyers should ask how TPAs select and audit field teams for storm events to ensure safety-focused, photo-documented reports.

That question should be near the top of your scorecard, not buried at the end.

Review the TPA Evaluation Checklist

| Evaluation Category | Key Question to Ask |

|---|---|

| Technology | Do you support real-time API integration with carrier and field systems? |

| Workflow design | How do you route claims by severity, geography, and specialty need? |

| Property expertise | What is your process for storm, tree, and complex structure claims? |

| Field network | How do you select, credential, and audit inspectors and independent adjusters? |

| Quality control | What does a failed photo package or incomplete report trigger operationally? |

| Security | Can you provide current SOC documentation and explain your access controls? |

| Reporting | What reports do supervisors receive daily, weekly, and by exception? |

| Escalation | Who owns surge events, service failures, and customer complaints? |

| Compliance | How do you manage licensing, documentation retention, and audit readiness? |

| Integration | How quickly do field findings become visible to desk adjusters? |

Ask for operational proof

RFP answers are polished. File handling tells the truth.

Ask prospective partners to walk you through:

- A storm claim from intake to inspection assignment

- A claim where field access is delayed

- A reinspection triggered by inadequate first documentation

- A file requiring emergency mitigation coordination

- A service failure and what corrective action looked like

Watch for specifics. Strong operators describe queue logic, role ownership, communication timing, and exception handling. Weak operators default to platform language and broad promises.

If your procurement team wants a useful analogy, the habit is the same one people use when evaluating practical resources and process models in other settings, including straightforward reference materials like effective-people style performance frameworks. You don’t judge by title alone. You judge by whether the system changes behavior.

Don’t ask whether a TPA has a network. Ask whether that network is current, specialized, and accountable.

Focus hard on vendor ecosystem management

This is the area buyers underrate most often. The TPA’s field ecosystem will shape your actual claim outcome more than its marketing language ever will.

Push on details such as:

- Credentialing standards: What qualifies an inspector or adjuster for assignment?

- Territory validation: How often is geographic availability verified?

- Specialty segmentation: Which vendors can handle steep roofs, tall structures, or emergency stabilization?

- Audit frequency: How often are reports, photos, and communication quality reviewed?

- Removal rules: What performance failures lead to probation or offboarding?

A TPA with weak field governance creates hidden cycle time, repeat inspections, and poor desk-adjuster confidence. A TPA with strong field governance becomes a force multiplier.

Integrating TPAs with Field Inspection and Adjusting Partners

The true test of a TPA partnership happens after assignment. Not in the contract. Not in the dashboard demo. In the handoff between claim administration and field execution.

That handoff decides whether the desk adjuster receives a usable inspection package quickly, or spends the next several days chasing missing angles, vague notes, and incomplete status updates.

What good integration looks like

In a well-run model, the workflow is tight.

The claim enters the TPA system. Assignment logic identifies geography, severity, and specialty needs. A qualified field partner gets the order with clear scope instructions, contact expectations, and reporting requirements. The inspector captures photos, measurements, observations, and safety-relevant details in the field using mobile tools. That information flows back into the claim environment without rekeying.

When that works, desk adjusters can act. They don’t have to decode the inspection. They can review it, compare it, reserve it, escalate it, or settle around it.

Where integration usually breaks

Most problems come from one of four places:

- Bad assignment matching: the vendor can cover the zip code but not the claim type

- Loose scoping: the field partner gets a generic order instead of a precise task

- Poor data flow: photos and notes arrive in email fragments or separate systems

- Weak status discipline: nobody knows whether contact was made, access was denied, or tarping is needed

These are not small issues. They shape cycle time and claim confidence from day one.

The field report shouldn’t create a second investigation. It should move the claim toward a decision.

Why specialty capability changes outcomes

Not every property inspection is interchangeable. Steep roofs, tall structures, storm-damaged elevations, and emergency stabilization work require different field skills than standard exterior loss inspections.

That’s why the TPA’s partner ecosystem matters so much. If the network includes properly qualified field resources, the claim can move with one inspection. If it doesn’t, the carrier pays for delay, duplicate handling, or both.

This is also where operational compatibility matters. A field partner may do excellent site work and still be a poor fit if it can’t meet your reporting standard or return information in a format the desk team can use.

For teams thinking about field readiness, the principle is similar to selecting commercial drying equipment used in water damage restoration workflows. Capability on paper is only part of the answer. You also need dependable deployment, fit for purpose, and output that supports the job at hand.

The operating model to aim for

A practical integration model usually includes:

- Clear assignment rules by loss type, severity, and structure complexity

- Standard field instructions so inspectors know exactly what must be documented

- Mobile-first reporting to avoid delay and duplicate entry

- Direct data transfer into the TPA or carrier claim environment

- Closed-loop communication so desk adjusters can request clarification quickly

- Vendor scorecards tied to actual field performance and file usability

That’s how a TPA becomes more than an outsourced admin layer. It becomes a control point that connects claim intake, field investigation, and desk-level decision making into one usable process.

Next Steps for Insurance Carriers

If you’re evaluating insurance TPA companies, start inside your own operation before you start the vendor search. Most carrier frustration with TPAs begins earlier than the contract. It begins with unclear internal expectations.

Run a short claims process audit. Identify where files slow down, where desk adjusters lose time, where field information arrives incomplete, and where customer communication falls apart. Separate volume problems from workflow problems. Those are not the same thing, and they require different solutions.

Then build requirements around the realities of your claim book:

- Which claim types need overflow support

- Which activities should stay under direct carrier control

- What field capabilities are essential

- What reporting and integration standards your teams need

- How you’ll audit quality after launch

The strongest TPA relationships are built around precision. Clear workflows. Clear vendor standards. Clear authority lines. Clear accountability for the field ecosystem that ultimately shapes claim outcomes.

That’s the part many buyers miss. A TPA can add scale, but scale only helps when the partner network behind it is real, specialized, and operationally aligned.

If your team is reviewing field-vendor strategy, surge readiness, or inspection quality in complex property claims, Fox Claims Consultants LLC is a practical resource. Their national property inspection support, steep and tall roof experience, emergency response capability, and documentation-focused field approach make them a strong fit for carriers, TPAs, and adjusters that need dependable on-site execution.

Leave a Reply