A bad temporary housing claim starts the same way. The family is standing in a wet driveway, the roof is open, the power is out, and nobody knows whether they’ll be out of the house for three nights or three months. The desk adjuster needs facts. The homeowner needs a place to sleep. The carrier needs costs controlled before receipts start piling up.

At this point, many temporary housing insurance claims encounter problems. People treat housing as a separate task that begins after the inspection, after the mitigation call, after the emergency response. In practice, those things are tied together from the first day. If the initial condition report is thin, the housing timeline is a guess. If the structure isn’t stabilized, the displacement period often stretches. If nobody sets expectations early, the claim gets more expensive and more frustrating for everyone involved.

Temporary housing is supposed to create order. It gives the insured a workable place to live while the home is unsafe or uninhabitable. But efficient ALE handling isn’t just about booking a hotel or approving a rental. It depends on speed, documentation, and realistic planning from the first inspection forward.

When Disaster Strikes Your Home What Happens Next

The first hours after a fire, storm, or major water loss are noisy. A homeowner is calling family, trying to save what they can, and wondering whether the house is safe. The adjuster is trying to confirm the cause, the scope, and whether the insured can remain in place. Contractors are asking for access. Everyone wants an immediate answer.

A common scene looks like this. A tree comes through the roof at night. Rain follows. The ceiling in two rooms collapses, insulation is soaked, and the HVAC can’t run. The family asks one simple question: can we stay here tonight? That answer drives everything else.

The first decision is habitability

If the home is unsafe, temporary housing becomes the first operational priority, not an afterthought. That doesn’t mean the most expensive option. It means the fastest reasonable option that matches the facts known at that moment.

The right first move is usually straightforward:

- Confirm immediate safety: Can the occupants remain in the structure without health or structural risk?

- Stop further damage: Tarping, water control, board-up, and access restriction are important immediately.

- Create a usable field record: Photos, measurements, room-by-room notes, and clear damage descriptions shape housing duration decisions.

- Open the ALE conversation early: The family needs to know what to save, who approves housing, and what expenses may be reimbursable.

A lot of confusion starts because people hear “temporary housing” and think only of hotels. That’s too narrow. The right placement depends on the damage, the likely repair path, the household size, pets, medical needs, work commute, and whether the displacement looks short or extended.

Order comes from fast facts

Temporary housing works best when the claim team gets solid property information. A rough verbal summary rarely does the job. A documented inspection gives adjusters a baseline for two key decisions: whether the home is presently habitable and how long displacement may reasonably last.

Practical rule: The better the first inspection, the fewer housing surprises you’ll manage later.

Even seemingly small details affect the housing path. A damaged kitchen may push a family into a hotel for a short period. A compromised roof deck, wet insulation, active electrical concerns, or interior contamination can shift the placement decision entirely.

For homeowners trying to piece things together, practical preparation helps. Even something as basic as backup power equipment can matter during storm recovery, and people often search for gear and parts under pressure, including resources like https://foxclaimsconsultants.com/303442/Predator-Generators-420cc-5500-9000W-Fits-Champion-Honda while waiting for next-step guidance.

What happens next should be organized, not improvised. That starts with understanding ALE itself.

Understanding Additional Living Expense Coverage

Additional Living Expense coverage, often called ALE, is the financial bridge between an unlivable home and a temporary place to live. It exists to help the insured maintain a reasonably similar standard of living while covered repairs are underway.

If you’re handling temporary housing insurance claims, that “bridge” idea matters. ALE isn’t a blank check for any living arrangement the family prefers, and it isn’t limited to a bare-bones motel if the displacement will clearly last longer. It is meant to cover the extra cost created by the loss of use.

What usually triggers ALE

ALE generally comes into play when a covered loss makes the home unsafe, unusable, or unsuitable to occupy. In field practice, the trigger question is practical, not theoretical: can this household continue living here safely and functionally while repairs occur?

That decision often turns on facts such as:

- Structural compromise: Open roof sections, unstable ceilings, broken windows, or unsafe floors.

- Utility loss: No power, no water, no sewer function, or unsafe HVAC conditions.

- Health conditions: Smoke residue, soot, water intrusion, contamination, or conditions that make occupancy unreasonable.

- Repair intrusion: Demolition, drying equipment, containment, or reconstruction that prevents normal living.

The policy language controls, but most disputes begin long before anyone reads the full form. They begin when nobody documents the habitability problem clearly.

What ALE usually pays for

ALE typically addresses the increase in living costs caused by displacement. That can include lodging and other necessary expenses tied to being out of the home.

Common categories include:

- Temporary lodging: Hotel stays, short-term rentals, or furnished housing

- Meal overages: Especially when the family no longer has a working kitchen

- Laundry costs: If the temporary location doesn’t have normal laundry access

- Pet-related costs: Boarding or pet-friendly housing premiums when necessary

- Storage or relocation expenses: When contents must be moved out of the repair zone

- Extra transportation costs: If the temporary address changes normal commuting patterns

The right standard is usually reasonableness plus documentation. If the family normally lives in a multi-bedroom home and has children, a cramped single-room hotel may be unsuitable beyond the immediate emergency period. If a less costly option provides similar function, carriers will usually expect that option to be considered.

Limits matter early, not late

One reason temporary housing insurance claims become contentious is that people don’t discuss limits until the claim has already burned through a large portion of available benefits. That’s a management failure.

In the United States, carriers spend significant amounts annually on ALE benefits, and ALE is a major source of claim accuracy issues behind restoration. The same analysis notes that integrated technology can reduce sourcing time by up to 80% and cut loss costs by 12-15% through better placement and limit management, according to Crawford’s review of temporary housing solutions.

A housing placement isn’t “approved and done.” It needs active limit management from day one.

For adjusters, that means discussing likely duration, expected expense categories, and reporting cadence early. For homeowners, it means asking direct questions before booking a property that may be hard to unwind.

What works in real claims

The smoothest ALE files usually follow a few simple habits:

| Claim habit | What it prevents |

|---|---|

| Early habitability decision | Delays in first-night placement |

| Clear lodging approval process | Disputes over unauthorized costs |

| Written expense expectations | Missing or incomplete reimbursement requests |

| Ongoing repair timeline updates | Housing extensions based on guesswork |

Practical tools matter too. During a displacement, people often scramble for access items, keys, and temporary-use equipment. Even a niche item like https://foxclaimsconsultants.com/741459/Camper-Replacement-Key-Cut-To-Your-Key-Code-301-360-30-Day can become relevant when a family is staying in alternate property arrangements or using temporary recreational housing.

ALE works best when everyone treats it as part of claims operations, not an accounting category.

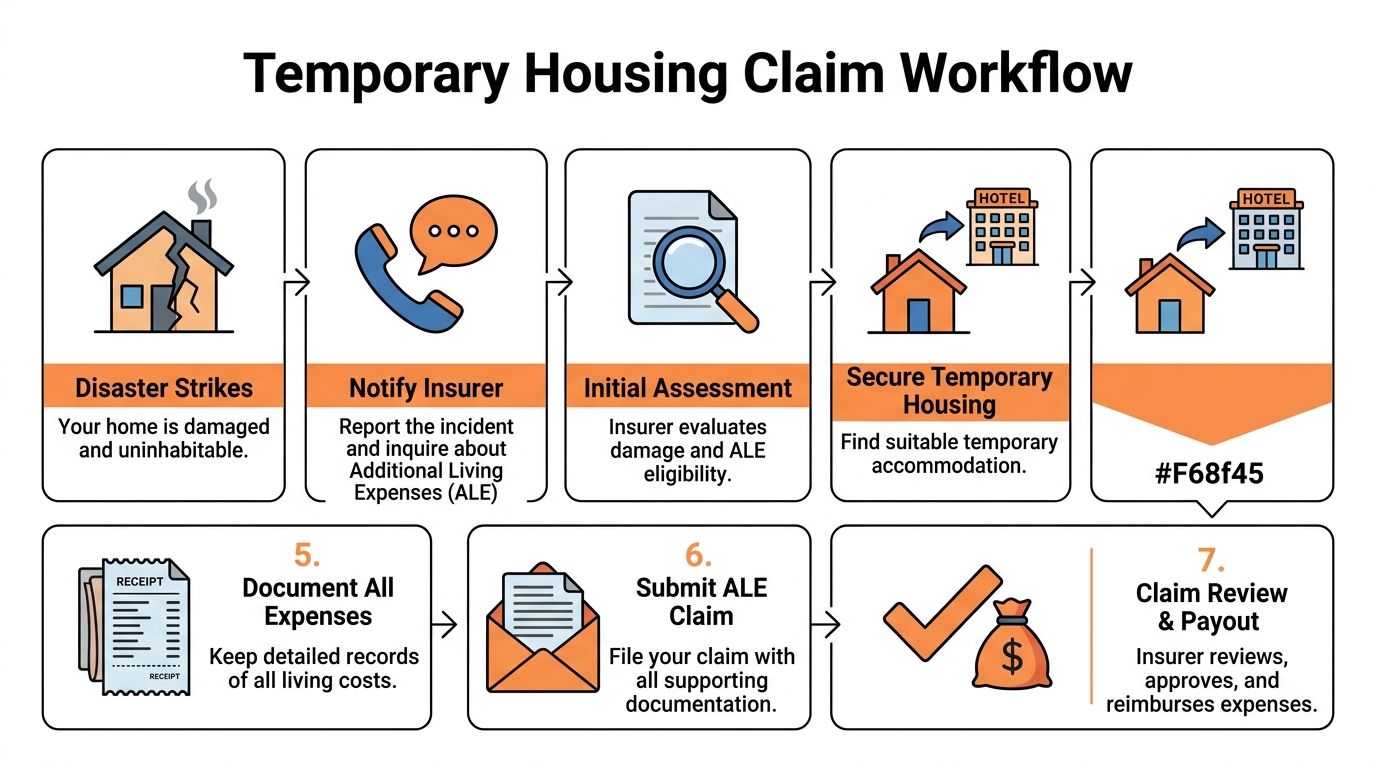

The Temporary Housing Claim Workflow from Start to Finish

A family can lose use of half the house in one night and still avoid a long, expensive displacement if the first inspection is accurate and the emergency work starts fast. I see the opposite more often. A vague habitability call, slow stabilization, and a rushed hotel placement can add weeks of avoidable ALE cost.

First notice and initial assessment

The workflow starts at first notice of loss, but the file usually turns on the first usable property assessment. That inspection should answer four practical questions:

- Is there a potentially covered cause of loss?

- Is the home safe and functional enough for occupancy, in full or in part?

- What emergency stabilization is required immediately?

- What repair path is reasonably likely based on current conditions?

The inspection does not need to be perfect on day one. It does need to be specific. "Home unlivable after storm" does very little for the housing decision. "Tree impact over rear slope, active water intrusion in two rooms, wet insulation, damaged branch circuit in affected area, tarp and moisture control needed today, multiple trades likely" gives the adjuster and housing team something they can use.

That level of detail affects ALE from the start. A good inspection can support partial occupancy, targeted mitigation, or a shorter hotel stay. A weak one pushes everyone toward the safest administrative choice, which is often the most expensive one.

The first 24 to 72 hours

This window drives more housing cost than many teams realize. Emergency tarping, water extraction, board-up, temporary power decisions, and controlled access planning all shape how long the insured stays out of the home. As discussed in this analysis of the temporary housing coordination gap, early coordination between field response and housing placement often breaks down during this period.

That breakdown creates predictable problems. The housing vendor books a unit based on worst-case assumptions. The mitigation team later makes part of the house usable. The repair scope changes after materials are opened up. Then everyone spends time revising approvals instead of controlling the claim.

The practical question is simple. What work done today can reduce or shorten displacement?

Sometimes the answer is full relocation. Sometimes it is far more limited. A fast roof tarp, debris removal, and isolation of one damaged area can preserve bedrooms, kitchen use, or safe access to bathrooms. That changes the housing requirement and the ALE exposure with it.

Housing search and placement

Once habitability is decided, placement should match the household's actual needs and the likely repair timeline. Cost matters, but placement failures create their own costs. Rebooking, extension disputes, school disruption, pet issues, and repeated approvals all add friction to the file.

A sound placement review looks at:

- Number of occupants and sleeping arrangements

- Pets or service animals

- Kitchen access

- Distance to work, school, and medical care

- Mobility or health needs

- Expected repair duration

- Policy limits and approval requirements

Short stays often fit a hotel. Longer repairs usually call for a furnished rental with normal living function. The trade-off is straightforward. Hotels are fast to place, but they become expensive and impractical if the loss drags on. Rentals take more setup, but they often control cost better over time and reduce family disruption.

Alternate living arrangements can also involve mobile units, RVs, or accessory structures. In those placements, practical habitability details matter, including ventilation and utility components such as a side exhaust fan with light for mobile homes or RV temporary housing setups.

Expense tracking and reimbursement

After placement, the claim shifts from housing selection to expense control. At this stage, clean files often start to slip. Verbal approvals get forgotten. Receipts disappear. The insured submits a stack of charges with no category breakdown, and reimbursement slows down.

The fix is straightforward if it starts early:

- Give the insured written instructions

- Set a regular submission schedule, such as weekly or every two weeks

- Separate expenses by category, including lodging, meals, mileage, laundry, pets, storage, and utilities

- Explain whether reimbursement is for total spend or the added cost above normal living expenses

- Name one contact for pre-approval questions

That last point prevents many disputes. Families make fast decisions under stress. If they know who to call before booking, moving, boarding pets, or signing an extended stay agreement, the file stays cleaner.

Ongoing management and extensions

Temporary housing claims rarely stay static. Permits stall. Dry-out reveals hidden damage. Materials go on backorder. Demolition exposes code issues. Good management means updating the housing decision before the lodging term expires, not after.

Here is the review pattern that works:

| Stage | What should happen |

|---|---|

| Early occupancy period | Confirm the placement fits the household and the expense process is understood |

| Repair planning stage | Compare the actual repair plan to the approved housing term |

| Mid-claim review | Update the expected duration using current field conditions, not the original estimate |

| Pre-extension point | Decide early whether to extend, relocate, or end temporary housing |

| Move-back planning | Coordinate final dates, last invoices, and return-home logistics |

The first inspection keeps showing up here. If the original field report understated damage or ignored stabilization options, every extension discussion gets harder to defend. If the inspection was disciplined and the emergency work was documented, later housing decisions are easier to support.

Final reconciliation and move-back

The last phase needs the same discipline as the first. Reconcile the approved housing period, final lodging charges, reimbursable extras, and the actual move-back date. Closeout errors lead to overpayment, underpayment, and avoidable friction.

Homeowners should keep every housing approval and every reimbursement submission. Adjusters should keep the decision trail that explains why occupancy was denied, why placement changed, and how the duration was updated. On a clean ALE file, those records tell the whole story.

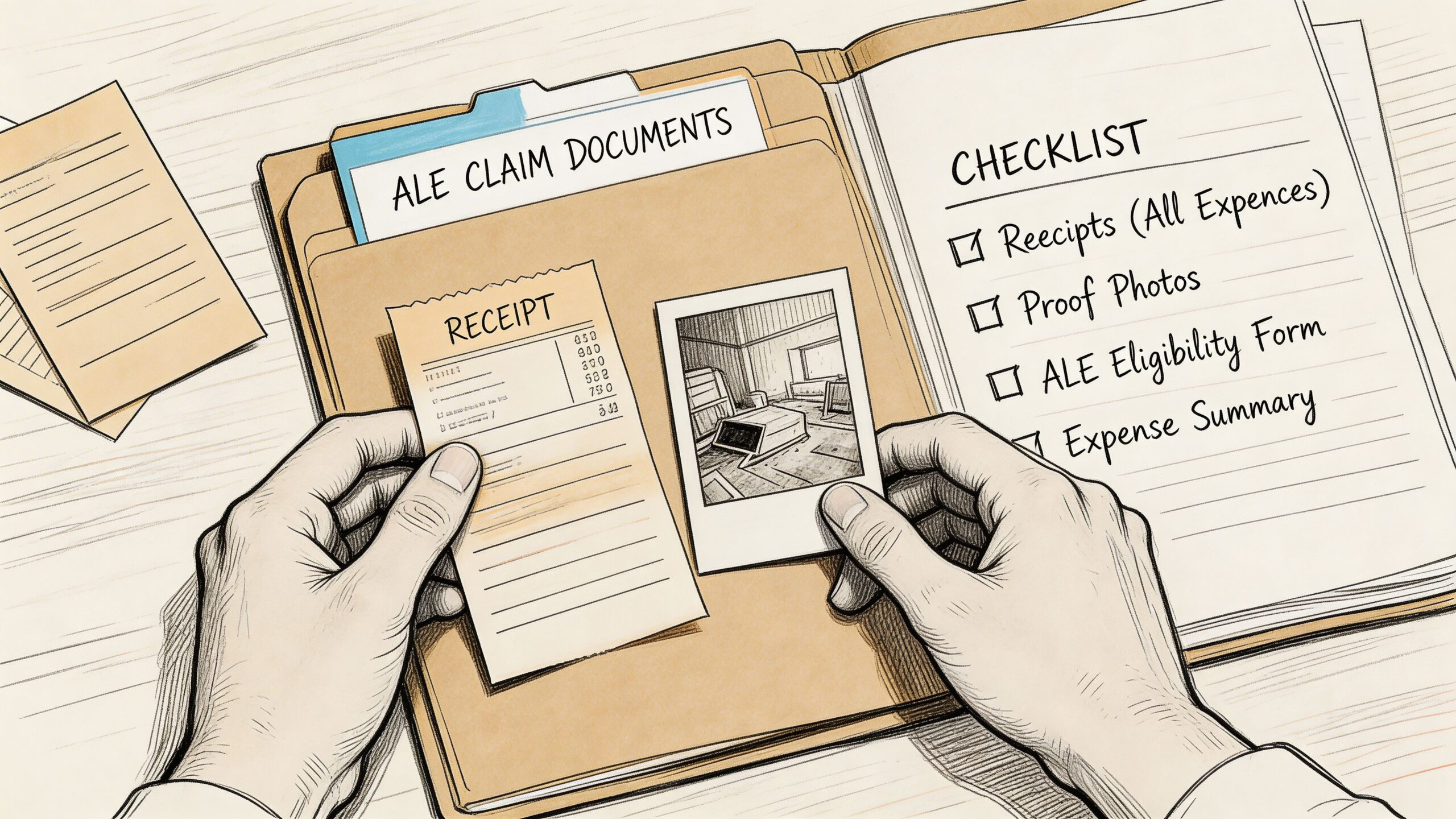

Essential Documentation for Your ALE Claim

The fastest way to delay payment on temporary housing insurance claims is poor documentation. The second fastest is incomplete documentation that looks organized at first glance but doesn’t prove anything important.

A solid ALE file needs two layers of proof. First, proof that the displacement was necessary. Second, proof that the expenses were incurred and were connected to that displacement.

What homeowners should keep from day one

Most insureds save hotel receipts and think that’s enough. It is generally not. The cleaner practice is to build one claim folder and feed it every day.

Keep these items:

- Lodging records: Hotel folios, lease agreements, booking confirmations, payment confirmations

- Meal records: Itemized receipts when the family is eating out because the home or temporary unit lacks a normal kitchen setup

- Laundry costs: Coin laundry, wash-and-fold, or service receipts

- Pet expenses: Boarding invoices or pet fees tied to temporary lodging

- Storage and moving costs: Truck rentals, movers, storage units, packing materials

- Extra travel costs: Mileage logs, fuel records when the temporary location changes routine travel

- Utility changes: New connection charges or unusual temporary utility expenses

- Approval emails or claim notes: If the adjuster approved something, save the written record

A simple spreadsheet helps. Date, vendor, category, amount paid, and short explanation. That one habit resolves a lot of disputes before they start.

What adjusters should verify

An adjuster reviewing ALE shouldn’t look only at the receipt total. The better question is whether the expense fits the displacement facts already documented.

Check these points:

| Documentation item | Why it matters |

|---|---|

| Initial field photos | Supports habitability decision |

| Emergency service records | Shows what was done to prevent further damage |

| Repair timeline updates | Supports length of displacement |

| Lodging invoices | Confirms actual housing cost and dates |

| Expense categorization | Helps separate necessary overages from ordinary living costs |

| Prior approvals | Prevents argument over whether the insured acted with authorization |

The inspection file sets the baseline

Many guides skip this part. The initial property record is not just for scope and estimate. It is the baseline for ALE necessity and duration.

If the inspection file includes room-by-room photos, exterior damage detail, moisture impact notes, safety observations, and emergency stabilization status, the adjuster has something concrete to tie housing decisions to. If it doesn’t, the adjuster is left reconstructing the logic later from invoices and phone calls.

Field note: Good housing documentation starts at the damaged home, not at the hotel front desk.

That’s also why emergency documentation matters. A tarp invoice without supporting photos is weaker than a tarp invoice backed by images showing open roof sections before and after the temporary repair.

How to organize the file so reimbursement moves faster

A practical folder structure works better than a pile of email attachments. Separate the claim into simple buckets:

- Property condition

- Emergency stabilization

- Housing approvals

- Receipts by month

- Repair schedule updates

- Final reconciliation

For physical records, people often use envelopes or small sealable organizers to sort receipts by category and week. Even basic supply solutions like https://foxclaimsconsultants.com/321061/1000-Pack-2×4-Inch-Clear-Plastic-Reclosable-Bags-2-Mil-Thick can help keep tiny paper receipts from disappearing in the first month of displacement.

A quick visual walkthrough can also help insureds understand the discipline needed in a claim file:

Documentation mistakes that create friction

A few errors show up constantly:

- Bundled receipts: One charge covers meals, toiletries, and unrelated purchases with no breakdown.

- No dates: The insured submits a statement with totals but no service dates.

- Missing reason for expense: There’s no explanation for why the cost was necessary.

- Verbal-only approvals: The insured relies on memory of a phone call.

- Late submissions: Costs are held for months, then dropped on the desk adjuster at once.

The cure is simple. Save everything, label it early, and match each cost to the period of displacement.

Real-World Temporary Housing Claim Scenarios

Theory helps. Actual claim patterns help more. Temporary housing insurance claims don’t all look alike, and the right housing choice changes with the likely repair path.

Short displacement after a kitchen fire

A family of four has a cooking fire. The flames are contained to the kitchen, but smoke moves through much of the first floor. The suppression effort leaves water on the floors below, and the power to part of the home is shut off pending electrical review.

The first night solution is a hotel. That makes sense. The duration is still uncertain, the family needs immediate shelter, and the adjuster needs time to determine whether the home can be partially occupied during cleaning and repairs.

Within a few days, the path becomes clearer. The kitchen is unusable, contents cleaning is active, odor remediation is ongoing, and the home isn’t practical for normal family life. The hotel remains suitable because the displacement appears short.

What matters in this scenario:

- Fast habitability call: Nobody delays the first lodging decision while waiting for every estimate.

- Meal overage tracking: The family keeps restaurant receipts because they’ve lost normal cooking access.

- Daily reassessment: If drying and cleaning progress faster than expected, the claim doesn’t automatically stretch.

- Clear end point: Once the home is safe and functional, ALE housing should stop.

This kind of claim usually goes bad only when people overcomplicate it. If the damage is concentrated and the repair path is short, simple lodging and disciplined receipts often solve the issue.

Longer relocation after major storm damage

A different file looks nothing like that. A severe storm causes roof failure, water intrusion across several rooms, insulation damage, and widespread interior repair needs. The family can’t reasonably remain in the home during mitigation and reconstruction. Housing strategy matters more here. A hotel works for the immediate emergency, but it can become inefficient if the repair path clearly points to a longer displacement. Mid-term rentals have become central in these claims. Bookings for stays of 30 days or more surged by 94% in 2023, and those 1-6 month rentals align with typical repair timelines and policyholder preference for stable living arrangements, according to West Coast HomeStays’ review of mid-term rentals in insurance housing.

That shift matches what adjusters see on the ground. A furnished apartment or house often works better than repeated hotel extensions when the family needs kitchen access, separate sleeping areas, and a more stable routine.

The long-displacement scenario brings different decision points:

| Decision point | Better choice in many cases |

|---|---|

| Immediate post-loss shelter | Hotel or short emergency stay |

| Clear multi-month repair path | Furnished mid-term rental |

| Family with pets or children | Housing with more daily function |

| Repeated hotel extensions | Reevaluate before costs drift upward |

A hotel solves urgency. A rental often solves duration.

This kind of file also creates more moving parts. Utility setup, lease terms, cleaning expectations, and extension decisions all need attention. If the repair timeline changes, the housing arrangement may need to change too.

For households using alternate power or water systems during partial occupancy, or trying to bridge gaps in temporary accommodations, practical support items can become part of the broader displacement picture, including equipment such as https://foxclaimsconsultants.com/691370/Pressure-Booster-Pump-100W-Self-Priming-For-RV-Camper-Boat.

What both scenarios teach

The short claim and the long claim share one rule. The housing decision should match the actual repair reality, not wishful thinking. Booking too small for too long causes frustration. Booking too much too early invites avoidable cost disputes.

Good adjusters and organized homeowners both do the same thing here. They revisit the facts as the claim develops and change the housing plan when the facts change.

Avoiding Common Disputes in ALE Claims

Most ALE disputes are predictable. They don’t come out of nowhere. They grow from vague approvals, weak expectation setting, and different assumptions about what “reasonable” means.

A major pressure point is time. While 68-74% of housing placements last fewer than 30 days, claim timelines can still vary from two weeks to two years, and that uncertainty creates major financial and emotional strain for families, as outlined in Catale’s discussion of temporary housing duration uncertainty.

Comparable living doesn’t mean upgraded living

One of the most common arguments starts when the insured says the temporary home should match their old home in every detail, while the carrier applies a tighter view of comparable living standard.

The practical answer sits in the middle. Comparable usually means similar function, not a lifestyle upgrade. If the family previously lived in a three-bedroom home with children and pets, a single room with no cooking space may not be a fair match beyond the immediate emergency. On the other hand, a premium property chosen mainly because it’s nicer than the insured residence will invite scrutiny.

What works:

- Document the household’s actual needs

- Explain why a specific lodging option was selected

- Get approval before locking in higher-cost housing

- Reevaluate when the expected duration changes

The timeline estimate is not a promise

Another recurring dispute starts with an early repair estimate that turns out to be wrong. Homeowners hear “you may be out three weeks” and treat it as a commitment. Adjusters treat it as a rough projection. Months later, the gap becomes personal.

The better approach is plain language. Early timelines are provisional. Demolition can reveal hidden damage. Material delays happen. Scope can expand. The claim team should say that clearly from the beginning.

Early duration estimates should be framed as working projections, not guarantees.

That doesn’t excuse poor communication. If the timeline changes, the insured needs to hear it early, with a reason tied to repair conditions.

Staying with family doesn’t erase the issue

Another misconception is that if the insured stays with relatives, there’s no ALE question left to resolve. That is too simple. The claim may still involve extra food costs, added transportation, pet issues, storage, or contributions to the host household depending on policy terms and documented facts.

The wrong move is assuming informal housing means no paperwork. The right move is documenting the arrangement and clarifying what extra costs are being incurred.

Small communication failures create big claim friction

A few habits reduce disputes dramatically:

- Write approvals down: Don’t rely on memory.

- Set review dates: Revisit the housing plan before the current stay expires.

- Explain denials specifically: “Not approved” isn’t enough. Give the reason.

- Keep the repair team and ALE team aligned: Housing should reflect real construction progress, not outdated assumptions.

Many disputes called “coverage disputes” are really management disputes. The policy matters, but the file handling often decides whether the experience feels fair or chaotic.

Best Practices for a Smooth Temporary Housing Process

A house fire is out by midnight. By morning, the insured is in a hotel, the mitigation crew has tarped the roof, and everyone wants an answer to the same question: how long will temporary housing last? The quality of that answer depends less on the hotel reservation than on what happened in the first 24 to 48 hours. If the initial inspection missed moisture spread, smoke migration, or structural instability, the housing plan will drift, costs will climb, and frustration will follow.

That is the part many ALE guides skip. Temporary housing runs better when the property file is built correctly at the start.

The strongest files use temporary housing as one workstream inside a larger recovery plan. Housing decisions should be updated when new field findings come in, when emergency stabilization changes the condition of the home, and when the repair path becomes clearer. A fast board-up, dry-out, or roof cover can shorten displacement in some losses. In other files, early stabilization reveals that the damage is broader than it first appeared. Either way, better field information leads to better housing decisions.

Technology is starting to improve this process, but only when the file handling is disciplined. Shared inspection photos, timestamped mitigation reports, contractor scheduling updates, and digital housing approvals can keep the adjuster, vendor, and insured aligned without a string of conflicting phone calls. The advantage is speed and visibility. The trade-off is that bad inputs travel fast too. If the first habitability call is poorly supported, a digital system just spreads the error faster.

For carriers and adjusters, the practical standard is simple:

- Tie every housing extension to a documented repair milestone.

- Recheck habitability after mitigation, not just after the original inspection.

- Separate short-term placement from long-term placement decisions.

- Use contractor availability and material lead times realistically, not optimistically.

- Watch for files where housing costs are rising faster than repair progress.

For homeowners, the best long-term move is to stay engaged after placement is approved. Ask what event will end the housing stay. Ask what repair milestone the claim team is watching. If the home becomes partly usable before full completion, ask whether a partial return changes the ALE plan. Those conversations prevent the common late-stage problem where the insured expects one more month and the file supports two more weeks.

Claim closure also needs attention. Once the insured returns home, unresolved ALE issues often shift from lodging to cleanup. Final invoices arrive late. Security deposits are still pending. Utility patterns may need explanation if the family moved back in stages. A good closeout reviews those loose ends before the file is archived.

The files that stay under control usually have one thing in common. The inspection, stabilization, repair schedule, and housing plan were handled as one connected operation, not as separate tasks passed from team to team.

When a property loss needs fast inspection, emergency stabilization, and documentation that supports cleaner housing decisions, Fox Claims Consultants LLC helps carriers, adjusters, and property owners move the claim forward with accurate field reporting, responsive emergency services, and practical support that reduces chaos at the start of the file.

Leave a Reply