A new file lands on your desk. The insured contractor is working a storm loss, the certificate lists Preferred Contractors Insurance Company Risk Retention Group, and nobody on the claim team has dealt with that carrier before. That’s when routine claim handling can stop being routine.

For adjusters, independent inspectors, contractors, and homeowners, the problem usually isn’t the name itself. The problem is what sits behind it. Is this a standard admitted carrier? How should you read the policy? Will claim handling feel normal, or will the file demand tighter documentation and more active expectation setting?

That’s why preferred contractors insurance co deserves a closer look than a quick Google search. On niche carriers, the operational details matter. They affect reservation decisions, payment expectations, report quality, contractor vetting, and how quickly a file moves from first inspection to a defensible outcome. Even small documentation gaps can turn into avoidable friction, especially on steep-roof, storm, and subcontract-heavy losses.

Claims professionals who work high-risk property losses already know the pattern. The harder the roof, the messier the scope, and the more layered the contractor setup, the more valuable clean evidence becomes. That same mindset applies when you’re trying to understand a carrier profile. If you need a good example of how field detail shapes downstream decisions, even a product-focused page like this Schluter Kerdi Board shower niche reference reminds you of a basic truth: specific assemblies, specific conditions, and specific documentation drive better claims outcomes.

An Adjuster's First Look at Preferred Contractors Insurance Co

The first practical takeaway is simple. Preferred Contractors Insurance Company Risk Retention Group, LLC, often shortened to PCIC, is not just another generic construction insurer. It sits in a specialty part of the market, and that changes how adjusters should approach the file from day one.

A claims professional usually encounters PCIC in the same situations where standard workflows start to strain. The contractor may work in roofing, steel erection, or another class that admitted markets often avoid. The loss may involve temporary repairs, subcontracted labor, disputed scope, or a liability question tied to who controlled the work.

What catches an adjuster’s attention first

The name alone causes confusion because it sounds similar to an insurer’s “preferred contractor” program. Those are not the same thing. PCIC is a carrier structure serving contractors. A preferred vendor network is a separate claims-management arrangement used by some insurers to steer repair work.

That distinction matters early because the wrong assumption can send the file in the wrong direction. If you treat a niche contractor carrier like a broad-market admitted insurer, you may under-document the risk issues that matter most later.

Practical rule: When a carrier name is unfamiliar, confirm the structure before you make assumptions about claim handling, oversight, or financial profile.

Why this carrier profile changes file handling

On a PCIC-related file, adjusters should tighten up four things immediately:

- Entity verification: Confirm the exact insured entity, policy period, and whether subcontracted operations are part of the claimed exposure.

- Scope clarity: Separate direct physical damage from liability-driven repair allegations.

- Vendor chain review: Identify who performed the work, who supervised it, and who approved temporary measures.

- Evidence discipline: Lock down photos, roof diagrams, weather context, invoices, and communication logs before positions harden.

That approach doesn’t assume trouble. It prevents preventable trouble.

What Is a Risk Retention Group and Who Is PCIC

A claim comes in from a roofing loss. The insured carries general liability through an entity the desk adjuster has never seen before, and the declarations page says Risk Retention Group. That label changes the first round of questions because carrier structure affects oversight, policy form expectations, and sometimes the pace and posture of claim handling.

A risk retention group, or RRG, is a liability insurer formed to serve members with similar exposure profiles. Under the federal Liability Risk Retention Act framework, these groups were built to insure liability risks that can be difficult or expensive to place in the standard market. For claims professionals, that usually means the insured operates in classes with tighter underwriting, heavier exclusions, or more loss volatility than a typical small contractor account.

That does not make the policy suspect. It does mean the file deserves a closer reading.

PCIC, short for Preferred Contractors Insurance Company Risk Retention Group, writes business for contractor risks that often fall outside the appetite of broad-market carriers. In practical terms, that points adjusters toward accounts with harder-to-place exposures, including subcontract-heavy operations and trades where one job can create a large liability dispute if supervision, scope control, or temporary protection breaks down.

The operational point is straightforward. An RRG is a specialized market solution, not a standard admitted-carrier model. Claims teams should expect tighter scrutiny around who performed the work, how the insured was classified, whether subcontractor activity was contemplated at underwriting, and whether the alleged loss fits the liability grant instead of a warranty or workmanship dispute.

PCIC’s niche focus matters for one more reason. Exposure on contractor liability policies is often measured by gross receipts or a similar work-volume basis rather than by direct payroll alone. That approach reflects a basic claims reality. A contractor can shift large amounts of field activity through subcontractors while keeping payroll light, and the loss exposure still follows the full operation.

For adjusters, homeowners, and contractors, the trade-off is clear. Specialized carriers like PCIC can insure accounts that standard markets may restrict or decline, but that specialization usually comes with closer attention to classifications, endorsements, and operational detail once a claim is reported. That is why early file development matters more on an RRG claim. Fox Claims Consultants helps reduce that risk by locking down scope, contracts, job records, and responsibility lines before the coverage dispute turns into a documentation problem.

Decoding PCIC Financial Strength and AM Best Ratings

A bad loss file exposes carrier differences fast. The claim is large, temp repairs are underway, counsel is circling, and the first practical question is simple. How much confidence should the adjuster place in the insurer’s operating stability while the file is being built?

PCIC’s financial profile deserves that scrutiny because its rating history has moved materially over time, then improved. For claims professionals, that history is not trivia. It affects how aggressively to document causation, how carefully to manage expectations, and how much room there is for delay if the file comes in incomplete.

What a changing rating history means in practice

PCIC’s current position is more favorable than its weaker period. The carrier has also gone through rating pressure and later improvement tied to underwriting performance, as noted earlier in the article.

That combination matters.

A stable or improving outlook can signal better operating discipline, but it does not change the daily claims reality on contractor liability files. Coverage disputes still turn on classification, completed work allegations, subcontractor involvement, and whether the reported damage fits the insuring agreement at all. On a carrier with a mixed financial history, the safer approach is to assume the file will be reviewed closely and to build it that way from day one.

Claims teams should read the rating history as context for process, not as a promise about any single outcome.

What adjusters should do differently on a PCIC file

The practical response is tighter file construction early, before positions harden.

| File condition | Why financial history matters | Better response |

|---|---|---|

| Large claimed exposure | Carriers with prior volatility often review major payments carefully | Tie every repair, invoice, and mitigation charge to dated support |

| Delayed reporting or incomplete notice | Gaps invite extra scrutiny on cause, timing, and scope | Lock down first notice facts, weather chronology, and scene records immediately |

| Subcontractor disputes | Liability can shift quickly if responsibility is not documented | Identify who performed the work, who supervised it, and what contracts say |

| Nervous insured or homeowner | Questions about the carrier can distract from the evidence | Explain the claim process plainly and keep the discussion focused on proof |

That discipline is not theoretical. It is operational. A file with weak dates, loose invoices, and no clear responsibility chain gives every party room to argue.

The opposite is also true. A claim package that ties photos, contracts, job notes, permits, and repair records together gives the carrier less room to slow the adjustment over preventable documentation gaps. Fox often sees this same issue on technical loss files where the dispute turns on exactly what work was done and by whom. Equipment records, site photos, and scope proof matter as much as the policy language. The same habits that help document field tools such as a conduit punch and die kit for hydraulic knockout drivers help document contractor operations when liability is contested.

Read improvement carefully

An improved outlook is a positive sign. It suggests the carrier corrected part of the underwriting instability that created pressure earlier.

For claims handling, that should produce measured confidence, not relaxed standards. Adjusters still need to assume that payment speed and dispute intensity will depend heavily on how well the file answers the obvious questions up front. What happened. When did it happen. Who did the work. What damage is alleged. What part of the claim is covered.

How to explain this to stakeholders

Homeowners and contractors usually ask the wrong question. They ask whether the carrier is good or bad.

A better answer is more precise:

- PCIC has served a specialized contractor segment that standard markets may avoid.

- Its financial history has shown both pressure and later improvement.

- That history does not decide the claim.

- The quality of the documentation still drives the adjustment.

That explanation is fair to the carrier and useful to the insured. It also reflects the operational reality of RRG-related claims. Stronger recent signals help. They do not replace disciplined evidence, clear chronology, and a claim file built for scrutiny.

Inside PCIC General Liability Coverage for High-Risk Trades

A roof crew finishes emergency dry-in work after a storm. Six weeks later, the homeowner reports new interior staining and says the temporary repair failed. That is the type of file where PCIC general liability coverage gets tested in real terms.

PCIC writes for contractor classes that produce harder causation questions and more post-project allegations than standard artisan risks. Adjusters handling these claims need to read past the declarations page and get precise about scope, timing, and who performed each task. On high-risk trade files, coverage often turns on whether the loss stems from the original event, active operations, or completed work that allegedly created new damage.

Where the coverage fight usually starts

The practical issue is rarely the existence of general liability coverage by itself. More often, the dispute is whether the facts fit the policy's insuring agreement after exclusions, subcontractor involvement, and completed-operations issues are applied.

That distinction matters on claims involving roofing, exterior restoration, emergency mitigation, and other trades where temporary measures are common. A tarp, patch, sealant application, or partial dry-in can stabilize the property on day one and still become the center of a liability claim later if water enters again.

Completed-operations exposure is often where the file gets expensive. Once the contractor has left the site, the argument shifts from immediate jobsite conditions to whether the finished or temporary work was defective, whether it caused separate damage, and whether the claimant can prove that sequence with something more than assumptions.

What adjusters need in the file

These claims reward documentation discipline. They punish loose timelines.

A workable file usually includes:

- date-stamped photos showing conditions before and after the contractor's work

- work orders that identify exactly what temporary or permanent repair was authorized

- weather history tied to the reported return of leakage

- notes showing whether employees or subcontractors performed the work

- a damage map that separates original storm impact from later deterioration or alleged repair failure

Files become harder when the record relies on broad statements from the contractor or owner without location-specific proof. "The tarp held" is not enough. "The leak came back" is not enough either. The file needs a chronology that ties each reported symptom to a repair area, a weather event, and a responsible party.

Operational reality on high-risk trade claims

Carrier structure and claim handling discipline intersect. On a specialized carrier file, speed and payment friction are influenced by how cleanly the evidence answers threshold coverage questions. Adjusters who build that record early reduce the room for avoidable disputes. Contractors also protect themselves when their field records show what was inspected, what was repaired, and what was outside their scope.

I tell contractors the same thing I tell claim teams. If the work is trade-specific, the documentation has to be trade-specific too. Even a simple equipment reference, such as this conduit punch and die kit used on assembly-specific field work, makes the larger point. Liability files are stronger when the record reflects the actual tools, tasks, and limits of the job performed.

For homeowners, the takeaway is straightforward. A certificate of insurance does not answer the hard part of the claim. The hard part is proving what work was done, whether that work caused additional damage, and whether the policy responds to that specific theory of loss.

Navigating RRG Risks and Common Policy Pitfalls

The biggest mistake people make with preferred contractors insurance co is assuming that the only issue is whether the contractor has insurance. That’s too shallow. The sharper question is whether the carrier structure, policy language, and repair-control facts create friction later.

Content often diverges into two main paths. One track is about PCIC as an RRG. The other is about preferred contractor programs run by insurers. They sound similar. They create very different risks.

The RRG risk adjusters should not ignore

One structural issue with RRGs like PCIC is heavy reliance on reinsurance. According to Agency Equity’s carrier directory entry for PCIC, that dependence can run at 70-80% of premium, which exposes the carrier to rating volatility. The same source says A.M. Best had placed its B (Fair) rating under review with negative implications, signaling concerns around claims handling stability in a volatile construction market.

That does not mean every claim is destined for delay. It does mean adjusters should treat support and communication discipline as absolutely critical.

What that means in the field

If you know a carrier relies heavily on reinsurance, don’t build the file as if assumptions will carry the day. Build it as if every line item may need to survive a second, harder review.

That means:

- Tight chronology: Loss date, notice date, inspection dates, mitigation dates, and invoice dates should line up cleanly.

- Clear responsibility mapping: Identify insured contractor work versus other trades, especially after emergency stabilization.

- Attachment-ready evidence: Photos should show location, angle, and context. Random close-ups rarely help later.

- Communication preservation: Save emails, texts, approvals, and direction given to or by the contractor.

PCIC is not the same as a preferred vendor network

This distinction saves a lot of confusion. PCIC is an insurance company structure for contractors. A preferred contractor network is an insurer steering policyholders toward selected repair vendors.

Those programs create a different liability question. According to Bordas Law’s analysis of insurer preferred contractors, insurers often present those vendors as independent contractors, but courts may still hold insurers liable if the insurer exercised enough control over the work. The same discussion references a Nebraska case, Williams v. Allstate, involving close pre-contract ties and work guarantees.

That matters because homeowners often say, “The insurer sent this contractor, so the insurer owns the result.” Legally, that isn’t automatic. Factually, control evidence can matter a great deal.

If an insurer selected the vendor, set pricing expectations, approved scope limits, or guaranteed performance, document those facts. Control is rarely proven by a single statement. It’s usually shown through the paper trail.

Common pitfalls that create avoidable disputes

A few patterns show up again and again:

- A homeowner confuses the contractor’s insurer with the homeowner’s insurer’s repair network.

- An adjuster documents physical damage well but fails to preserve communications showing who controlled the repair decision.

- Temporary work gets approved narrowly, then later allegations expand into workmanship and completed-operations issues.

- Nobody separates contractor liability questions from direct first-party property scope until the file is already tense.

Even practical field gear pages such as this 3M half-face respirator product page point back to the same habit good claims people already know. Hazard-sensitive work needs deliberate procedure. Carrier analysis does too.

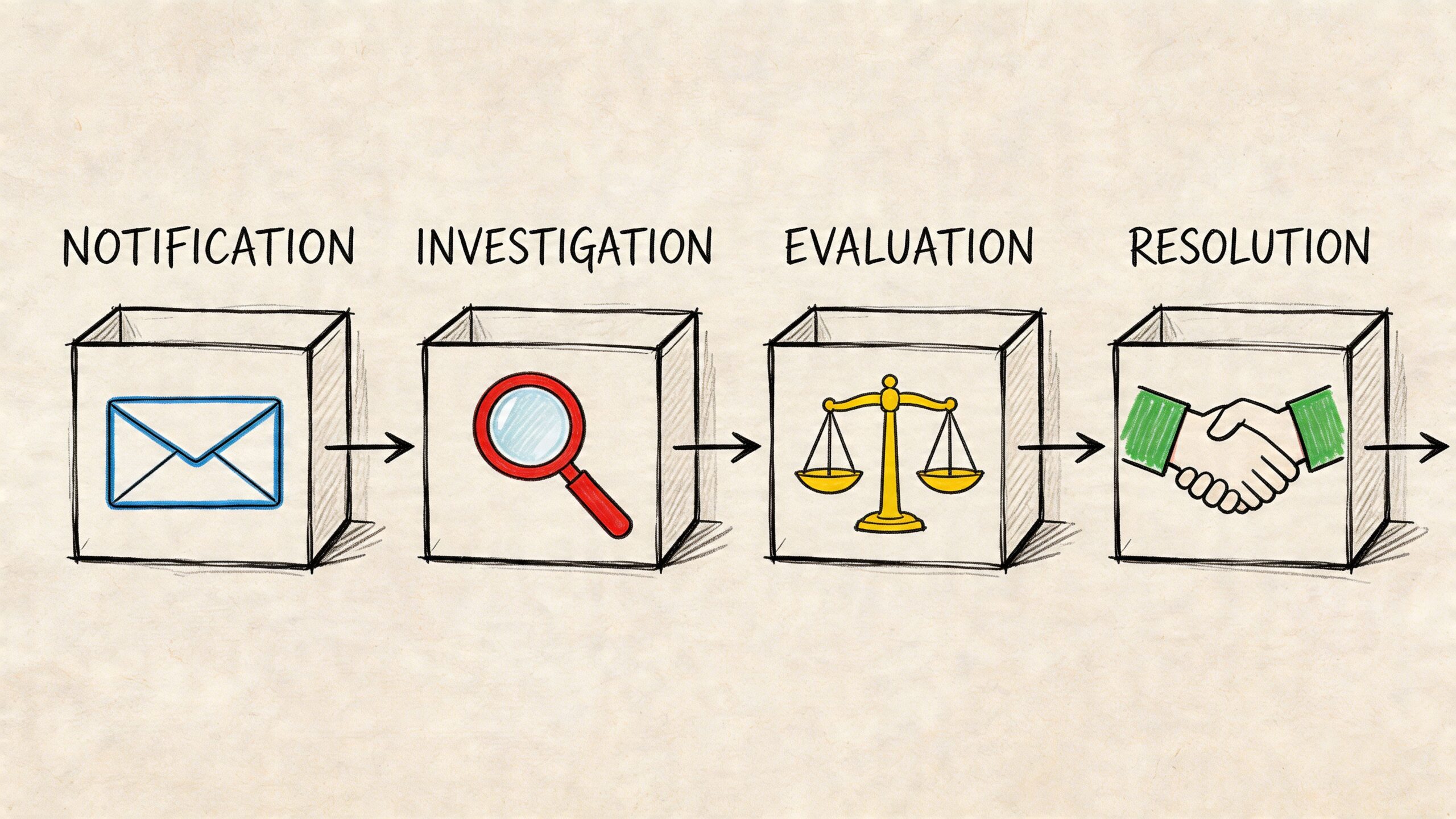

The PCIC Claims Process A Practical Walkthrough

A PCIC claim usually moves best when everyone treats documentation as part of claim handling, not as an afterthought. The process itself is familiar. The margin for vagueness is smaller.

Step one through notice and intake

Start with the basics, but do them thoroughly. Confirm the named insured, date of loss, site address, reporting party, and a short statement of what allegedly happened. If the claim involves storm work or a temporary repair, identify that immediately.

For homeowners and contractors, the most common early mistake is reporting the event in broad language. “Roof leak after the storm” is not enough. A better report states when the damage was discovered, what emergency work was performed, who performed it, and what changed afterward.

Investigation and field proof

The investigation phase is where a file either gets clearer or starts to drift. Field documentation should connect exterior conditions, interior damage, repair attempts, and contractor involvement in one consistent record.

Use a simple evidence stack:

- Photos with context: Wide shots, elevation references, and close-ups that relate back to a specific area.

- Document trail: Contract, work authorization, temporary repair invoice, and any scope approvals.

- Role clarity: Which entity inspected, which entity repaired, and which entity supervised.

- Damage separation: Original loss damage versus later allegations of poor workmanship or incomplete repair.

A page like this aluminum manifest document holder listing may seem far removed from claims practice, but it points to a habit that matters here. Files move better when documents travel in order and stay accessible.

Evaluation and resolution

By the time the file reaches evaluation, the goal is to make the coverage and damage questions easier, not louder. Adjusters should ask whether the record supports a first-party property payment issue, a contractor liability issue, or both.

Use this quick decision check:

| Question | Why it matters |

|---|---|

| Was there direct physical loss from the reported event? | Establishes the starting point |

| Did temporary repairs alter the damage path or create a new issue? | Frames later allegations |

| Is the dispute about scope, workmanship, causation, or control? | Keeps the analysis focused |

| Do the documents support each claimed cost? | Prevents late invoice fights |

Clean claims files don’t happen because everyone agrees. They happen because the evidence is organized well enough that disagreement has limits.

For contractors, the best move is to report early and preserve records. For homeowners, it’s to keep every communication and avoid paraphrasing repair instructions from memory. For adjusters, it’s to insist on a documented timeline before taking broad positions.

Streamline PCIC Claims with Fox Claims Consultants

PCIC-related claims reward precision. They punish assumptions. That’s especially true on steep roofs, storm damage, tree impacts, temporary repairs, and losses where contractor work and coverage analysis can overlap.

That’s where a specialized inspection partner changes the file trajectory. Fox Claims Consultants LLC supports carriers, adjusters, and policyholders with certified field inspections, ladder assist, storm and tree damage assessments, emergency response, photo-rich reporting, and precise estimating. On niche carrier files, that kind of support does more than fill a gap. It helps reduce ambiguity before ambiguity turns into dispute.

The practical value is straightforward:

- Safer roof access: Difficult structures get inspected with the right field discipline.

- Stronger evidence packages: Reports are built for review, not just for the site visit.

- Better cycle-time control: Clear documentation cuts down on repeated questions.

- Less room for scope drift: Photos, notes, and timelines keep the claim grounded.

For teams handling contractor losses, even a simple field-ready item like these ATG MaxiFlex nitrile-coated gloves points back to the bigger standard. Claims move best when the people on the roof and the people in the file both work with discipline.

When a PCIC claim involves a steep roof, storm damage, temporary repairs, or a file that needs sharper support, Fox Claims Consultants LLC gives adjusters and carriers the field evidence they need to make sound decisions fast. Their national team handles ladder assist, thorough inspections, emergency tarping support, and detailed estimating with clear communication at every step.

Leave a Reply