After a major property loss, things get chaotic. Fast. For insurance carriers and adjusters, trying to document every single damaged item is a monumental task—one that can stall a claim before it even gets started. This is where inventory management consultants come in. They are the specialists who step into the chaos and create a clear, structured process for faster, more accurate settlements.

Why Top Carriers Rely on Inventory Management Consultants

When a home gets hit by a fire, flood, or major storm, the scene is overwhelming. The policyholder is distressed and displaced. The adjuster is facing down a mountain of work, trying to evaluate hundreds—sometimes thousands—of personal items. This is precisely when an inventory consultant proves their worth.

These specialists bring an objective, systematic approach to what is often a highly emotional and disorganized situation. Their job isn’t just to make a list. It’s to create a comprehensive and verifiable inventory of all affected contents, paving the way for accurate valuation and salvage.

Bringing Order to Chaos

An experienced consultant knows exactly what to look for during on-site home inspections. They methodically document items, capturing everything from brand names and model numbers to the specific condition of each piece with detailed notes and photos. This level of detail builds a defensible claim file from the ground up, minimizing the back-and-forth between the carrier and the policyholder.

By taking on the labor-intensive job of inventory creation, these consultants free up the adjuster to concentrate on other critical parts of the claim, like assessing structural damage or analyzing policy coverage. It’s a smart division of labor that gets the entire claim moving forward, faster.

Driving Accuracy and Reducing Claim Cycle Times

A consultant’s expertise has a direct impact on both speed and accuracy. With a professionally prepared inventory in hand, valuation stops being guesswork and becomes a data-driven exercise.

Their role is to provide a clear, unbiased foundation for the contents portion of the claim, ensuring all parties have confidence in the final numbers. That precision helps avoid costly revisions and lengthy negotiations, directly cutting down claim cycle times.

This isn’t just a niche service; it’s a growing standard. The global market for these specialized services is projected to hit $2,813.5 million by 2025, showing just how much carriers are relying on experts to manage complex claims.

Ultimately, bringing in an inventory management consultant is a strategic move. It helps mitigate loss for the carrier, lightens the load for the adjuster, and gives the homeowner a fair, transparent path to getting their life back together.

How Consultants Benefit Different Stakeholders in a Claim

The value of an inventory specialist touches every person involved in the claim. While their primary function is documentation, the ripple effects create a smoother process for carriers, adjusters, and homeowners alike.

| Benefit | Impact for Carriers & Adjusters | Impact for Homeowners |

|---|---|---|

| Expert Documentation | Creates a defensible, detailed claim file. Reduces errors and omissions. | Ensures all damaged items are accounted for, preventing forgotten losses. |

| Increased Efficiency | Frees up adjuster’s time to focus on structural assessments and coverage. | Accelerates the claims process, leading to faster financial recovery. |

| Objective Valuation | Provides an unbiased, data-driven basis for settlement talks. | Builds trust in the process with a transparent and fair valuation. |

| Dispute Reduction | Minimizes back-and-forth negotiations over contents value. | Reduces the stress and conflict often associated with making a claim. |

| Improved Accuracy | Leads to more precise initial settlements, avoiding supplements. | Provides a clear and accurate record for replacement or reimbursement. |

By serving as a neutral third party focused solely on the facts, consultants help align everyone’s expectations and keep the claim moving toward a swift and fair resolution.

Know What You Need Before You Start Looking

Before you even think about picking up the phone to hire an inventory management consultant, you need a crystal-clear picture of what you actually need them to do. Starting the search without a detailed plan is like sending an adjuster into the field blindfolded. It just doesn’t work.

A well-defined Scope of Work (SOW) is the only way to focus your search and set solid expectations from day one. This isn't just paperwork; it's the blueprint for the entire engagement. Without it, you're inviting miscommunication, scope creep, and a partnership that's doomed to fall short. We’ve seen it happen—vague requests lead to vague, unusable reports, especially when the stakes are high on a large property claim.

One Size Does Not Fit All

The scope for a residential flood is a completely different world from a massive commercial fire. The type, scale, and complexity of the loss directly shape the services you need, and your SOW has to reflect that reality.

Let’s look at two very different scenarios:

Residential Flood: Here, the job is often about carefully documenting furniture, electronics, and personal belongings that carry huge sentimental value. The consultant's key role is separating what’s truly a total loss from what can be salvaged, all while navigating water damage and potential mold.

Commercial Fire: This is where complexity skyrockets. The scope will likely involve documenting specialized manufacturing equipment, massive volumes of product stock, and critical business records. The consultant’s work here is foundational to the Business Interruption (BI) portion of the claim.

The whole point is to think through the unique challenges of each claim. That clarity is what ensures you hire a consultant with the right expertise for that specific job, not just any job.

A strong SOW isn't just a task list. It’s a strategic document that aligns the consultant’s work with the claim's specific goals. It protects everyone involved by creating a shared definition of success before a single item is ever tagged.

The Core Services You Must Define

When you're building your SOW, think bigger than just "make an inventory list." A truly comprehensive scope digs into the details of how the work gets done. This level of detail is what separates a passable report from a bulletproof, defensible one.

Your SOW should spell out exactly what you expect in these key areas:

On-Site Documentation: Get specific. What’s the standard for photos—overview shots, close-ups, serial numbers? What’s the protocol for tagging items? How should the pre-loss condition of each item be recorded?

Digital Cataloging: Name the software or platform you want them to use. Define the data fields you need for every single item—like brand, model, age, condition, and links to replacement cost research. Consistency here is non-negotiable.

Valuation and Research: Be clear on what you need. Will the consultant provide Replacement Cost Value (RCV), Actual Cash Value (ACV), or both? Specify which sources they should use for pricing to keep the valuation credible and consistent.

Salvage Management: If there’s potential for salvage, outline the consultant’s role. Are they identifying and separating salvageable goods? Are they coordinating disposal or connecting you with a salvage buyer?

Reporting and Deliverables: Define the finish line. What format does the final report need to be in—a PDF, an editable spreadsheet, or an import file for your claims management system? Set firm deadlines for first drafts and the final submission.

How to Find and Vet Your Ideal Consultant

Once you have a solid Scope of Work, it's time to find the right expert. The best inventory management consultants are rarely just sitting by the phone waiting for a call; you need to know where to look and, more importantly, what to look for. Your goal isn't just to hire a vendor—it's to find a partner whose expertise truly fits the unique, often chaotic world of property claims.

Forget broad internet searches. Start with your trusted professional network. Referrals are gold in this business, so ask your colleagues at other carriers, respected independent adjusting firms, or even the large restoration companies you work with. These are the people who see consultants in action and can vouch for their results. Industry associations for claims professionals are another great place to find pre-vetted service providers.

Building Your Vetting Checklist

With a shortlist in hand, the real work begins. You can't just go with your gut; you need a consistent, repeatable process to evaluate each candidate. This isn't about finding someone you like—it's about finding someone whose work product will stand up under scrutiny.

A simple checklist is your best tool for making an objective decision. Here’s what you need to verify:

- Credentials and Certifications: While there's no single, universal certification for this role, you should look for specific training in contents valuation or a deep history in property claims.

- Direct Property Claims Experience: This is non-negotiable. A consultant who specializes in retail inventory simply won't get the nuances of a smoke-damaged home. Ask them to walk you through case studies similar to the claims you handle.

- Technological Capabilities: What software do they use? You need to ensure their final reports can be delivered in a format that works for you, whether that's a simple spreadsheet or a file that integrates directly with your claims platform.

- References: Always, always check them. Talk to at least two recent clients—preferably other adjusters or carriers—to get an unvarnished opinion on their performance, communication, and overall reliability.

The Interview Questions That Matter

The resume tells you what they've done. The interview tells you how they think. This is your chance to move past the sales pitch and see how a consultant will actually perform on a claim. Ditch the generic questions and get specific to the realities of property loss.

The right interview questions will tell you more than a resume ever could. You're not just hiring a service; you're vetting a partner who will interact with adjusters and distressed policyholders. Their ability to communicate with clarity and empathy is just as important as their technical skill.

Use these questions as a starting point to see how they operate under pressure:

Describe your process for a large-loss residential fire, from the moment you arrive to delivering the final report. What are your first three steps on-site?

This cuts right to their methodology and shows you what they prioritize when they walk onto a loss.How do you handle a disagreement with a policyholder over an item's pre-loss condition or value? Give me a specific example.

This is a test of their people skills and their ability to de-escalate conflict while remaining objective.What’s your typical turnaround time for a final inventory and valuation report on a claim with around 500 line items?

This helps you understand their capacity and set realistic expectations. Accurate estimating services for contents are time-sensitive, and delays here can stall the entire claim.How do you ensure the data you collect is accurate and defensible if a claim goes to appraisal or litigation?

A great consultant understands their work doesn't exist in a vacuum. This question reveals their commitment to creating a bulletproof work product that supports the entire claims process.

You’ve hired a top-notch inventory management consultant. Great. But their real value isn’t just in their expertise—it’s in how seamlessly they fit into your claims process. A skilled expert working in a silo can create more headaches than they solve. Real success comes from a clear, structured plan to plug them into your workflow from the very first day.

It all starts with a kickoff meeting. This is the crucial first step to get the consultant, the adjuster, and the policyholder on the same page. The goal is simple: set clear expectations, map out how everyone will communicate, and agree on a timeline. Skipping this alignment is a recipe for crossed wires and immediate delays.

Defining Roles and Responsibilities

When roles are fuzzy, claims get messy. Everyone involved needs to know exactly what they’re responsible for and how they fit into the bigger picture. We recommend creating a simple responsibility matrix to eliminate any confusion.

- The Adjuster: Stays the primary point of contact for the policyholder and holds the final authority on the settlement. They review the consultant’s findings, check them against the policy, and make the final call.

- The Consultant: Serves as the on-the-ground expert for data collection and valuation. Their job is to build a detailed, objective inventory and provide well-researched values for the adjuster to review.

- The Policyholder: Provides access to the property and any necessary information about the damaged items. They should always direct questions about claim status or coverage to the adjuster, not the consultant.

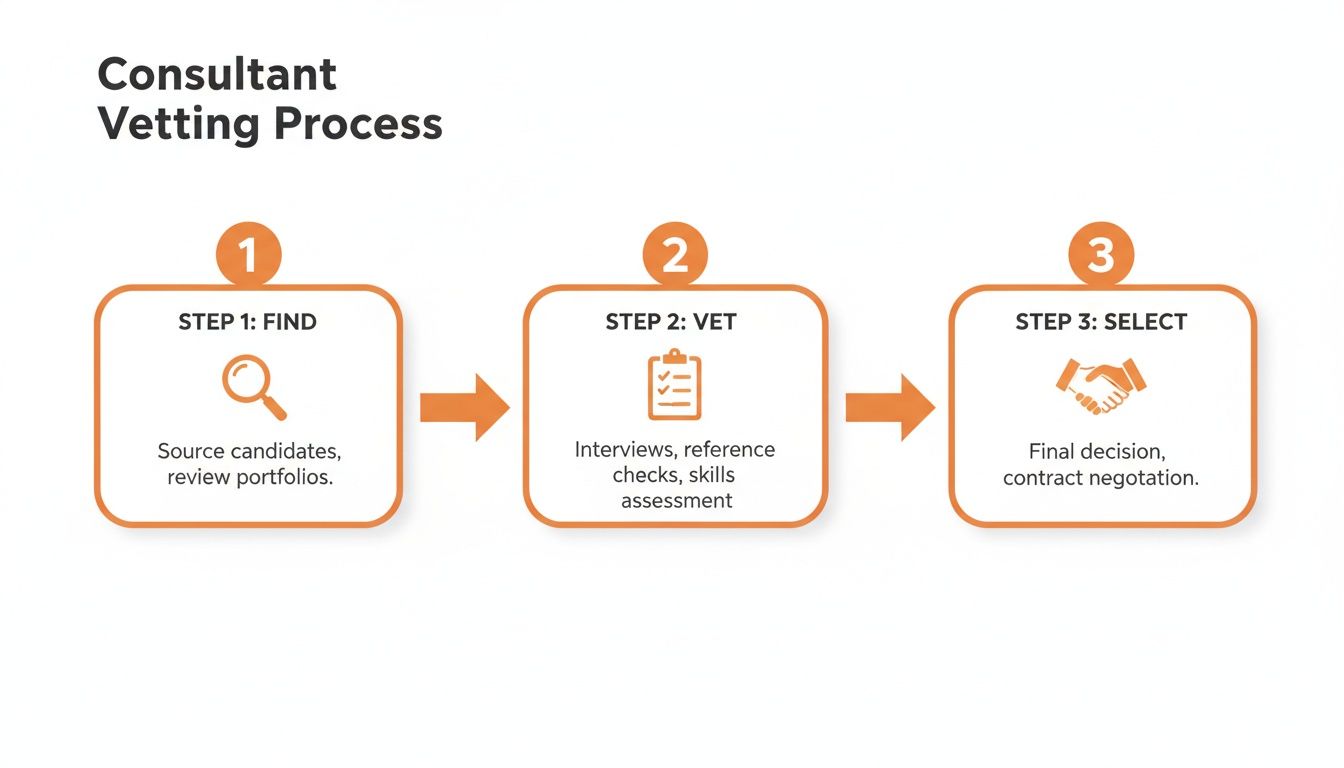

This infographic gives a great high-level view of the first few steps when bringing a new consultant into the fold.

As you can see, finding and vetting the right partner is just the start of building a truly structured and effective partnership.

Establishing Communication and Data Protocols

With roles clearly defined, the next step is to nail down the flow of information. How will the consultant deliver their reports? What does the review process look like? Answering these questions upfront prevents major bottlenecks down the road.

A common friction point we see is handling valuation disputes. For instance, if a policyholder disagrees with the Actual Cash Value (ACV) on a piece of electronics, the path to resolution should already be established. The consultant supplies their research, the adjuster reviews it against the policy, and then the adjuster communicates the final decision. The consultant provides data; the adjuster makes the decision.

The best partnerships treat the consultant like an extension of the claims team, not an outside vendor. This requires transparent data-sharing and communication loops that keep everyone in the know without creating information overload.

To keep everything consistent and accurate, we strongly recommend using a standardized format for all documentation. A solid property inspection report template is a fantastic foundation for creating a custom deliverable that gives you exactly what you need every time.

Finally, set a clear rhythm for updates. A quick weekly check-in call or a summary email is often all it takes to keep the adjuster aware of progress without getting lost in the weeds. This kind of proactive communication means no surprises when the final report arrives, allowing for a smooth and rapid move toward settlement. The goal is a predictable, repeatable workflow that turns expert insights into faster, more accurate claim resolutions.

Measuring Success and Avoiding Common Pitfalls

So, how do you know if bringing in an inventory management consultant is actually paying off? Gut feelings about efficiency won’t cut it. The real answer is in the data.

To see their true impact, you have to track specific Key Performance Indicators (KPIs). You need to establish a baseline before they start. Without that clear "before and after" picture, you're just guessing at your ROI.

Key Performance Indicators to Track

The right KPIs turn your abstract goals into cold, hard numbers. They should tie directly back to the objectives you laid out in your Scope of Work, giving you a clear view of how the partnership is performing.

For most property claims, these metrics are a great place to start:

- Time to Complete Inventory: How many days does it take from the consultant's first site visit to the moment you receive the final inventory report? Every day saved here speeds up the entire claim.

- Valuation Accuracy: What percentage of items have their initial valuation accepted by both the adjuster and the policyholder without a fight? A high accuracy rate is a sure sign of quality work.

- Claim Cycle Time Reduction: This is the big one. Compare the total claim cycle time on claims with a consultant versus those without. It's the ultimate measure of their impact on your overall efficiency.

- Policyholder Satisfaction: Use simple surveys to ask policyholders about their experience with the inventory process. Happy clients almost always mean fewer disputes and a smoother path to settlement.

This focus on data is happening everywhere. The market for Inventory Management Systems is projected to more than double, exploding from $7 billion in 2025 to over $15 billion by 2033, all driven by the need for better analytics. Consultants bring that same data-first mindset to claims, helping you make faster, more accurate decisions. You can discover more insights about the growing demand for data-driven inventory management to see where the industry is headed.

Navigating Common Pitfalls

Even with perfect KPIs, things can go wrong. Being proactive about managing the relationship with your inventory consultant is the best way to avoid the common issues that can derail a project.

The most common point of failure isn't a lack of expertise; it's a breakdown in communication. Small misunderstandings about scope or deadlines can quickly spiral, leading to delays and frustration for everyone involved.

Watch out for scope creep. This is what happens when the project's requirements suddenly expand beyond what you originally agreed to, blowing up your budget and timelines. Think of a simple request to add detailed salvage reports halfway through the job—without adjusting the fee or deadline. That’s a classic example that can quickly strain the partnership.

Poor communication is the other big one. If your consultant goes silent and isn't providing regular updates, adjusters are left in the dark and policyholders get anxious. Set a clear communication rhythm from day one so everyone knows when to expect information.

A hands-on approach helps you spot small issues before they become major headaches, ensuring your investment delivers the results you paid for.

Answering Your Top Questions About Inventory Consultants

Adding an inventory expert to a property claim can feel like another moving part. We get it. It’s natural to have questions about how it all fits together.

Here are the straight answers to the questions we hear most often from carriers, adjusters, and homeowners.

When Is the Best Time to Engage an Inventory Management Consultant?

The best time is as soon as the property is safe to enter. Don’t wait.

Getting a consultant on-site early is a game-changer. They can capture a clean, untampered record of every damaged item before anything gets moved, thrown out, or breaks down further.

We’ve seen what happens when you wait too long. It almost always leads to incomplete lists, arguments over the pre-loss condition of items, and frustrating delays for everyone.

What Is the Typical Cost Structure for These Consultants?

Costs can vary, so it’s critical to get the fee structure ironed out during vetting and have it clearly defined in your contract. No one likes surprises.

You’ll generally see one of three models:

- Hourly Rate: The consultant bills for their time on-site and for research. This is pretty common for smaller or less complicated losses.

- Flat Fee: A single, all-in price is quoted based on the estimated scope of the loss. This gives you cost certainty from the start.

- Percentage of Claim Value: The fee is a set percentage of the total contents claim value.

Always ask for a detailed proposal that breaks down all potential costs. This helps you make sure the expense lines up with the policy's Loss Adjustment Expense (LAE) provisions.

How Do Consultants Handle Valuation Disputes with Policyholders?

A true professional acts as a neutral, data-driven expert. Their job isn’t to pick sides; it’s to establish objective facts. Their valuations are built on methodical research using established databases, online marketplaces, and direct vendor pricing to land on a fair, defensible number.

When a disagreement comes up, the consultant’s role is to provide the detailed documentation to back up their findings. They can walk both the adjuster and the policyholder through the methodology—explaining things like Replacement Cost Value (RCV) vs. Actual Cash Value (ACV)—and provide the evidence to resolve the issue.

This turns a potential argument into a fact-based conversation, which helps de-escalate conflict and get everyone closer to a fair settlement.

Is a Consultant's Report the Final Basis for a Settlement?

No, but a good one gets you most of the way there. Think of the consultant's report as a powerful piece of evidence and an expert recommendation. The final settlement authority always stays with the insurance adjuster.

The adjuster uses that detailed report to verify the loss, confirm coverage applies under the policy, and authorize the final payment. The thoroughness and accuracy of the consultant’s work just give them a strong, defensible foundation to make that decision.

In most cases, a high-quality report makes the validation process faster and forms the core basis for the contents settlement.

At Fox Claims Consultants LLC, we provide the on-the-ground support and detailed reporting you need to handle complex property claims with confidence. From storm damage assessments to comprehensive inventory services, our team delivers the clarity you need to move claims forward. Learn more about our services and how we can help.

Leave a Reply