A storm hits on Friday night. By Monday morning, your queue is full, voicemails are piling up, policyholders want answers, and half the properties on your assignment list have steep roofs, tree impact, or active water intrusion. The pressure isn't just to move fast. It's to move fast without paying on bad information, missing dangerous conditions, or sending people into situations they shouldn't be in.

That’s where many claims operations teams get tripped up. They treat the field inspection piece like a commodity. It isn't. In a heavy-weather environment, the difference between a clean inspection file and a weak one shows up later as re-inspections, estimate disputes, cycle-time drag, avoidable leakage, and unhappy insureds.

A strong insurance claims contractor isn't just another vendor in the chain. Used correctly, that partner becomes your field intelligence layer. They stabilize the site, capture usable evidence, document causation, and give desk adjusters something they can work from. That matters in a market where annual insured losses from natural disasters now exceed $100 billion globally, with total catastrophe costs reaching $151 billion per year, and average property claims processing runs 23.9 days according to insurance claims statistics and trends.

The practical question isn't whether contractors are involved in claims. They already are. Instead, the question is whether you're using the right kind, under the right controls, for the right tasks.

Bringing Order to Claims Chaos

A storm week rarely breaks a claims team at the coverage desk. It breaks in the field. The file stalls when no one can confirm safe roof access, separate fresh storm damage from old deterioration, document temporary repairs, or return with evidence an adjuster can defend.

An insurance claims contractor brings control to that point of failure. The job is to convert a confusing site visit into a field package that supports action: access notes, condition photos, measurements, mitigation observations, and reporting that fits carrier review standards. Adjusters still make the coverage and payment decisions. The contractor improves the quality of the facts those decisions rest on.

That distinction matters operationally. A contractor who only gathers photos adds volume. A contractor who documents conditions in a disciplined way reduces reinspection risk, shortens estimate disputes, and limits the back-and-forth that drags out cycle time.

The operational value shows up in three areas:

- Evidence quality: Useful files document what was inspected, how it was accessed, what was observed, and which facts support causation or scope.

- Safety control: Steep roofs, unstable surfaces, active leaks, and storm debris call for trained field partners with the right equipment and protocols.

- Vendor discipline: Licensed, properly scoped contractors are less likely to create downstream problems through poor documentation, overreach, or biased reporting.

Practical rule: If your first field report can support multiple competing conclusions, the claim is already on a slower and more expensive path.

The trade-off is straightforward. A low-cost field vendor may look efficient at assignment intake, but that savings disappears when the file comes back for clarification, a second inspection, or a challenge from the insured or contractor. Carriers and independent adjusters get better results when they treat claims contractors as controlled specialists, not interchangeable labor.

That requires standards. We look for clear photo sequencing, fact-versus-opinion separation, documented safety decisions, and defined limits on what the field partner can conclude. Those controls help prevent a common failure point in property claims: reports that read more like advocacy than observation.

During CAT intake, even simple visual controls can help keep assignments from slipping. Teams that track inspection status, pending documents, and mitigation follow-up in one place often work faster with fewer handoff errors. A peel-and-stick erase board workflow surface can be a practical option for managing that field queue.

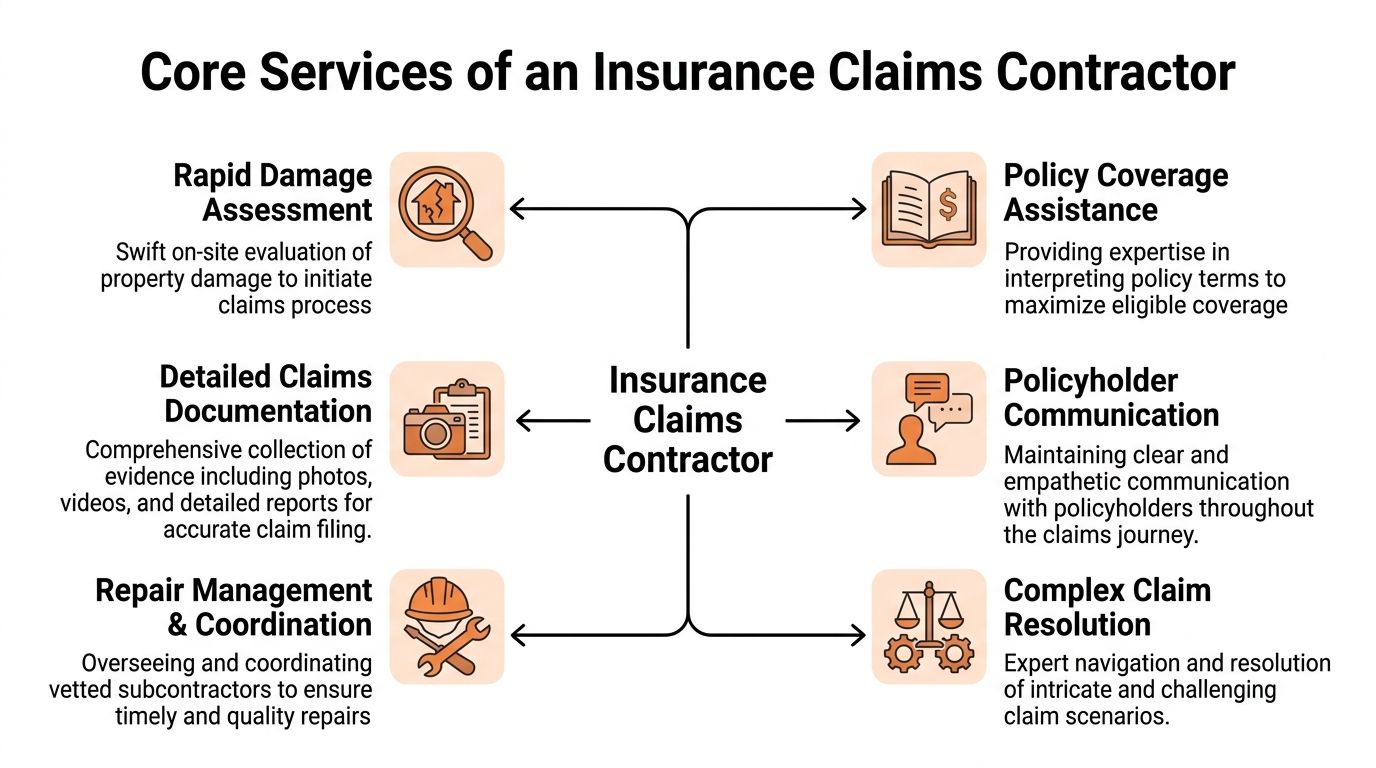

The Core Services of an Insurance Claims Contractor

An adjuster arrives at a loss site with a steep roof, active water intrusion, and a policyholder asking for answers on the spot. That file can move cleanly, or it can turn into reinspection, scope disputes, and preventable safety risk. A skilled insurance claims contractor helps keep it on the first path by handling the field tasks that require access, documentation discipline, and technical judgment.

Property inspections that support claim decisions

Inspection work is the base layer. If the field documentation is weak, every later decision gets harder.

A useful inspection does more than collect photos. It records access points, elevations reviewed, roof sections inspected, exterior components observed, interior indicators of water movement, and any condition that limits certainty. It also separates observation from opinion. That distinction matters when a file is challenged by a policyholder, public adjuster, or roofer.

The best contractors bring order to difficult site conditions. Steep slopes, multi-story elevations, detached structures, soft metals, prior repairs, and mixed causes of loss all require a methodical approach. You need a report that shows what was seen, what could not be safely accessed, and what additional inspection method is justified. That is how carriers reduce rework and avoid paying for conclusions that are not supported by the field record.

Ladder assist that controls safety and file quality

Ladder assist is often treated as simple roof access. In practice, it is a control point for both safety and documentation quality.

Pressure creates bad field decisions. An adjuster under diary load may be tempted to climb a roof that should have been assessed first for pitch, surface condition, weather exposure, and fall risk. A qualified ladder assist team helps control that risk. They set access correctly, support movement across difficult rooflines, and document conditions in real time while the adjuster observes the same surface.

The operational value is straightforward:

- Pre-access evaluation: Roof pitch, material, moisture, height, and weather are assessed before anyone climbs.

- Controlled access setup: Ladders are placed and secured correctly, reducing improvised field choices.

- Paired field documentation: Photos and notes are captured during the inspection, not reconstructed later.

- Clear limits: If access is unsafe, the contractor documents the limitation instead of forcing a poor decision.

Even outside roofing, the principle is the same. A universal steel removal puller tool for windshield extraction exists because the right tool and method produce cleaner results than force and guesswork. Roof access follows that same logic.

One well-documented inspection usually costs less than a rushed inspection followed by clarification, supplement review, and a second site visit.

Emergency services and loss mitigation

Some assignments cannot wait for the normal claims timeline. If wind has opened the roof system, a tree has breached the structure, or water is actively entering the building, the contractor's first job is stabilization.

That work has to do two things at once. It must reduce further damage, and it must preserve the claim record. Temporary tarping, board-up, and water control only help the file if the contractor also documents the pre-mitigation condition, the areas protected, and any evidence that was obscured by the temporary measure. Without that discipline, the carrier inherits a harder causation and scope dispute later.

Strong field partners handle emergency work with clear boundaries. They identify what was done to protect the property, what remains exposed, and what belongs in temporary protection versus permanent repair scope. That keeps mitigation from drifting into unsupported reconstruction.

Estimating and reporting that reduce friction

A contractor's estimate should help the adjuster make a faster, cleaner decision. Poor estimates do the opposite. They create review time, supplement churn, and arguments over line items that were never tied back to field evidence.

The better standard is simple. Every meaningful scope item should be traceable to inspection findings, measurements, material identification, or visible damage. If the estimate includes underlayment, drip edge, starter, ridge, flashing, valley work, interior repair, or detach and reset components, the report should show why those items are there. If the contractor is making an assumption, it should be labeled as an assumption.

This is also where vendor vetting matters. Some contractors write toward repair opportunity instead of claim accuracy. That creates biased reports, inflated scopes, and a higher chance that an unlicensed or overreaching vendor shapes the file before the adjuster does. We look for disciplined photo sequencing, written support for each major line item, and reporting that stays inside the contractor's role. Those controls improve cycle time because desk staff spend less time decoding field reports and more time resolving the claim.

When to Deploy a Specialized Claims Partner

A wind event hits three counties overnight. By 8:30 a.m., your team has a queue full of roof losses, tree strikes, and water intrusions. Some properties need tarping now. Some need ladder assists and steep-slope access. Some need a second set of eyes because the first inspection left causation questions unresolved. That is when a specialized claims partner stops being a convenience and becomes a control point for cycle time, file quality, and field safety.

The decision should be tied to claim complexity and operational strain, not habit. Use a specialized partner on files where delay, poor access, inconsistent documentation, or safety exposure will cost more than the assignment itself.

For carriers managing volume and consistency

Carriers usually feel the need first during surge conditions, but volume is only part of the decision. The larger issue is whether your existing vendor mix can produce the same field package across markets. If one contractor gives clear measurements, labeled photos, and tight scope notes while another sends a vague summary and six unusable images, your desk team inherits the inconsistency.

A specialized partner is the right move when you need one operating standard across a broad footprint. That means defined inspection protocols, clear communication intervals, and reports that stay inside the contractor's role. We use that model at Fox Claims because standardization cuts review friction and helps adjusters make decisions without rebuilding the file from scratch.

Use a specialized partner when you need:

- CAT surge support with controlled intake, triage, and emergency service coordination

- Consistent field documentation across territories instead of market-by-market variation

- Safer handling of steep-slope, high-elevation, or otherwise hazardous inspections

- Faster deployment of temporary protection before secondary damage expands the loss

- A repeatable process for large-loss or technically disputed files

The same logic applies on rural properties and larger sites where access, acreage, and outbuilding exposure complicate the inspection. On losses involving broad grounds review, crop-adjacent exposure, or large property footprints, details as basic as acreage coverage planning for site treatment can affect how field teams scope access, document affected areas, and separate insured damage from surrounding conditions.

For staff and independent adjusters protecting time

Adjusters should deploy a specialized partner when the file demands more field work than claim judgment. If the day is going to disappear into roof access, ladder setup, safety decisions, and repeat site visits, the adjuster is spending high-value time on tasks that can be assigned without giving up claim authority.

That choice matters most on files with narrow margins for error. A steep or slick roof, a tree impact with multiple damage paths, interior staining that could point to more than one source, or a claim where the insured is already disputing causation all benefit from a disciplined field package.

A contractor is worth deploying when:

- The roof is steep, tall, wet, brittle, or otherwise unsafe to access

- The loss includes tree impact, detached components, or multiple affected elevations

- Causation will likely be disputed without stronger photo evidence and measurements

- The first inspection was incomplete and a return trip will slow resolution

- The adjuster needs a neutral field file, not a repair-driven opinion

Keep the authority where it belongs. The contractor documents conditions, measurements, and observed damage. The adjuster handles coverage, valuation, and the final decision.

For homeowners seeking a neutral assessment

Homeowners usually ask for outside help after a confusing inspection. They were told the loss was minor, excluded, or unrelated to the reported event, but the explanation was thin and the documentation did not show how that conclusion was reached.

A specialized field partner helps when the goal is clarity, not advocacy. Good contractors separate observation from opinion, note access limits, identify what was and was not inspected, and document visible conditions in a way the carrier and policyholder can both review. That reduces arguments created by incomplete files and lowers the chance that an unlicensed or biased vendor shapes the claim before the facts are clear.

A second inspection is usually justified when access was limited, the original report lacked support, or the property conditions created legitimate safety barriers for the first inspector.

The Business Case ROI and Key Benefits

Claims leaders don't approve vendor relationships because they sound useful. They approve them when the relationship improves measurable outcomes. With a strong insurance claims contractor, the return usually shows up in cycle time, processing cost, leakage control, and fewer preventable touches.

Better documentation lowers friction

Poor field files create avoidable expense. Missing measurements, unclear causation photos, weak temporary repair notes, and vague scope descriptions force desk teams to reopen issues that should've been settled the first time.

That’s why documentation quality deserves executive attention. According to insurance claims data analysis on documentation quality, high-quality documentation, including high-res photos and 3D scans, directly correlates with 2-10% reductions in claims processing costs. The same source notes that better proof-of-loss documentation helps avoid underpricing, prolonged cycles, and missed subrogation opportunities.

That benefit compounds when catastrophe volumes rise. Every avoidable question in the file becomes another email, another phone call, or another re-assignment.

Reduced cycle time and fewer repeat visits

Cycle time doesn't improve because people work harder. It improves because the file arrives cleaner. A strong contractor package gives the desk adjuster enough detail to make a decision or move quickly to the next decision point.

Three practices produce the biggest payoff:

- Evidence captured in one trip: Roof, exterior, interior, and emergency mitigation notes should work together as one file.

- Consistent estimating inputs: Clean measurements and material detail reduce back-and-forth with estimating teams.

- Structured handoff notes: The person reviewing the claim shouldn't have to guess what the field inspector intended.

For operations teams looking to reduce repeat handling, the principle is simple. The first file should be settlement-ready or close to it.

A durable claims process also depends on strong field support hardware and disciplined workflows. Even something as ordinary as a vehicle reinforcement bar for field fleet reliability points to the larger operational truth. Stable systems support faster response.

Lower loss adjustment expense and safer execution

Loss adjustment expense rises when you stack specialist visits. One person inspects. Another returns for access. A third documents mitigation. A fourth rechecks because the first set of photos wasn't enough. That is an expensive habit.

A specialized contractor can consolidate much of that work into one coordinated assignment. The direct savings come from fewer trips and cleaner intake. The indirect savings come from safety. Sending properly equipped field personnel to steep and tall roofs reduces the pressure on adjusters to handle dangerous inspections themselves.

This short clip illustrates the broader need for disciplined field operations and evidence-driven claim handling:

Stronger indemnity decisions

The best ROI isn't always visible as a line-item reduction. Sometimes it's the claim you pay correctly the first time.

A contractor who documents conditions well helps prevent both overpayment and underpayment. Overpayment can happen when scope is padded because nobody captured enough field detail to challenge it. Underpayment happens when real damage is missed or poorly documented, which invites supplements, disputes, and service complaints later.

Field standard: If a line item can't be traced back to a photo, note, measurement, or observable condition, it deserves another look before approval.

When claims leaders talk about ROI from an insurance claims contractor, they're really talking about confidence. Confidence that the site was assessed safely. Confidence that the estimate reflects actual conditions. Confidence that the desk adjuster isn't making payment decisions from a thin file.

How to Choose the Right Insurance Claims Contractor

The market is full of people who can take pictures of damage. That doesn't mean they belong in your claims process. The right partner reduces uncertainty. The wrong one inserts more of it.

This matters more as carriers outsource field work. A McKinsey report highlighted in this discussion of unlicensed professionals adjusting claims notes that carriers are shifting up to 30% of their workforce to outside vendors. The risk is obvious. Vendors who influence payment decisions without the right training or licensing awareness can miss damage, write weak estimates, and lengthen the claim.

Green flags that signal a reliable partner

Start with capability, then verify discipline. A qualified insurance claims contractor should be able to explain exactly how they handle difficult roofs, emergency services, causation documentation, and reporting standards.

Look for these green flags:

- Safety program with teeth: They can explain roof access protocols, weather stoppage rules, fall protection practices, and when they won't put personnel on a surface.

- Clear lane discipline: They know the difference between factual site reporting and claims advocacy, and they stay in the proper role.

- Evidence-first reporting: Their sample file includes labeled photos, measurements, elevation references, and observations tied to scope.

- Standardized communication: You know when you'll receive contact confirmation, inspection status, emergency updates, and final deliverables.

- CAT readiness: They can discuss dispatch, triage, and reporting consistency when volume spikes across multiple states.

Ask for a sample workflow, not just a capabilities sheet. The workflow tells you how the engagement will behave under pressure.

Red flags that usually lead to trouble

The warning signs are usually visible early. Vague answers, loose process language, and pressure to “just trust the field team” often predict weak files later.

Be cautious when a vendor shows these traits:

- No proof of insurance or unclear liability coverage

- Reports that blur fact, opinion, and negotiation language

- Pressure to use affiliated repair vendors without a neutral inspection basis

- Inconsistent file structure from one assignment to the next

- Poor response discipline during initial onboarding

A reliable partner doesn't resent scrutiny. They expect it.

Vetting checklist for procurement and claims leaders

The fastest way to compare vendors is to force specificity. Put the same questions to each one and review their actual deliverables.

| Attribute | Green Flag (Reliable Partner) | Red Flag (Potential Risk) |

|---|---|---|

| Safety approach | Written access and stop-work protocols | “We figure it out on site” |

| Reporting quality | Labeled photos, measurements, clear observations | Unsorted photos and short narrative summaries |

| Role boundaries | Stays in inspection and documentation lane | Speaks as if they are adjusting the claim |

| Communication | Defined status updates and contacts | Status depends on who answers the phone |

| Emergency response | Can document pre-mitigation and temporary repair actions clearly | Can tarp a site but can't explain what was preserved |

| Scalability | Consistent process across markets | Quality changes by territory or subcontractor |

One practical onboarding step is to require a mock assignment. Give the vendor a sample loss type and ask them to show intake, dispatch, field documentation, estimate support, and final report format.

For teams building SOPs around vendor review, a complete service and repair manual-style reference approach is a good model. The best contractor relationships run on documented procedures, not verbal assumptions.

Critical Questions for Claims Professionals

A claim can go off track long before a coverage decision is issued. It happens when the file starts relying on field reports that are thin, inconsistent, or written in a way that pushes the reader toward a conclusion instead of documenting the facts. Claims professionals need a way to pressure-test contractor output before it shapes reserve decisions, reinspections, or litigation posture.

How do we identify and counter biased reports

Start with role discipline. A claims contractor should document site conditions, capture measurements, and record what was observed. They can support technical interpretation within their scope. Payment position and claim advocacy belong elsewhere.

Bias usually shows up in the report structure before it shows up in the conclusion. Photos skip key elevations. Interior damage is mentioned without room-by-room support. Excluded items disappear from the file without explanation. Boilerplate language appears in losses that clearly required property-specific analysis. Those are operating problems, not just writing problems, because they slow review and invite dispute.

A William Professional Association analysis of insurer tactics and engineering disputes points to post-hurricane conflicts tied to engineering reports that policyholders or reviewers viewed as incomplete or slanted. That is the practical lesson for carriers and adjusters. If the field evidence is not traceable, the report becomes hard to defend and expensive to revisit.

Use a screening test that forces the file to stand on its own:

- Can a second reviewer trace the inspection from site arrival through final opinion using only the report, photos, and measurements?

- Do the images and notes document each material area inspected, including areas with no visible damage?

- If an item was excluded, is there a stated reason tied to observations rather than silence in the file?

- Would an expert who has never seen the property understand what was found, what was limited, and what still needs follow-up?

A report should let another qualified person reconstruct the inspection logic without calling the inspector for clarification.

What's the best way to manage third-party contractors during a CAT event

CAT failures usually start with expansion before control. New vendors get activated, assignments surge, and every partner submits a different product. Desk adjusters then spend their time translating reports instead of making claim decisions.

The fix is operational discipline. Build one intake standard, one report structure, one status cadence, and one escalation path for unsafe conditions or access problems. Audit the first wave of files immediately. If a vendor is drifting on photo standards, mitigation documentation, or turnaround expectations, correct it in the first few assignments.

We use this approach at Fox Claims because CAT volume punishes inconsistency fast. A contractor network only helps if your staff can read the output quickly, compare files across territories, and spot exceptions before they become reopen rates, supplements, or complaints.

How do we integrate contractor reports into the claims system

Integration is less about software than file design. If the contractor delivers unlabeled photos, mixed mitigation and repair notes, or narratives that change by market, the claims system just stores confusion faster.

Useful reports are structured for claim handling. They include labeled photo sets, measurements, scope notes, documented temporary repairs, causation observations within the contractor's lane, and estimate-ready details that map cleanly into the file. Whether the upload is automated or manual matters less than consistency.

Before launch, ask questions that expose whether the contractor can support your workflow:

- What photo set is required for each loss type?

- How are elevations, slopes, rooms, and detached structures labeled in the file?

- How do you separate emergency mitigation records from permanent repair scope?

- Will the report format stay the same across all territories and subcontracted coverage areas?

- What is delivered when access is restricted, evidence is disturbed, or site conditions change mid-inspection?

How should contractors and adjusters divide responsibilities

This boundary needs to be clear on day one. Contractors document, inspect, measure, and report. Adjusters evaluate coverage, apply policy language, set payment position, and communicate the claim decision.

Problems start when the contractor writes as if they are deciding the claim, or when the adjuster expects a general field vendor to resolve specialized causation issues without the right credentials or scope. Both errors create risk. One invites bias arguments. The other produces weak technical support.

The strongest partnerships are built on defined scope, report standards, licensing compliance where required, and documented escalation rules for disputed or unsafe conditions.

If you need a national field partner for steep and tall roof inspections, storm and tree damage assessments, ladder assist, emergency tarping, or precise property documentation, Fox Claims Consultants LLC provides safety-focused inspections, rapid response, and clear reporting built to help carriers, adjusters, and policyholders move claims forward with less friction.

Leave a Reply