Catastrophe adjuster insurance isn't just a line item on a budget; it's the core protection that allows independent claims professionals to work in some of the most challenging environments imaginable. This isn't just one policy, but a specific combination of coverages, primarily Errors & Omissions (E&O) for professional mistakes and General Liability for accidents on-site.

This insurance ensures you can handle high-stakes claims without putting your personal finances on the line.

Why Catastrophe Adjuster Insurance Is Non-Negotiable

Picture yourself as the first adjuster on the ground after a major hurricane, navigating streets filled with debris to help families begin the long process of rebuilding. This is the reality for a CAT adjuster, and it's a world packed with professional and personal risk.

For these critical professionals, having the right insurance isn't just a good idea—it’s the essential toolkit for surviving a high-stakes career.

Think of it like a pilot's pre-flight checklist. Before ever leaving the ground, a pilot confirms every system is ready to go. Your insurance portfolio does the same thing, protecting you from the financial turbulence that can hit without warning. It could be a simple miscalculation on a multi-million-dollar commercial roof or accidental property damage during an inspection. One mistake could ground your career for good.

An Escalating Need for Protection

The need for solid coverage has grown right alongside the increasing frequency and intensity of major disasters. We've seen a dramatic spike in billion-dollar weather events across the country.

According to NOAA data, what used to be an average of just three of these disasters per year in the 1980s has exploded to around 20 events annually in the 2020s. This new normal puts immense pressure on carriers and the adjusters they deploy.

The potential for a career-ending lawsuit is very real and growing. A single oversight on a complex claim can trigger litigation that easily wipes out an adjuster's personal assets, making comprehensive insurance an absolute necessity.

Before we dive deeper, here’s a quick overview of the essential policies every adjuster needs to have in their toolkit.

Quick Guide to Essential Adjuster Coverages

| Insurance Type | Primary Purpose | Who It Protects |

|---|---|---|

| Errors & Omissions (E&O) | Covers claims of negligence or mistakes in your professional work (e.g., a scoping error). | Your business assets and personal finances from lawsuits. |

| General Liability | Covers third-party bodily injury or property damage you might cause on-site (e.g., your ladder falls on a car). | You from the costs of accidents that happen during an inspection. |

| Commercial Auto | Covers accidents involving your work vehicle, which personal auto policies often exclude. | You and your business if you're in an accident while driving for work. |

| Workers' Compensation | Covers medical expenses and lost wages if you are injured on the job. | You from the financial burden of a work-related injury. |

These policies work together to create a safety net, allowing you to focus on the job without worrying about what could go wrong.

The High Stakes of the Job

The work itself is inherently dangerous. You’re dealing with heights, unstable structures, and potential hazards at every turn. A robust insurance plan doesn't just protect your business—it gives you the confidence to do your job right.

Beyond the physical danger, the professional liability is massive. A tiny error in a damage report or an overlooked building code can come back as a lawsuit months or even years down the road.

Your insurance is your first and best line of defense. It ensures you can continue doing the vital work of helping communities recover without risking your own financial future. Protecting yourself is step one, and fully understanding adjuster safety in CAT zones is just as critical for a long and successful career.

Building Your Foundational Insurance Portfolio

Putting together your insurance coverage as a catastrophe adjuster is a lot like packing your gear for a deployment. You don't just throw things in a bag; you start with the essentials—the non-negotiable items that protect you from the biggest risks.

For an independent adjuster, this means building a foundation with three core policies. Without them, you're stepping onto a storm site with your career and finances completely exposed.

Errors and Omissions (E&O) — The Professional Safety Net

Your Errors & Omissions (E&O) policy is your professional liability coverage. It's what protects you when a mistake in your work leads to a lawsuit. In the high-stakes world of catastrophe claims, even a small oversight can have massive financial consequences.

Think about it. You miscalculate the square footage on a complex roof. You overlook a critical building code update that costs the policyholder thousands. Months later, you get a letter from an attorney. These aren't far-fetched scenarios; they happen.

E&O insurance is designed for exactly this. It helps cover your legal defense, settlements, and judgments. With lawsuits sometimes claiming an adjuster's report was altered by someone else entirely, this coverage isn't just a good idea—it's essential. A single error shouldn't be able to end your career.

General Liability — The On-Site 'Oops' Policy

While E&O covers your paperwork and decisions, General Liability (GL) covers your physical presence on-site. It’s for the unpredictable "oops" moments that are bound to happen in the chaos of a post-disaster environment.

This is your coverage for things like:

- Your ladder slipping and smashing a homeowner's picture window.

- Someone tripping over your tool bag and getting injured.

- The classic—accidentally stepping through a ceiling while inspecting an attic.

Without GL, you’re paying for that new window, the medical bills, or the drywall repair out of your own pocket. A standard policy handles these third-party claims for bodily injury and property damage, ensuring an on-site mishap doesn’t become a financial disaster.

These are the real-world risks every adjuster faces, and a solid insurance foundation is what lets you manage them effectively.

Commercial Auto Insurance — For the Road Warrior

Never, ever assume your personal auto policy has you covered for work. The second you start using your truck to drive from one inspection to the next, you're operating commercially. If you get in an accident, most personal auto insurers will deny the claim flat out.

That’s why Commercial Auto insurance is the third pillar of your protection. Think of the conditions you drive in—roads littered with debris, unfamiliar storm-ravaged neighborhoods, and constant travel. It's a high-risk environment.

A Commercial Auto policy is built for these work-related realities, covering your liability and physical damage. For any adjuster who lives out of their vehicle on deployment, this is a non-negotiable part of being a professional.

Specialized Coverages for Proactive Adjusters

So, you’ve got your foundational policies in place—E&O, General Liability, and Commercial Auto. That’s a great start, but the job isn't done. Experienced adjusters know that true security means covering all the angles, especially the ones that can sneak up on you.

We’re talking about protecting the expensive gear you rely on every day and the sensitive data you handle with every claim. These aren't just add-ons; they’re the coverages that turn a basic safety net into a comprehensive shield for your business.

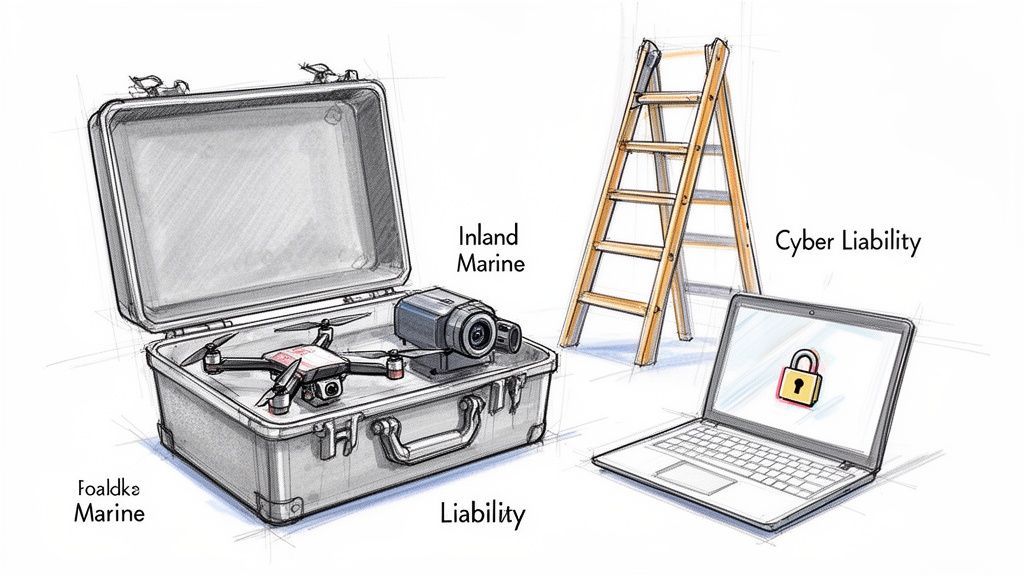

Protecting Your Tools with Inland Marine

Think about your most valuable equipment. Your drones, thermal cameras, specialty ladders, and high-powered laptops are the very tools that make you effective. The problem is, your standard property insurance usually only covers them when they're sitting at a single, specified address.

But as a CAT adjuster, your office is your truck, a storm-ravaged neighborhood, or a steep rooftop. Your gear is always on the move.

That’s where Inland Marine insurance steps in. Don't let the name throw you; it has nothing to do with boats. Think of it as a personal bodyguard for your equipment, following it from your vehicle to the inspection site and back again. If your $5,000 drone gets swiped from your truck or your thermal camera takes a tumble, Inland Marine is what helps you replace it without skipping a beat.

Guarding Data with Cyber Liability Insurance

In this line of work, you are a walking, talking database of sensitive information. You’re constantly handling policyholder names, addresses, policy numbers, and even financial details—often on a laptop in a hotel lobby or a coffee shop with questionable Wi-Fi.

This is the modern-day risk every adjuster faces, and Cyber Liability insurance is built to address it head-on. If you have a data breach—say, a stolen laptop or a hacked phone—this coverage is your lifeline.

It’s designed to help cover the massive costs that follow, such as:

- Notification costs for alerting every affected policyholder.

- Credit monitoring services to help protect the victims.

- Legal defense and crippling fines if you get sued over the breach.

In an era where a single lost laptop can spiral into a major privacy disaster, Cyber Liability is no longer a luxury. It's a non-negotiable part of a professional catastrophe adjuster's insurance portfolio.

Understanding Workers Compensation for Adjusters

The final piece of this puzzle is Workers' Compensation, and how it applies to you depends entirely on your business structure. If you’re a W-2 employee for an adjusting firm or carrier, good news—your employer is required by law to provide this for you.

But if you’re a 1099 independent contractor, you are the business. The firms that hire you won’t cover you. It's your responsibility, period.

This is a critical distinction many overlook. Without it, a simple fall from a ladder can mean career-ending medical bills and lost income with absolutely no safety net. For adjusters navigating treacherous storm sites, knowing your limits and having the right backup is crucial. That includes knowing when to call for a steep roof assist to keep yourself safe and ensure the job gets done right.

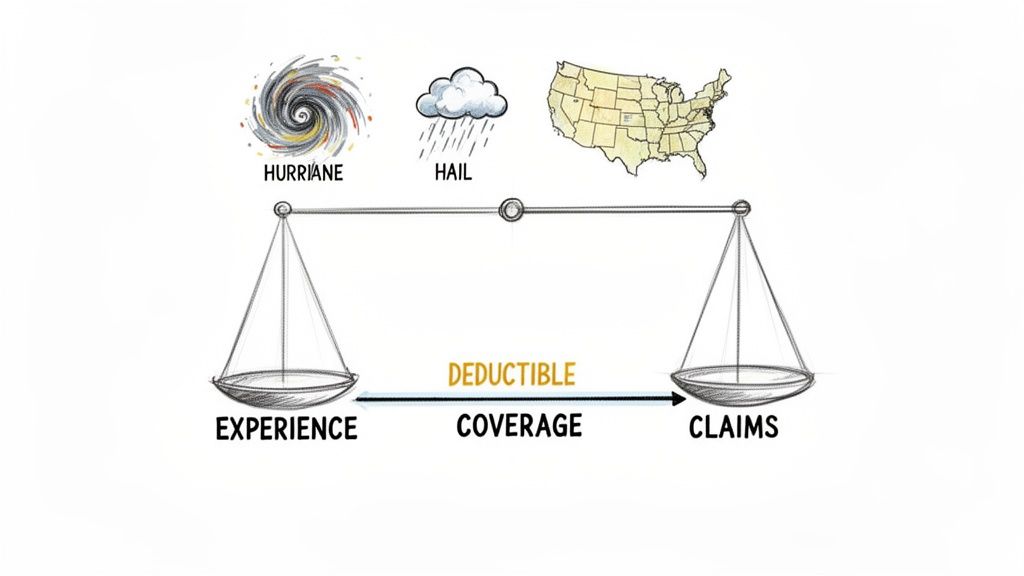

How Your Insurance Premiums Are Calculated

Ever wondered what actually goes into your insurance quote? It’s not just a number pulled from a hat. Insurers are essentially calculating risk, and they look at a handful of key factors to build a profile that’s unique to you and your work.

Your track record is the first thing they’ll look at. An adjuster with ten years in the field and a clean history is a much safer bet than someone brand new. A history of E&O claims? That’s a red flag for underwriters, and it almost always means higher premiums.

The Nature of Your Work Matters

The kind of disasters you run toward and the properties you climb on play a massive role in your rate. It’s a simple reality of the job.

An adjuster scoping high-value commercial properties after a hurricane is carrying a lot more liability than someone handling minor hail dings on residential homes. The potential for a seven-figure mistake is just plain higher when you’re dealing with a massive, complex commercial loss.

- High-Risk Adjusters: If you’re regularly on steep roofs, inspecting total fire losses, or assessing large commercial buildings, expect higher premiums. The complexity and claim values are just greater.

- Lower-Risk Adjusters: If you specialize in daily auto claims or simple residential jobs, your rates will likely be lower because the financial exposure is more contained.

Even the states where you hold a license can move the needle. Operating in places known for being more litigious, like Florida or California, can bump up your premium simply due to the legal environment and the sheer volume of claims.

Balancing Cost and Protection

The most direct levers you can pull to manage your premium are your policy limits and deductible. It’s a classic trade-off.

A higher deductible means you pay less each month, but you’ll have a bigger out-of-pocket expense if a claim ever hits. On the flip side, higher coverage limits give you a much stronger safety net, but your premium will reflect that.

Finding that sweet spot is the goal. You need enough catastrophe adjuster insurance to protect your livelihood without being "insurance poor." You want to walk onto any job site feeling confident that your assets are covered.

This insurance is a non-negotiable investment in your career. We’ve seen firsthand how independent adjusters on major storms can pull in six-figure incomes in just a few months. The median annual wage for claims adjusters is $76,790, with top-tier markets pushing well past $90,000. Protecting that earning power is everything. Verisk’s PCS Catastrophe Compensation Report offers a deeper dive into these compensation trends.

At the end of the day, your premium is a reflection of your specific risk. Being disciplined about managing that risk—from keeping a clean claims history to using a detailed property inspection report template on every job—is the best way to keep your insurance costs in check over the long haul.

Smart Risk Management for Carriers and Firms

When a major catastrophe hits, deploying a wave of independent adjusters is a massive operational lift. It’s how you handle the overwhelming claim volume, but it also opens your company up to significant risk. A smart risk management strategy isn't just about protecting your bottom line—it’s about safeguarding your reputation and ensuring your policyholders get the fair and timely service they deserve.

Your first line of defense is a rock-solid vetting process. Think of it as building your disaster response team with professionals who are just as prepared and protected as your own staff. This has to go way beyond just confirming they have a valid adjuster license.

A Vetting Checklist for Contract Adjusters

Your firm needs a non-negotiable checklist for every single independent contractor before they’re ever activated. This isn't bureaucracy; it's about creating consistency and minimizing your exposure from day one.

- Verify Certificates of Insurance (COIs): Never take an adjuster's word for it. You need a current COI sent directly from their insurance provider. Critically, this certificate must name your firm as an additional insured, which extends their policy’s protection to cover your company.

- Confirm Adequate Coverage Limits: Set clear, minimum requirements for catastrophe adjuster insurance. This means specific limits for both Errors & Omissions (E&O) and General Liability. A common standard is $1 million per occurrence and a $2 million aggregate, but you should align this with the value and complexity of the claims you expect to handle.

- Review Policy Exclusions: Don't stop at the COI. Ask for the full policy declaration pages to see what’s excluded. You need to be certain their coverage is actually suitable for the specific perils and environments they’ll be working in.

A well-defined contract is the other piece of the puzzle. This legal document should leave zero room for interpretation.

A well-drafted contract clearly outlines the scope of work, service level agreements (SLAs), and, most importantly, the insurance and indemnification duties of the independent adjuster. It contractually transfers specific risks from your firm to the adjuster, which is then covered by their own insurance policies.

This structured approach is absolutely essential for managing the sheer scale of modern disasters. According to the Insurance Information Institute, insured losses from U.S. catastrophes hit an incredible $115.6 billion in 2023. Events of this magnitude will always overwhelm internal teams, making it vital for carriers to partner with reliable national firms. You can discover more insights on the rising impact of U.S. catastrophes on iii.org.

By rigorously vetting every contractor and using ironclad contracts, carriers can build a resilient, scalable response force. This allows you to manage corporate risk effectively while leveraging specialized partners and inspectors on demand to ensure accurate and prompt claim resolution for policyholders.

Your Top Insurance Questions, Answered

When you're out in the field, the last thing you want to worry about is whether you have the right insurance. Getting your coverage squared away isn't just a box to check—it’s the foundation of a solid career.

We get a lot of questions from adjusters trying to navigate the insurance landscape. Here are the straight answers to the most common ones we hear.

I'm a W2 Employee. Do I Still Need My Own E&O Policy?

If you're a W-2 employee working directly for an adjusting firm or an insurance carrier, you're almost always covered under their corporate Errors & Omissions (E&O) policy. They've got you covered.

But here's a pro tip: never assume. It's always a good move to check with your HR department. Ask about the policy's limits and understand exactly what it covers.

For independent (1099) adjusters, it's a different story. You're your own business, and the hiring firm’s policy won’t extend to you. You are absolutely required to carry your own E&O insurance. No exceptions.

What Are the Standard E&O Coverage Limits?

For a long time, the industry standard for independent cat adjusters was a policy with $1 million per occurrence and a $1 million aggregate limit. This is still a common baseline.

However, the game is changing. Many of the bigger carriers and IA firms now require higher limits to even get on their roster, often asking for a $2 million aggregate.

The right limit for you really depends on two things: the value of claims you typically handle (large loss commercial vs. residential) and, most importantly, the requirements of the companies you want to work for.

Key Takeaway: Your insurance has to match the requirements of the firms deploying you. Always double-check their minimums before you sign a contract. Showing up underinsured is a quick way to get sent home from a deployment.

Can I Just Get One Policy to Cover Me Everywhere in the US?

Yes and no. Your core insurance policies, like General Liability and E&O, will typically cover your work nationwide. From an insurance standpoint, you're good to go.

The real roadblock isn't your insurance—it's your licensing.

You must hold a valid adjuster license for the state you're physically working in. Your insurance policy could be perfect, but without the right state license, you're operating illegally. That can get a claim thrown out, expose you to massive fines, and put a serious dent in your professional reputation.

As you look to work in new areas, it's helpful to understand how partners can provide expert insurance claims assistance that aligns with regional rules and regulations.

When you're facing high-risk structures and need a partner you can trust, Fox Claims Consultants LLC delivers. Our certified inspectors provide rapid, safe, and thorough assessments for steep roofs, storm damage, and more. Get the reliable support you need to move claims forward fast.

Leave a Reply