The storm has moved on. Your claim queue hasn’t.

Phones are ringing, first notices are stacking up, policyholders want timelines, and your internal team is already triaging files before sunrise. In that environment, a cat claims adjuster isn’t just another field resource. They’re the person you send into a compressed, chaotic operating zone where speed matters, documentation matters, and bad field decisions echo through the entire file.

For carriers, desk adjusters, TPAs, and independent firms, defining the role is rarely the issue. The difficulty lies in using that role correctly. A CAT response breaks down when the field runs ahead of process, when desk reviewers get weak photo sets, or when high-risk inspections sit untouched because nobody should be climbing that roof under those conditions. That’s where operations discipline separates a manageable surge from a costly mess.

After the Storm The Role of the CAT Claims Adjuster

A major storm creates the same pattern every time. The event passes, access opens in patches, and then the inflow starts all at once. Wind claims, tree strikes, interior water damage, roof reports, partial collapses, and emergency mitigation requests all hit the carrier within a narrow window.

That’s the moment the cat claims adjuster steps in. This isn’t a routine local adjuster working a steady book of business. It’s a field specialist deployed into a catastrophe zone to inspect loss sites quickly, document conditions accurately, make coverage-relevant observations, and feed usable information back into the claim workflow so payments and next steps don’t stall.

What the role looks like in the field

A CAT adjuster’s job starts with mobility and judgment. They enter unstable environments, work from changing schedules, and often inspect multiple damaged properties in a single day. They have to move fast without getting sloppy.

The role matters because the field inspection is where the file either gains clarity or starts drifting. If the scope is incomplete, if the photos don’t show the right elevations, if the inspector misses a mitigation need, or if the cause-and-effect story is weak, the desk side ends up rebuilding the file later. That costs time and credibility.

A few field realities define the role:

- They work surge volume: The assignment load comes in concentrated waves, not a smooth daily flow.

- They build the file foundation: Desk teams depend on their photos, measurements, notes, and initial estimate logic.

- They operate in damaged environments: Access issues, debris, weather exposure, and unsafe structures are normal, not exceptional.

- They support decision speed: Good field work shortens the path to reserve accuracy, payment review, supplements, and closure.

Practical rule: In CAT operations, the first inspection isn’t just an inspection. It’s the first version of the whole claim strategy.

Why definition alone isn’t enough

The broad concept is understood. After a disaster, carriers deploy adjusters. That part is simple. The harder question is how to make the deployment effective when files involve steep roofs, emergency tarping, tree impacts, difficult access, and policyholders who need answers immediately.

That’s where claims operations has to think beyond staffing counts. Capacity isn’t just the number of adjusters available. Capacity is how many files you can inspect safely, document correctly, and convert into desk-ready claims without rework.

Even something as ordinary as field prep can become operationally important. Basic measurement tools, staging supplies, and property documentation habits all affect file quality, whether you’re looking at a roof slope or organizing temporary site materials like food-safe empty pails for storage and field use.

CAT Adjuster vs Desk Adjuster Unpacking the Key Differences

The easiest way to understand the distinction is this. A CAT adjuster works like an emergency room physician. A desk adjuster works more like the doctor coordinating diagnosis, records, next steps, and follow-up. Both matter. They just solve different problems under different conditions.

The CAT side deals with concentration, access, and triage. The desk side deals with file integrity, coverage review, estimate reconciliation, communication, and closure. Confuse those roles, and claim handling gets inefficient fast.

Why the field role feels different

A catastrophe deployment begins after a formal catastrophe designation with a PCS CAT number, which triggers mobilization of personnel and resources. In that setting, CAT claims adjusters often handle 8 to 15 inspections per day, far above routine workloads, according to National Adjuster Authority’s CAT services overview.

That number explains the operating mindset. A CAT adjuster can’t approach every file like a long-form investigation on day one. The work is triage-based. The first priority is to get to the property, verify visible damage, capture complete documentation, identify urgent mitigation issues, and move the file into a desk-ready state.

Desk adjusters carry a different burden. They may never step on the property, but they still own important claim decisions. They review policy terms, examine estimates, request supplements, coordinate with vendors, issue payments, and manage communication when the insured has questions or disagreements.

Adjuster role comparison

| Attribute | CAT Claims Adjuster | Staff Claims Adjuster | Desk Claims Adjuster |

|---|---|---|---|

| Primary environment | Field deployment in catastrophe zones | Local or regional territory | Office or remote claim handling environment |

| Work pattern | Surge-based, event-driven | Steady caseload | Continuous file management and review |

| Typical pace | High-speed triage | Balanced and scheduled | Multi-file coordination |

| Volume profile | Very high during events | More predictable | High administrative and communication load |

| Core output | Inspection findings, photos, measurements, estimate input | Investigation and adjustment of assigned claims | Coverage review, estimate review, payment handling, supplements |

| Best use case | Large event response, rapid field capture | Routine claim handling in normal operations | Managing file progression after field data arrives |

| Main risk if underperforming | Incomplete scope, unsafe inspection decisions, weak documentation | Delays and uneven service | Bottlenecks, rework, poor policyholder communication |

What works and what doesn’t

The strongest CAT operations respect the handoff. The field side gathers facts. The desk side turns those facts into decisions. Trouble starts when one side assumes the other will fill in missing pieces.

What works:

- Clear inspection instructions: Tell the field exactly what must be documented. Elevations, roof test areas where appropriate, interior rooms, detached structures, mitigation status, and site hazards should be explicit.

- Tight photo standards: Require complete photo sets, not a random camera roll.

- Defined escalation rules: If the structure is too steep, too high, unstable, or obstructed, the file should escalate immediately rather than inviting unsafe improvisation.

- Fast desk review: Good field work loses value if it sits untouched in the queue.

What doesn’t work:

- Vague assignments: “Inspect and send estimate” is not an operating plan.

- Assuming every adjuster should climb every roof: They shouldn’t.

- Separating estimate review from field reality: If the desk team doesn’t understand how the property was inspected, supplement disputes multiply.

- Late communication with the insured: Silence makes every timeline feel longer.

The field doesn’t need more guesswork. It needs cleaner instructions and faster decisions on exceptions.

The dependency most teams underestimate

Desk adjusters rely on CAT adjusters more than many workflows admit. If the first inspection misses a steep rear slope, a detached garage, or active water intrusion, the desk file starts with blind spots. Then come supplement requests, callback inspections, and avoidable friction with contractors and policyholders.

That’s why a cat claims adjuster shouldn’t be measured only by speed. Speed matters, but usable accuracy matters more. A fast inspection that creates three rounds of rework isn’t efficient. It’s just front-loaded delay.

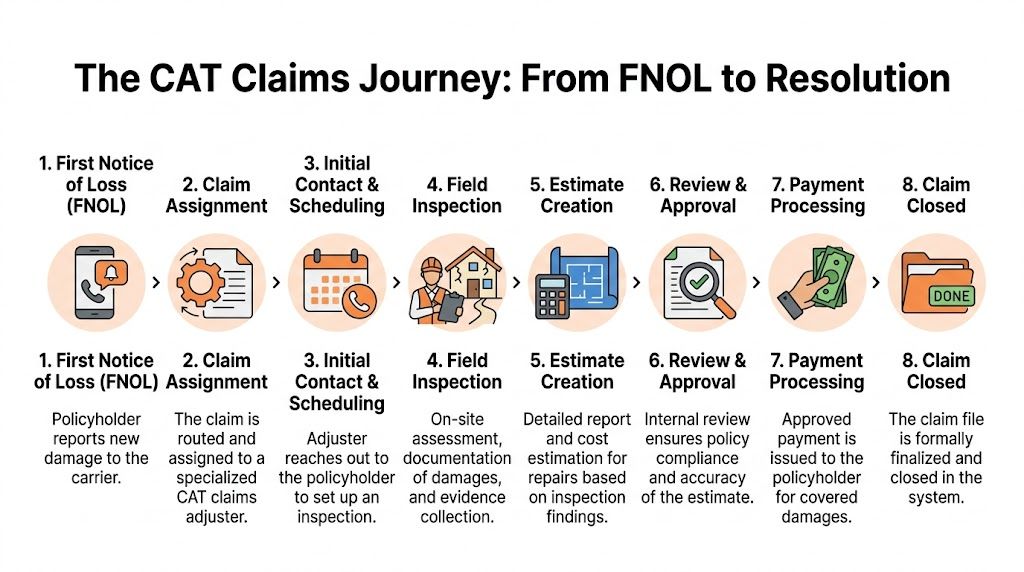

From First Notice of Loss to Claim Closed The CAT Timeline

A CAT file moves best when everyone understands the sequence. In surge conditions, confusion usually comes from skipped handoffs, not from lack of effort. The timeline below is the operational path most carriers are trying to protect.

Hurricane Katrina remains the clearest historical reminder of what scale does to claims operations. It generated over 1.7 million insurance claims and led to deployment of about 15,000 adjusters, making it one of the largest mobilizations on record, as noted in EBSCO’s overview of claims adjusting. Large-scale events force discipline because there’s no room for loosely managed response.

The operating sequence

First notice of loss arrives

The policyholder reports damage. At this point, the carrier needs clean intake data, property location accuracy, contact details, and a basic description of loss conditions.Claim assignment happens

The file gets routed based on event type, severity, geography, and staffing model. Some claims can move through standard field paths. Others need immediate escalation because of safety issues or severe access problems.Initial contact and scheduling begins

This step looks simple but often determines customer perception. Fast outreach sets expectations, confirms occupancy and site safety, and surfaces urgent mitigation needs before the inspection date.Field inspection takes place

The adjuster or inspection resource visits the property, documents visible damage, records measurements, assesses conditions, and identifies anything that changes the scope or urgency of handling.

Where carriers gain or lose time

The most common breakdown is between assignment and inspection. Files linger because contact isn’t made quickly, route density is poor, or unsafe structures aren’t redirected to the right field partner soon enough.

A second breakdown happens after the inspection. The field may upload photos and notes, but if reporting lacks structure, the desk adjuster spends valuable time reconstructing what happened on site. A tape measure sounds basic, but disciplined measurement and consistent reporting are still the backbone of property loss review. Even small field tools such as a soft flexible dual-sided tape measure reflect a bigger point. Precision in the field supports speed in the file.

Field lesson: If the inspection package can’t stand on its own without a follow-up call, it isn’t finished.

What a good CAT timeline produces

A clean timeline creates three operational benefits.

- Better reserve confidence: Early facts support better financial handling.

- Fewer unnecessary touchpoints: Strong first-pass documentation reduces avoidable callbacks.

- Clearer policyholder communication: When the file is moving, the insured hears specifics instead of vague status updates.

The final stages that decide closure quality

After inspection, the estimate is created and reviewed. The desk side checks the estimate against policy terms, photos, measurements, and applicable internal standards. Payment handling follows for covered damage, and supplements are addressed if repair-discovered conditions emerge later.

Closure should happen only when the file tells a coherent story. That means the cause of loss, scope, estimate support, communication log, and mitigation record all line up. If any of those pieces are weak, the claim might be technically closed but operationally unresolved.

For claims leaders, the timeline isn’t just a sequence. It’s a control system. Every handoff should answer one question: did the previous step give the next person enough to act without guessing?

Mastering High-Risk Inspections Safety and Specialized Services

The steep roof is where CAT theory meets field reality.

In a surge event, everyone wants speed. But speed stops helping the moment an inspection becomes unsafe or incomplete. A wet multi-story roof, tree-loaded elevation, brittle surface, or awkward ladder position changes the assignment immediately. The file still needs to move. It just can’t move by asking the wrong person to take the risk.

Why general field capacity isn’t enough

A cat claims adjuster has to make rapid coverage-relevant observations. On roof losses, that includes distinguishing storm-created conditions from wear, prior damage, installation issues, or manufacturing defects. That’s a technical task, not just a visual one.

According to BSA Claims’ guide for insurance providers and claims adjusters, CAT adjusters must distinguish wind-driven hail damage from pre-existing manufacturing defects. The same source notes that independent partners handling ladder assists and emergency tarping can provide a 24 to 48 hour boots-on-ground response and that accurate Xactimate-compliant estimates can reduce settlement cycle times by 15 to 20 percent.

That matters because a difficult roof claim usually fails in one of three ways:

- The adjuster climbs when they shouldn’t

- The adjuster avoids the difficult area and submits an incomplete scope

- The file waits too long for a qualified inspection resource

None of those outcomes help the carrier or the insured.

Ladder assist and emergency services are operating tools

Ladder assist is often misunderstood as a convenience. It’s really a control measure. It gives the file a safer path to documented access on difficult structures and reduces the odds that the inspection depends on improvised field decisions.

Emergency tarping matters for the same reason. If active openings or exposed areas remain untreated, interior water damage can continue while the claim is still being scoped. That turns a roof file into a larger property loss and creates preventable supplement pressure later.

Here’s a practical way to think about specialized services:

- Use ladder assist when access is the barrier: Steep pitch, height, fragile surfaces, and awkward setup conditions all qualify.

- Use emergency tarping when mitigation can’t wait: If the structure is open to continued weather intrusion, the right response is stabilization first.

- Use specialist documentation when the roof drives the claim: You need full elevations, clear test-area photos where appropriate, and measurements the desk side can effectively use.

- Use certified safety equipment, not hope: Proper fall protection isn’t optional on the right assignments. Gear such as fall protection with dual hooks and rated capacity reflects the standard of preparation these inspections require.

The field side of this topic is easier to understand when you watch actual roof and damage conditions in context.

What strong operators do differently

Strong claims teams don’t treat every inspection as if the same resource can solve it. They separate routine access from specialized access early. They also write assignment instructions that tell the field what “complete” means.

Unsafe access should never be solved with optimism. It should be solved with the right resource.

If you want faster files, don’t pressure adjusters into risky inspections. Build a response model that gets the correct inspection capability to the property without delay.

Checklists for Seamless CAT Claim Collaboration

When CAT handling bogs down, it usually isn’t because people stopped working. It’s because coordination got loose. Field assignments go out with thin instructions. Desk adjusters expect photos they never requested. Homeowners prepare for one kind of visit and get another.

That coordination gap becomes more obvious on high-risk structures. AdjusterPro’s CAT adjuster guide notes that rising disaster frequency has amplified the need for rapid, safety-focused inspections and cites industry data showing carriers using specialized partners for emergency tarping and steep-roof photo documentation have reduced claim cycle times by up to 40 percent post-hurricane. The lesson isn’t just “use more vendors.” It’s “use the right partner with a defined operating playbook.”

Checklist for carriers and desk adjusters

Use this list before assigning high-volume property work to any independent field resource or specialized inspection partner.

- Confirm scope discipline: Require a written inspection standard. You want to know what gets photographed, measured, noted, and escalated.

- Ask about high-risk access capability: If the assignment includes steep roofs, tall elevations, tree impacts, or unstable access, verify that the partner is set up for that work instead of treating it as an exception.

- Set reporting expectations in advance: Require organized photo labeling, room-by-room or elevation-based documentation, and estimate support that fits your workflow.

- Define communication intervals: Decide when status updates are due. Silence creates duplicate calls and false escalations.

- Establish mitigation triggers: Spell out when the field should recommend or coordinate emergency protection to prevent further damage.

- Require estimate compatibility: If your team works in Xactimate, don’t accept vague scopes that someone else has to rebuild later.

- Audit file usability, not just turnaround: Fast uploads aren’t enough. Check whether the desk adjuster can review the claim without calling the field back.

- Review logistics readiness: Ask how the partner handles route density, weather delays, access restrictions, and occupied properties.

- Check simple field organization tools: Operational readiness often shows up in ordinary details, including how documents, photos, and site notes are organized. Even basic storage systems like a wide mesh pocket hanging holder for file organization point to whether the operation values order.

Checklist for homeowners before the inspection

Policyholders can help the inspection go faster and cleaner without trying to “adjust” the claim themselves.

Document visible damage early

Take your own photos before temporary changes occur, as long as it’s safe to do so.Make access easier

Open gates, secure pets, and clear pathways to damaged rooms or exterior areas if possible.List what changed after the event

A short written list helps. Include leaks, stains, broken materials, fallen limbs, detached gutters, or interior areas that worsened after rainfall.Gather claim and policy information

Keep contact details, claim number, and any mitigation invoices or receipts ready.Don’t climb the roof

Homeowners trying to verify damage themselves often create a second problem.Ask what happens next

At the end of the visit, ask who reviews the file, whether more information is needed, and what the next communication step will be.

The collaboration habit that pays off

The best CAT files start with alignment before anyone arrives on site. That means the carrier knows what it wants, the field knows what complete looks like, and the homeowner knows what to expect. Most delays people blame on “storm volume” are really handoff failures.

How Fox Claims Delivers Clarity in Real-World Scenarios

Operational value shows up fastest in messy files. Not ideal files. Messy ones.

Here are three common scenarios claims leaders run into during CAT response, and why specialized field support changes the outcome.

Scenario one with widespread hail and too many steep roofs

A hail event hits a dense neighborhood of homes with steep rooflines and limited driveway access. The carrier has adjusters in market, but several properties require more than a standard walk-around and ladder setup. If every adjuster tries to solve roof access alone, inspections slow down and documentation quality starts to vary.

The better approach is to split the work. The adjuster keeps claim ownership and coverage focus. The specialized inspection team handles the difficult access, captures the roof condition thoroughly, and returns a documentation package the desk side can review without gaps.

That model helps because it removes the bottleneck from the hardest part of the assignment. Instead of asking one person to be scheduler, estimator, climber, photographer, and safety officer on every file, you narrow the field task to the right expertise.

Scenario two with a tree impact and hidden scope questions

A tree-on-house loss looks straightforward from the street. Then the inspection reveals roof damage, fascia issues, wet insulation, ceiling staining, and potential hidden damage around the impact point. Files like this often turn into supplement magnets when the first inspection only captures the obvious.

A specialized field partner adds value here by producing a tighter damage narrative. The goal isn’t extra commentary. It’s complete visual proof and a cleaner scope path. Good photo sequencing, closeups of impact areas, clear interior documentation, and precise measurements give the desk adjuster enough to make decisions without guessing at what the field saw.

Even in unusual losses, the same operational rule applies. A claim moves faster when the file is organized. Whether it’s photos, mitigation notes, or leak tracing support tools like a fluorescent coolant leak detection solution, the underlying principle is visibility. Hidden issues become expensive when nobody documents them early.

Better documentation doesn’t just support payment. It reduces argument later.

Scenario three with post-storm emergency stabilization

After a wind event, some properties don’t need a complicated coverage analysis first. They need protection from the next rain. If the roof covering is compromised or an opening is active, waiting for the full claim cycle to run before addressing mitigation can worsen the loss.

In those situations, the specialized partner’s role is immediate stabilization followed by disciplined documentation. That sequence matters. If tarping occurs without photos, the desk side loses valuable pre-mitigation evidence. If photos happen without timely stabilization, the structure may keep taking on water.

What works in practice is a combined field response. Stabilize first when necessary, document thoroughly, report quickly, and hand the desk adjuster a file that supports action.

Those aren’t glamorous wins. They’re operational wins. And in catastrophe response, operational wins are what keep claim volume from becoming claim drift.

Frequently Asked Questions About CAT Claims

What’s the difference between an independent adjuster and a public adjuster

An independent adjuster is typically assigned by an insurance carrier or adjusting firm to inspect and handle claims on the carrier’s behalf. A public adjuster represents the policyholder, not the insurer.

That distinction matters because people often hear “independent” and assume neutral in the everyday sense. In claims operations, independent usually refers to employment and assignment structure, not to whom the adjuster represents in the claim.

How are claims prioritized after a catastrophe

Carriers usually prioritize based on severity, safety, habitability, accessibility, and the risk of ongoing damage. A home with active water intrusion or major structural concerns will generally need faster handling than a minor exterior-only loss.

Within that framework, routing also depends on claim type. Some files can move through standard field inspection channels. Others need specialized inspection support because access, roof conditions, or mitigation needs make a routine assignment unrealistic.

What should I do if I disagree with the adjuster’s assessment

Start by asking for clarity, not conflict. Find out what damage was included, what wasn’t, and whether the issue is scope, causation, pricing, or coverage.

For carriers and desk adjusters, disagreements often reveal a documentation problem. For homeowners, they often reveal a communication problem. Either way, the next step is the same. Gather the relevant photos, estimates, invoices, and repair observations, then ask for a formal review of the specific disputed item rather than making the disagreement general.

How do drones and software support a cat claims adjuster

Technology helps most when it reduces blind spots and speeds up documentation flow. Drones can assist with visual capture on some properties. Mobile tools help the field upload photos and notes immediately. Estimating software such as Xactimate helps standardize repair logic and supplement review.

None of that replaces judgment. A strong CAT file still depends on someone knowing what they’re looking at, what they can safely access, and what needs escalation.

Is CAT adjusting still a strong career path

Yes, especially for people who can handle field pressure, variable deployment conditions, and technical property work. The broader employment category for claims adjusters, appraisers, examiners, and investigators is projected to decline 5 percent from 2024 to 2034, but the role remains important because catastrophe demand continues. The median annual wage was $76,790 as of May 2024, total employment stood at 365,300 jobs, and about 21,600 openings are expected each year from retirements and turnover, according to the U.S. Bureau of Labor Statistics occupational outlook for adjusters.

What’s the biggest mistake in CAT operations

Treating every property like a routine inspection. Catastrophe claims reward fast action, but they punish generic handling. The right file path depends on site conditions, damage type, access risk, mitigation urgency, and documentation quality. Teams that recognize those differences early usually deliver better outcomes for both the carrier and the policyholder.

When your CAT response depends on accurate field data, safe access, and fast emergency support, Fox Claims Consultants LLC provides the specialized property inspection help that keeps difficult claims moving. From steep and tall roof inspections to ladder assist, storm and tree damage assessments, emergency tarping, and precise estimating support, Fox Claims gives carriers, desk adjusters, IAs, and TPAs a dependable boots-on-the-ground partner when conditions are demanding and timelines are tight.

Leave a Reply