Yes, homeowners insurance often covers tree damage, but the answer isn't always a simple "yes." It all comes down to one critical question that every insurance adjuster will ask: what did the tree hit?

If a storm knocks a tree over and it lands on your house, garage, or even a fence, your policy is designed to kick in and help. But if that exact same tree falls and lands in an empty part of your yard? You'll almost certainly be paying for the cleanup yourself.

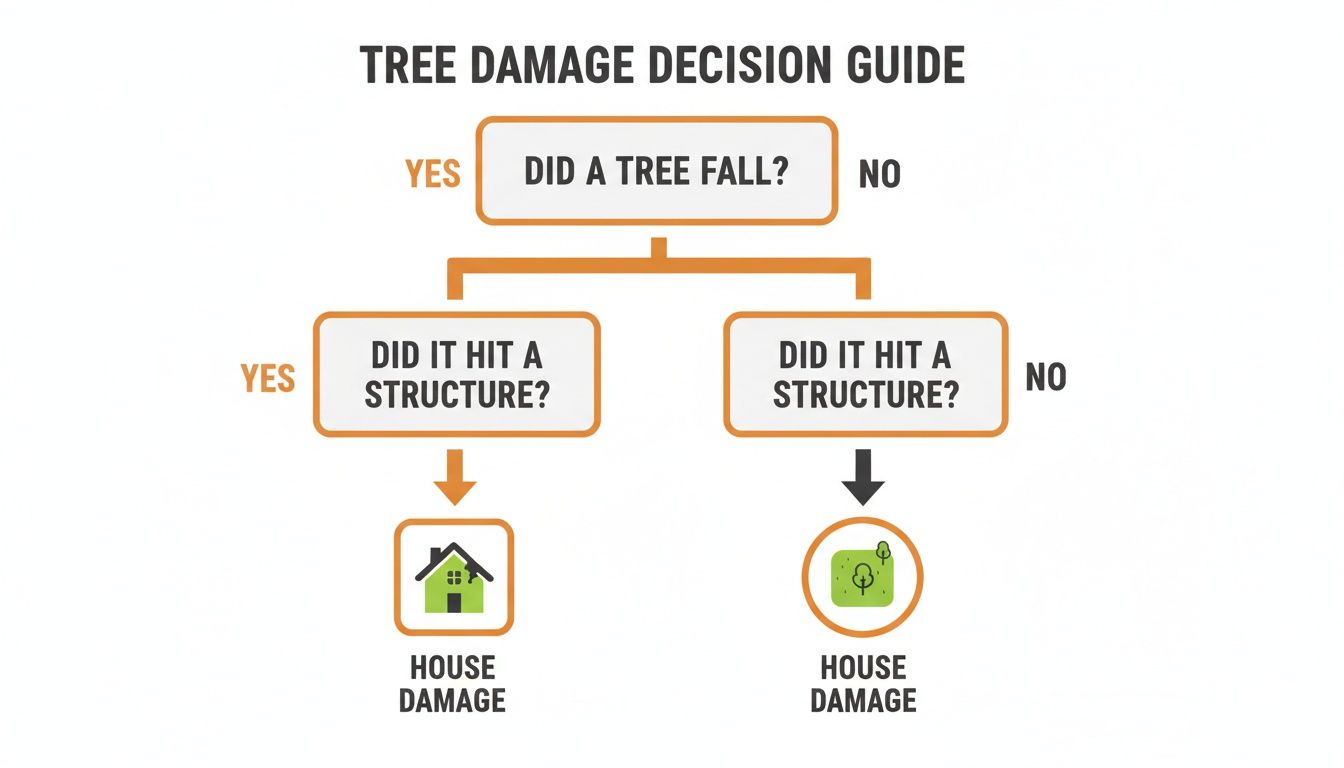

Your Policy and Fallen Trees: The Essential Rules

It helps to think of your homeowners insurance as a shield for your covered structures, not for your entire property or your landscaping. For a claim to be valid, two things generally need to happen.

First, the tree has to fall because of a covered peril—a specific, sudden event your policy is written to protect you against. This usually includes things like a windstorm, a lightning strike, or the heavy weight of ice and snow.

Second, the falling tree must damage a covered structure. If the peril (the wind) causes the tree to damage your house, the coverage is triggered. If the tree just falls in the yard, the chain of events stops there, and so does the insurance coverage.

This simple flowchart breaks down the basic logic every insurance company follows.

As you can see, coverage really hinges on that point of impact. It’s a crucial distinction that many homeowners only discover after a storm.

Tree Damage Coverage Scenarios at a Glance

Navigating these rules can feel confusing in the heat of the moment. This table simplifies the most common scenarios you might face.

| Scenario | Is Damage to Your House Covered? | Is Tree Removal Covered? |

|---|---|---|

| Your tree falls on your house. | Yes | Yes, up to your policy's sub-limit. |

| Your neighbor's tree falls on your house. | Yes | Yes, up to your policy's sub-limit. |

| A tree falls in your yard and hits nothing. | No | No |

| A tree falls and blocks your driveway. | No, unless it also damaged a structure. | Maybe, some policies offer a small amount for removal if it blocks access. |

| A tree falls on your detached garage or shed. | Yes | Yes, up to your policy's sub-limit. |

Remember, these are general guidelines. The specific language in your policy is what ultimately determines your coverage.

Understanding Tree Debris Removal Limits

Here's where things can get frustrating for homeowners, even with a covered claim. While your policy will pay to repair the damage to your roof or garage, it provides very little for the actual cost of removing the tree that caused the damage.

Most standard homeowners policies cap the payout for tree debris removal at a small, set amount—typically just $500 to $1,000 in total. You can learn more about how these typical homeowners insurance limits work and why they often fall short.

This is a common pain point. The cost to remove a huge, mature oak tree that has crashed through your roof can easily run into thousands of dollars. The insurance company will cover the roof repairs (minus your deductible), but that tiny $500 allowance for tree removal will leave you with a massive out-of-pocket expense to get the wood hauled away. It’s a gap in coverage that catches too many people by surprise.

Decoding Your Policy for Tree Damage Coverage

Think of your homeowners insurance policy less like a single umbrella and more like a set of specific tools, each designed for a different job. When a tree comes crashing down, your insurance company doesn’t just hand you a blank check. Instead, they match each part of the damage to a specific coverage in your policy.

Knowing how these coverages work is the first step to understanding what you're actually owed.

The first and most important tool is Coverage A (Dwelling). This is the heart of your policy, built to cover the physical structure of your house itself. If a massive limb punches through your roof, shatters a window, or damages your siding, Coverage A is what pays to put it all back together.

Beyond Your Home's Four Walls

But what happens when the tree misses your house entirely and crushes your fence or a detached garage? That’s where Coverage B (Other Structures) kicks in.

This part of your policy is specifically for structures on your property that aren't physically attached to your main house. Think of things like:

- Detached garages

- Sheds

- Fences

- Gazebos or pergolas

The damage is still covered because the tree hit insured property, but the funds come from a different bucket within your policy. Likewise, if that same tree breaks a window and falling debris destroys your laptop and couch, Coverage C (Personal Property) is what helps you replace those ruined belongings.

What Happens If You Can't Live There?

Sometimes the damage is so bad that your home simply isn't safe to live in. A tree that has compromised your roof’s integrity can leave your entire house exposed to the elements, forcing you to move out while repairs are made.

This is the exact scenario that triggers Coverage D (Additional Living Expenses). This coverage reimburses you for necessary costs like hotel stays, meals, and even laundry services—the extra expenses you have to pay because you can’t be in your home.

The Misunderstood Part of Your Policy

Finally, we have to talk about the tree itself—specifically, getting it off your house and hauled away. This is covered under a provision for Debris Removal, and it's one of the biggest sources of frustration for homeowners.

Most policies have a surprisingly low cap for debris removal, often just $500 to $1,000. That limit applies even if the actual bill for a crane and a specialized crew to safely remove a massive oak is several thousand dollars.

The insurance carrier’s main job is to fix the damage to the structure. Removing the tree that caused the damage is a secondary concern with its own, much smaller, limit. Because these details are buried deep in your policy, getting professional insurance claims assistance can make all the difference, ensuring you know exactly what you're owed and don't leave money on the table.

Common Gaps in Your Tree Damage Coverage

Knowing what your policy covers is one thing. Knowing what it doesn't is where homeowners can get into real trouble. It’s absolutely crucial to understand the common gaps and exclusions in your policy to avoid the shock of a denied claim.

It all boils down to a simple rule we see trip people up all the time: no impact, no coverage.

That huge oak tree that fell in your yard during a storm? If it landed harmlessly on the grass without hitting your house, your shed, or your fence, it's not an insurance event. It might be a massive cleanup headache, but the cost of removing it is yours alone.

The Problem of Neglect

Here’s another major exclusion that catches homeowners completely off guard: neglect. Insurance is designed for sudden and accidental events, not problems that have been brewing for months or years.

If a tree on your property was visibly rotting, diseased, or leaning precariously and you did nothing about it, your insurance carrier can—and likely will—deny the claim. They'll argue the damage wasn't accidental; it was preventable. This is precisely why getting a professional opinion after a loss is so important to determine the true cause. You can get a sense of what the experts look for by learning more about professional storm damage property inspections.

Landscaping and the Tree That Caused It All

What about your prized landscaping that got crushed? Most people are surprised to learn how limited this coverage is.

Some policies do offer a small amount for landscaping—often capped at just 5% of your dwelling coverage, with a per-plant limit of around $500. But here's the fine print: that coverage almost always excludes the very tree that fell and caused the damage in the first place.

This is a critical detail, and poor documentation is one of the top reasons we see these types of claims get denied. If you can prove a neighbor’s neglected tree was the cause, you might be able to recover your deductible, but that requires solid, indisputable proof.

The core principle is simple: your policy protects your home from the tree, but it doesn't protect the tree itself or, in most cases, the empty ground it falls on. Proactive care is always your best first line of defense against both tree-related risks and potential claim denials.

Navigating Disputes When a Neighbor's Tree Falls

When your neighbor’s tree comes crashing down onto your roof, the first question is always the same: who’s going to pay for this? The answer almost always comes as a surprise. In most situations, your own homeowners insurance policy is responsible for the damages, not your neighbor's.

This is because the law generally views a healthy tree toppled by a storm as an "Act of God." Your neighbor couldn't stop the hurricane-force winds or the lightning strike, so they aren't considered legally at fault. Your policy is designed to protect your home from these exact events, no matter where the tree came from.

But the whole situation flips if you can prove your neighbor was negligent.

The Critical Difference of Negligence

Negligence is the absolute game-changer in neighbor tree disputes. If the tree that fell was visibly dead, diseased, or unstable—and your neighbor knew about the risk but did nothing—the responsibility can shift right back to them. The key is proving they were aware of the hazard and chose to ignore it.

Think about it this way: their tree has been dead for a year, dropping huge branches and leaning dangerously over your property line. You've mentioned it to them, but they just shrugged it off. When that tree finally gives way and smashes into your house, their failure to act makes them liable for the damage.

In cases of proven negligence, your insurance company will still step up and pay your claim to get repairs moving. But then they'll go after your neighbor's insurance company for reimbursement through a process called subrogation.

Creating a Paper Trail Is Your Best Defense

If you’re worried about a hazardous tree on a neighbor's property, you need to be proactive. Verbal warnings are easy to deny or forget. You have to create a clear, undeniable record of your concerns before something bad happens.

Follow these steps to build an ironclad paper trail:

- Take Dated Photos and Videos: Document the tree’s condition over time. Capture clear images of dead limbs, rotting wood, a split trunk, or a dangerous lean toward your home.

- Get a Professional Opinion: This is a big one. Hire a certified arborist to inspect the tree and give you a written report confirming it's a hazard. An expert opinion adds serious weight to your claim.

- Send a Certified Letter: Mail your neighbor a formal, polite letter detailing your concerns. Include copies of your photos and the arborist's report. Sending it via certified mail with a return receipt gives you legal proof that they received your warning.

This is exactly the kind of documentation your insurer needs to successfully pursue a subrogation claim. A successful subrogation gets your insurance company’s money back, and just as important, it often means you get your deductible refunded. This process shows exactly how does homeowners insurance cover tree damage in these complex liability fights.

Your Step-by-Step Action Plan After a Tree Falls

The sound of a tree crashing into your home is something you never forget. It's a moment of pure chaos and panic. But what you do in the minutes and hours that follow can make all the difference — for your family’s safety and for the success of your insurance claim.

Your first move is always safety. Before you assess a single broken shingle, make sure everyone inside is okay. If the area is safe to move around in, check for immediate hazards like downed power lines, the smell of gas, or any signs that the structure is unstable. If you spot any of these dangers, get everyone out immediately and call 911.

Mitigate and Document the Damage

Once you've confirmed the area is safe, your next job is to prevent the problem from getting worse. In the claims world, we call this "mitigating your damages." If that tree punched a hole in your roof, you need to get it covered with a tarp to keep rain from pouring in and causing even more destruction.

Now, before you or anyone else moves a single branch, it’s time to become a crime scene investigator. Your smartphone is the most important tool you have right now.

- Take Wide Shots: Get pictures of the entire scene from different angles. You need to show the tree, where it came from, and how it’s lying on your property.

- Get Close-Ups: Go in tight on every single point of contact. Photograph the damaged shingles, the dented gutters, the cracked siding, and any destruction you can see inside the house.

- Record Video: A slow, narrated walk-around video is invaluable. It provides context that photos can miss and captures the immediate aftermath in real-time.

This evidence is not a suggestion; it’s essential. It creates a clear record of the damage before any cleanup begins, which is critical for your claim.

Notify Your Insurer and Call in Professionals

With your initial photos and videos secured, it's time to call your insurance company and report the claim. Stick to the facts and give them a clear picture of what happened. They'll assign an adjuster, but getting your own independent, expert assessment is a smart next move.

A professional inspector can provide a detailed, unbiased evaluation of the damage—including issues that aren't immediately obvious. This expert report is essential for ensuring your claim accurately reflects the full scope of necessary repairs.

This is especially critical in storm-prone states. In Texas and Florida, for instance, tree-related claims have surged right alongside lightning incidents, with 4,490 and 5,339 claims respectively in recent years. A timely, thorough inspection from an expert can also spot opportunities for subrogation if a neighbor’s negligence was a factor—a key piece of understanding how does homeowners insurance cover tree damage.

Engaging a specialist ensures every detail is captured, helping you secure the fair settlement you need to get your home back to the way it was. For serious damage, you need a team that knows how to handle complex claims. You can request an expert to look at your property right away with our tree service damage appointment request.

Frequently Asked Questions About Tree Damage Claims

When a tree comes down, the questions start piling up almost as fast as the debris. It’s a stressful, chaotic moment, and even if you’ve read your policy, the real-world specifics can get confusing. We've seen it all, so here are the straight answers to the most common questions we hear from homeowners dealing with tree damage.

What If the Repair Cost Is Less Than My Deductible?

This is the first and most important financial question you should ask before picking up the phone to file a claim. Your deductible is simply the amount you’ve agreed to pay out of pocket before your insurance coverage kicks in.

Let's say a branch snaps off in a storm and cracks a window. You get an estimate for the repair, and the cost comes to $750. If your policy has a $1,000 deductible, filing a claim is a non-starter. You’d pay the entire $750 yourself because the cost never reached the threshold for your insurance to pay anything.

Filing that claim gives you a zero-dollar payout, but it does give you one thing you don't want: a mark on your claims history. Insurers track how often you file, and even a "zero-pay" claim can be a factor they use to raise your premiums at renewal time.

Think of your insurance policy as a safety net for major financial hits, not a maintenance fund for minor repairs. It’s there to protect you from catastrophic costs you can't handle alone.

This is why getting a professional damage estimate is so critical. An expert assessment from a team like Fox Claims Consultants gives you the hard numbers. It allows you to make a smart business decision by comparing the total repair cost to your deductible, so you know for sure if filing is the right move.

Does Homeowners Insurance Cover My Car If a Tree Falls on It?

We get this question all the time. The answer is a simple and absolute no. Your homeowners insurance policy will not cover your car, even if the tree was yours and the car was parked in your own driveway.

Damage to your vehicles is handled exclusively by your auto insurance policy. For this to be covered, you need to have comprehensive coverage, which is the part of an auto policy designed for non-collision events like theft, hail, and—you guessed it—falling objects.

Here’s a classic, messy scenario: A huge tree in your yard falls during a storm, crushing your detached garage and the car parked inside.

- The Garage: Damage to the garage is covered by your homeowners insurance, falling under Coverage B (Other Structures).

- The Car: Damage to the car is covered by your auto insurance policy, under your comprehensive coverage.

This means you’re filing two separate claims with two different insurers and paying two separate deductibles. It can get complicated fast. A professional can help you separate the damage to the structure from the damage to the vehicle, creating clean documentation that helps both claims move forward without getting tangled up.

Will My Insurance Rates Go Up After a Tree Damage Claim?

It's a fair question, and the honest answer is: it might. Filing a claim can signal increased risk to your insurance carrier, which could lead to a higher premium when your policy renews.

But it’s not a given. The impact on your rates depends on a few key factors:

- The Cause of the Claim: Insurers view claims differently. If the damage was from a massive hurricane that hit your entire region (a "catastrophic event"), it’s often treated differently than if it was an isolated incident that only affected your property.

- Your Claim History: One claim in ten years looks very different from three claims in two years. Frequency matters. A pattern of claims is a major red flag for insurers and a surefire way to see a rate hike or even a non-renewal notice.

- State Regulations: Every state has its own set of rules that dictate how and when an insurer can raise your rates after a claim.

You can't control how your insurer will re-evaluate your risk, but you can control the outcome of the claim you file. Ensuring your claim is professionally documented and accurately assessed maximizes your settlement. A full and fair payout puts the money you need in your hands for proper repairs, which can easily offset any potential, minor premium increase down the road. Make your one claim count.

How Do I Prove a Neighbor's Tree Was a Hazard Before It Fell?

If you want to hold your neighbor financially responsible for their tree falling on your property, you have to prove they were negligent. This takes more than just your word against theirs. Without solid proof, the event will almost always be considered an "Act of God," leaving you to file a claim on your own policy and pay your own deductible.

To build an undeniable case for negligence, you need to create a paper trail before the tree comes down.

Step 1: Send a Certified Letter

A text or a chat over the fence won't cut it in the eyes of an insurance company. You need to send a formal letter via certified mail with a return receipt requested. This U.S. Postal Service feature gives you legal proof that your neighbor received your formal notification of the hazard.

In the letter, be polite but firm. Clearly identify the tree and your specific concerns. For instance: "I am writing to formally notify you of the hazardous condition of the large pine tree on your property line, which has several large, dead branches overhanging my roof and appears to be leaning."

Step 2: Back It Up with Visual Evidence

Show, don't just tell. Your letter should include clear, compelling proof of the danger.

- Dated Photos: Take pictures from multiple angles showing the rot, dead limbs, split trunk, or lean. Use a timestamp function if you can.

- Video: A short video showing how the tree or its branches sway precariously in the wind can be incredibly effective.

This evidence makes the hazard real and difficult to ignore.

Step 3: Get an Arborist's Report

This is your ace in the hole. Hire a certified arborist to inspect the tree and give you a formal written report. An arborist is a tree health expert, and their professional opinion carries huge weight.

The report will officially document the tree's condition, diagnose any disease or decay, and give a professional assessment of its risk. A copy of this report, included with your certified letter, is the ultimate proof that your neighbor was made aware of a professionally-diagnosed hazard and failed to act.

When that tree eventually falls, this collection of documents—the return receipt, the photos, and the arborist's report—gives your insurance company everything it needs to successfully pursue your neighbor's insurance for the damages (a process called subrogation) and get your deductible refunded.

What if a Tree Just Blocks My Driveway?

This is a common gray area. If a tree falls and only blocks your driveway—without hitting your house, fence, or any other insured structure—your policy will generally not cover damage to the driveway surface itself.

However, many policies offer a small amount of coverage for debris removal if it blocks access to your home. This isn’t for fixing the pavement; it’s strictly for the cost of cutting up and hauling away the tree so you can get in and out.

This coverage is usually very limited, often capped at around $500. That might be enough for a small tree, but it likely won't cover the full expense of removing a massive oak that requires a crane and a full crew.

The key word here is access. If the tree is just lying in your yard, there's no coverage for removal. But if it's completely blocking your only way in or out, you may be able to claim that small removal benefit. Check your policy's specific language to be sure.

When a tree falls, the last thing you need is a prolonged and frustrating battle with your insurance company. At Fox Claims Consultants LLC, we provide the expert inspections, detailed documentation, and rapid response needed to move your claim forward with confidence. Whether you need an emergency tarp to prevent further damage or a comprehensive assessment to ensure a fair settlement, our team is ready to help. Get the professional support you deserve by visiting https://foxclaimsconsultants.com.

Leave a Reply