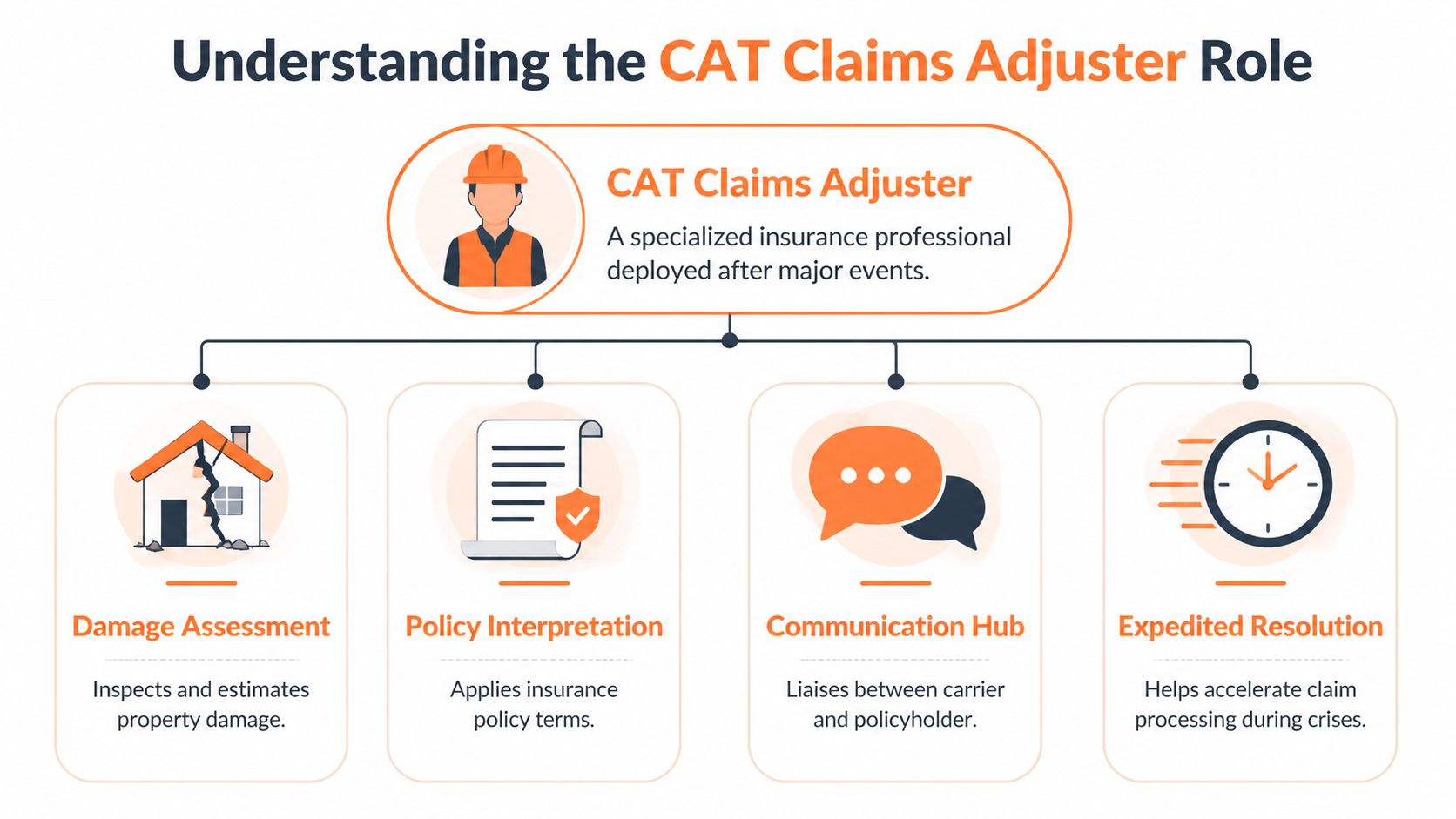

A CAT claims adjuster is a specialized insurance professional who assesses property damage from major disasters such as hurricanes, floods, tornadoes, hail, wind, and fires so claims can move toward settlement quickly. In catastrophe deployments, these adjusters often handle 100 to 200 claims per deployment, compared with 20 to 30 active claims for a daily adjuster, which is why they become central to recovery when a storm overwhelms normal claim operations.

If you're reading this after a storm, you already know the feeling. Phones are ringing, policyholders want answers now, roads may still be blocked, roofs are unsafe to walk, and every delay raises the chance of more damage, more dispute, and more frustration.

People often ask, in plain terms, what is a cat claims adjuster and why does the role matter so much? The short answer is that CAT adjusters bring structure to disorder. They step into high-volume, high-pressure losses and turn scattered facts into documented, defensible claim files.

In practice, they don't work alone. The strongest catastrophe response happens when field CAT adjusters, desk CAT adjusters, and specialized inspection partners each do the part they are best equipped to do. That's what keeps a storm claim moving instead of stalling in the usual choke points: unsafe access, poor photo sets, incomplete scope notes, and delayed decisions.

When the Storm Hits First Responders for Property

The first hours after a major storm rarely look organized. A neighborhood wakes up to shingles across yards, water stains spreading across ceilings, a tree through a garage, and a line of voicemails from worried insureds asking the same thing: what happens next?

For carriers, the problem is immediate and operational. One weather event can create more losses than a local team can absorb. Staff adjusters already carrying normal claim volume suddenly have catastrophe files stacked on top of daily work. Homeowners don't care about that math. They want someone who can inspect the damage, explain the process, and help move the claim.

That's why CAT adjusters are often the closest thing property insurance has to first responders. They don't restore power, and they don't remove debris. They do something just as important for the claim. They establish what happened, what was damaged, what the policy may respond to, and what needs to happen now to prevent the loss from getting worse.

What their arrival changes

When a CAT adjuster reaches a loss site, the file starts becoming usable. The inspection creates a factual base for every later decision. Coverage review gets sharper. Repair conversations get grounded. Temporary mitigation can be prioritized. Desk teams can finally work from something real instead of speculation.

Practical rule: The first solid field documentation often determines whether a catastrophe claim moves cleanly or turns into a weeks-long argument.

That field reality matters even more on steep roofs, multi-elevation structures, or homes with tree impact where access isn't simple. Those are the losses where poor inspection practice creates bad estimates and bad estimates create bad outcomes.

A lot of claims professionals learn this the hard way. The claim that looks straightforward on first notice often becomes complicated the moment someone has to inspect a slick, damaged roofline or verify hidden storm impact. Teams that prepare for that complexity early tend to keep control of the file better than teams that wait until the reinspection phase.

For readers looking at storm response tools and field readiness through a practical lens, even operational gear discussions such as this property field equipment listing reflect the same underlying truth. Catastrophe work depends on getting reliable information from unstable conditions, fast.

What Is a CAT Claims Adjuster Really

A CAT adjuster is not just an adjuster who happens to be busy. The role is built for surge conditions. These professionals are deployed after major disaster events to evaluate loss, apply policy terms, estimate damage, and help push claims toward resolution under compressed timelines.

The simplest way to understand the role

If you want a practical analogy, think of a CAT adjuster as an emergency room doctor for property. The job isn't to solve every problem in one moment. The job is to stabilize the situation, identify the damage accurately, document what matters, and move the file toward the right next decision.

That means four things usually happen fast:

- Damage gets assessed: The adjuster inspects the property, documents visible conditions, and identifies affected components.

- Policy terms get applied: The loss still has to be adjusted to the contract, not just to the damage.

- A scope gets built: Repair direction starts with a defensible estimate and solid documentation.

- Communication gets coordinated: The adjuster becomes a working link between policyholder, carrier, contractors, and internal claim staff.

Why the role is different from ordinary field adjusting

CAT work isn't just about inspection skill. It's about performance in disruption. Roads may be blocked. Hotels may be scarce. Insureds may be displaced. Utilities may be out. The adjuster still has to build a file that can withstand scrutiny.

The income potential reflects the intensity and volatility of that work. During the 2017 hurricane season, top-performing independent CAT adjusters made $65,000 to $100,000 in a single month, and many drive 35,000 to 40,000 miles yearly chasing storm assignments, according to AdjusterPro's catastrophe adjuster income overview. That same source notes 21,600 annual openings are projected even as the broader adjuster field declines, which tells you how persistent catastrophe demand remains.

High earnings in CAT work usually come packaged with travel, pressure, uneven living conditions, and very little room for sloppy documentation.

What good CAT adjusting looks like

Good CAT adjusting is disciplined, not dramatic. The best adjusters don't just move quickly. They know where speed helps and where speed creates rework. They document enough to support the estimate, communicate clearly enough to reduce confusion, and avoid guessing when a specialist needs to be brought in.

Poor CAT adjusting looks different. It leans on weak photos, rushed notes, incomplete roof observations, and broad assumptions about causation. Those files may look closed for a moment. Then supplements, complaints, reinspections, and coverage disputes bring them right back.

That difference is why this role matters so much inside the insurance ecosystem. A strong CAT adjuster doesn't just inspect damage. They protect claim quality while the whole system is under stress.

Anatomy of a CAT Deployment A Day in the Life

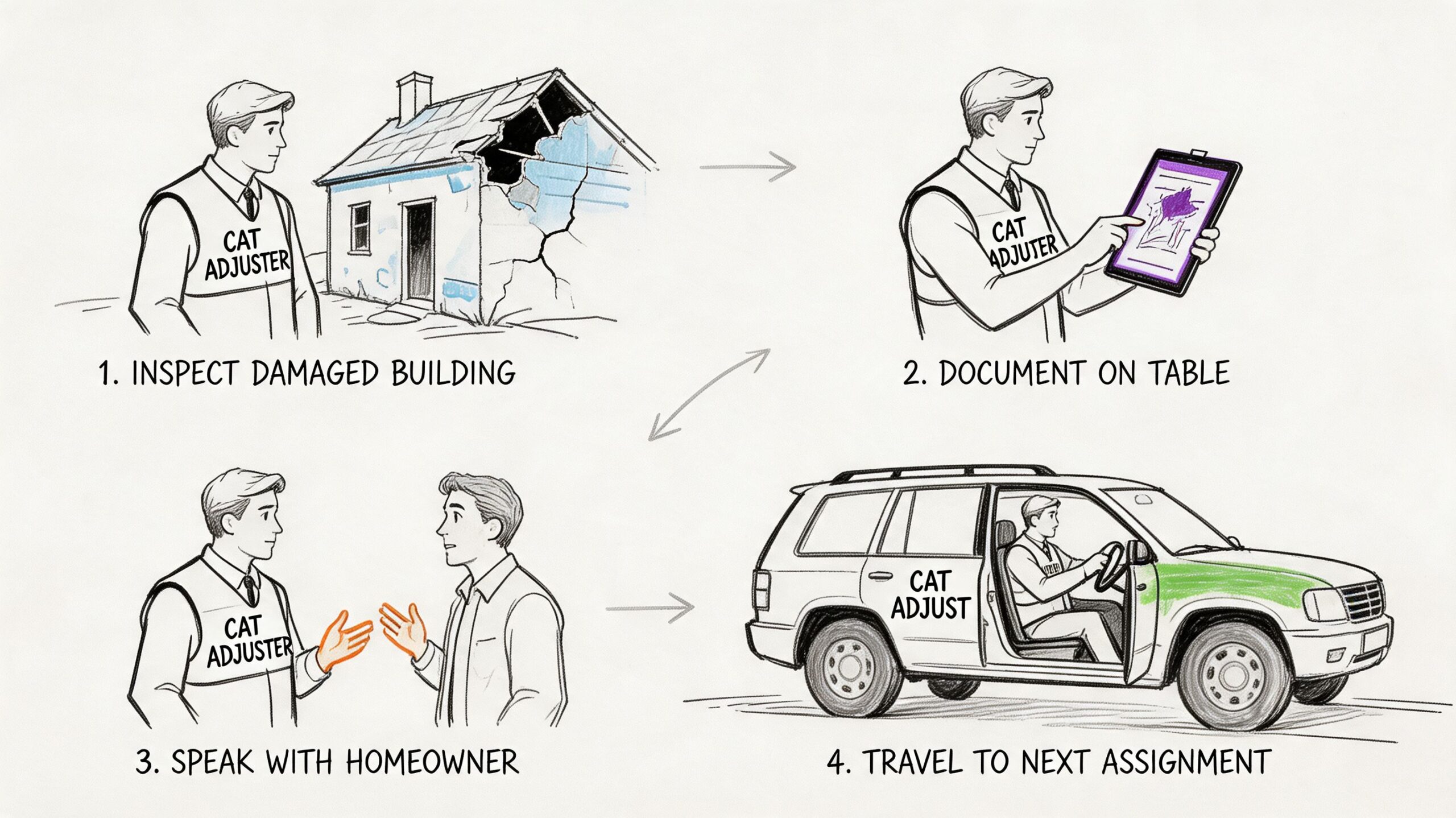

The deployment usually starts with a call, not a schedule. A major event lands, claim volume spikes, and adjusters are mobilized into places where infrastructure may still be unstable and the insured population needs immediate contact.

A field CAT packs for function, not comfort. Ladders, boots, PPE, chargers, moisture tools, claim software access, backup paper notes, and enough logistics planning to work through bad cell coverage and long days. Once deployed, the routine gets repetitive in the way only hard work does. Drive. Inspect. Photograph. Explain. Upload. Write. Repeat.

What the day actually feels like

Morning starts with assignment review and route planning. The best adjusters don't just sort by address. They think about access, severity, daylight, occupied versus vacant property, and whether a file is likely to need specialist support.

By midday, the pace is physical and administrative at the same time. One property may need a straightforward exterior review. The next may involve a steep roof, interior water mapping, detached structures, and a homeowner who hasn't slept well since the storm. The job requires technical judgment and people skills in the same hour.

Industry practice reflects that workload. CAT adjusters are deployed when carriers need help with sudden claim surges and often process 100 to 200 claims per deployment, compared with 20 to 30 active claims for daily adjusters. They are commonly paid on CAT pay, a performance-based structure that rewards fast closure, as described in BSA Claims' breakdown of CAT and daily adjusters.

Speed helps and speed hurts

The pressure to close files is real. So is the temptation to over-simplify a complicated loss. That's where deployment discipline matters.

A productive CAT day usually includes:

- Clear first contact: Set expectations early so insureds know what the inspection will and won't answer that day.

- Tight field documentation: Photos should prove condition, not just show that someone visited.

- Accurate handoff notes: Desk reviewers need context, not a pile of unlabeled images.

- Escalation judgment: Unsafe access, structural concerns, or specialist damage patterns should be flagged immediately.

You can see the field rhythm in this short clip of catastrophe adjuster deployment work.

Late evening is often when the second shift begins. Notes get cleaned up, estimates get built or reviewed, and files are pushed forward before the next day starts. This is also where support tools matter. Teams that rely on clean image capture and durable documentation workflows generally create fewer downstream arguments, which is why practical equipment choices like this field camera housing option mirror a real need in catastrophe work.

The claim isn't truly inspected until the documentation is clear enough for someone off-site to understand exactly what you saw.

CAT vs Desk vs Public Adjuster Key Differences

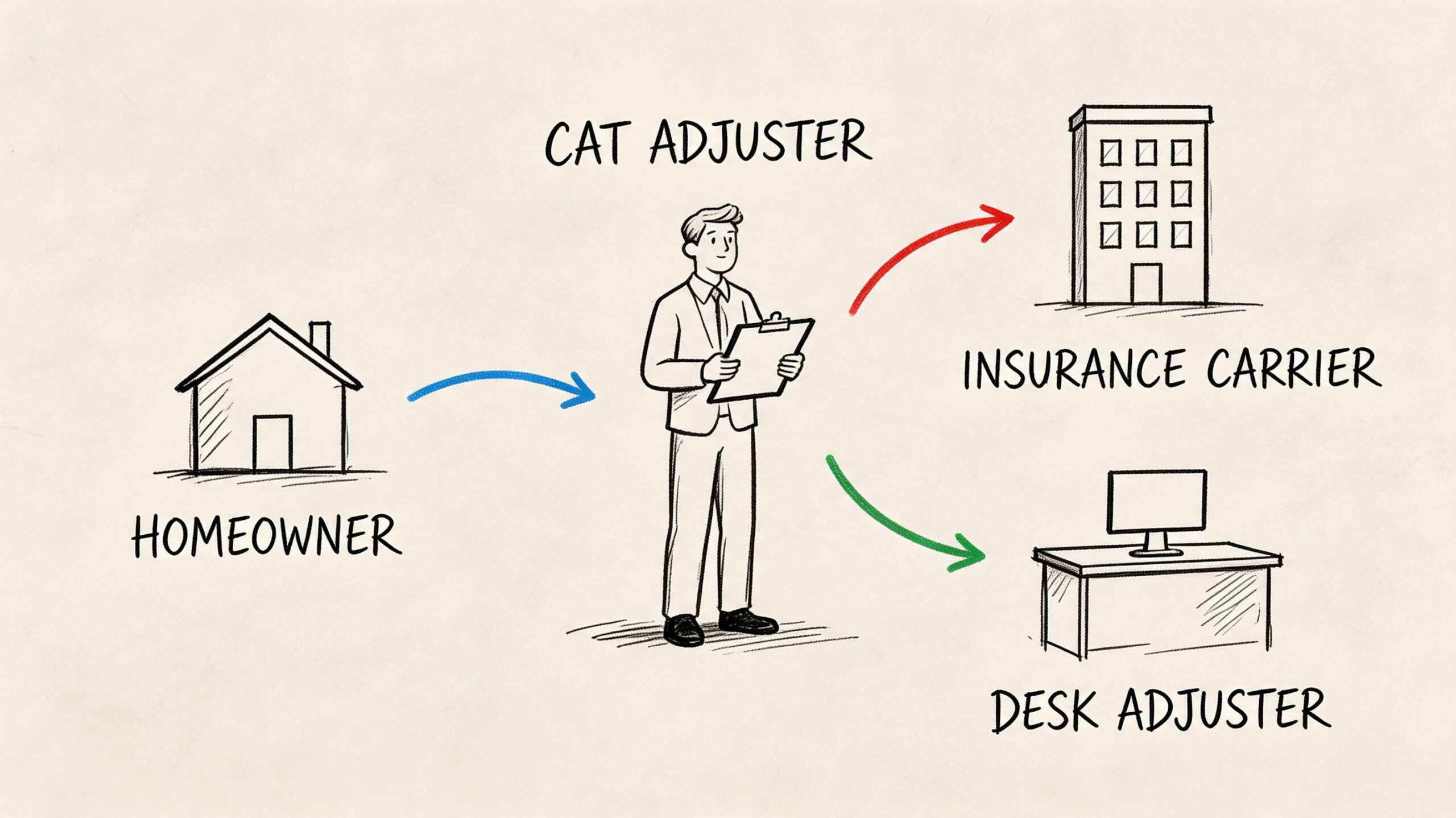

People outside claims often hear "adjuster" and assume every role does the same thing. In catastrophe response, that misunderstanding causes confusion fast. The field CAT, the desk CAT, and the public adjuster all touch the claim differently.

The biggest distinction is who they represent

A CAT adjuster working catastrophe files for a carrier or independent adjusting firm is there to inspect, evaluate, and move the insurance claim based on the policy and the documented loss. A desk CAT adjuster supports that same catastrophe process remotely. A public adjuster represents the policyholder, not the insurer.

The desk role deserves more attention than it usually gets. During catastrophe volume spikes, desk CAT adjusters work remotely to review files, verify field information, and finalize settlements, often handling 100 to 200 claims per deployment, according to Indeed's explanation of CAT adjuster roles.

Adjuster Role Comparison

| Adjuster Type | Who They Represent | Typical Environment | Primary Goal |

|---|---|---|---|

| CAT adjuster | Insurance carrier or assigned adjusting partner | Disaster zone, on-site inspections, field deployment | Document damage and move catastrophe claims forward |

| Desk CAT adjuster | Insurance carrier or assigned adjusting partner | Office or home, remote file handling | Review field data, verify documentation, finalize claim activity |

| Public adjuster | Policyholder | Field, office, negotiation settings | Advocate for the policyholder's claim presentation |

Where files stall

Trouble usually starts when people expect one role to do another role's job. A field CAT can gather facts from the loss site, but may not be the person issuing the final payment decision. A desk CAT can keep a large claim inventory moving, but can't safely inspect a storm-damaged steep roof from a laptop. A public adjuster can present the insured's view of the loss, but doesn't stand in for the carrier's adjustment obligation.

That's why catastrophe files move best when each role stays in its lane and communicates clearly across the file.

- Field CATs need usable access, good assignment instructions, and a way to flag issues early.

- Desk CATs need labeled photos, concise summaries, and documented reasons for estimate decisions.

- Public adjusters need timely responses and a claim file built on evidence rather than assumptions.

For teams thinking about field safety and claim support materials, operational readiness often extends beyond personnel to practical supplies such as these replacement filter materials used in protective equipment setups, especially when inspections happen around debris, damaged interiors, or post-event contamination concerns.

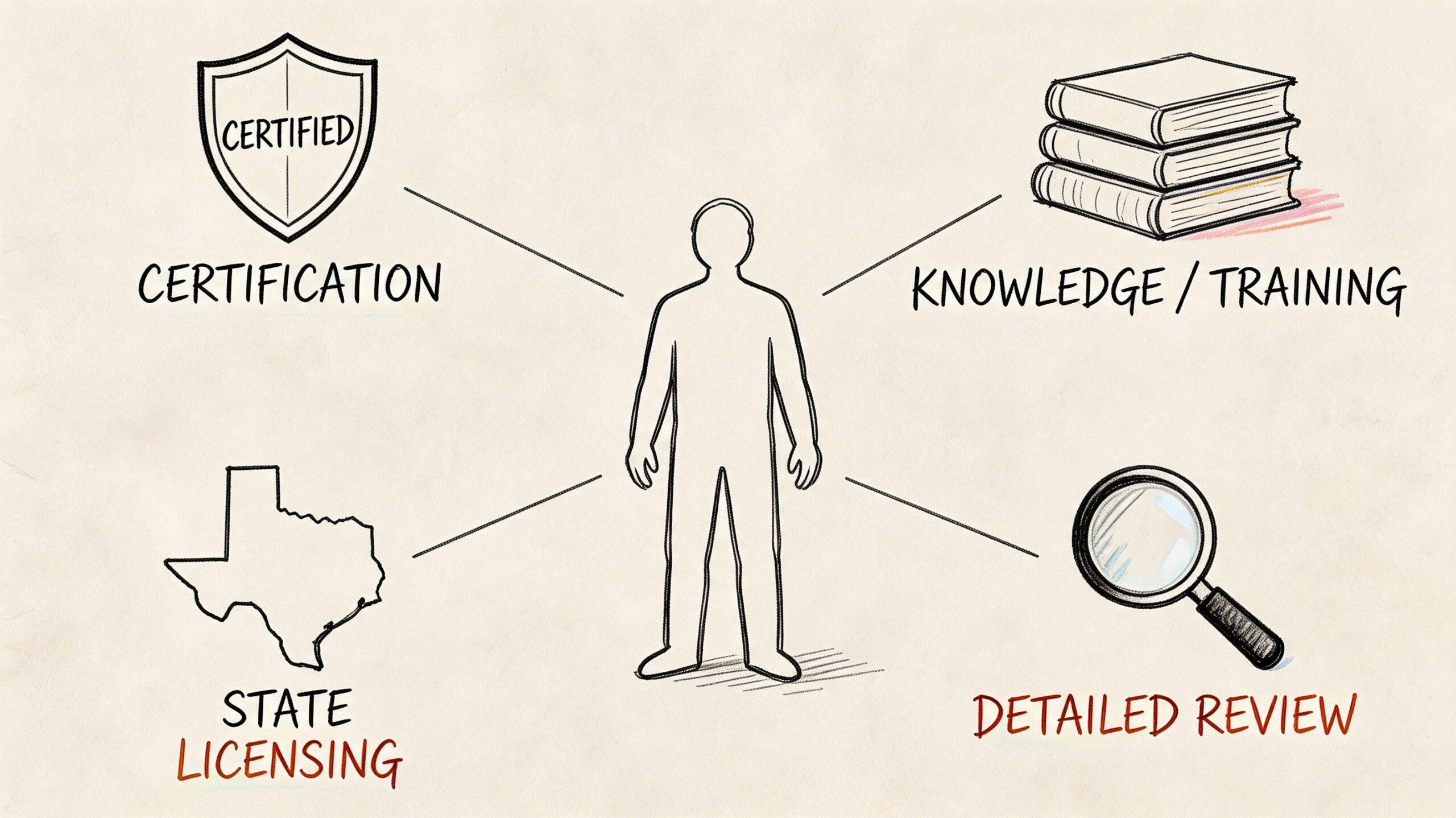

Qualifications and Certifications Beyond the Basics

A storm file can go sideways before the estimate is even written. The adjuster reaches a property with a steep, wet roof, a partially collapsed fence line, exposed wiring near the service mast, and an insured who wants answers on the spot. In that moment, licensing is only the starting point. Real CAT readiness shows up in judgment, field discipline, and the ability to pass clean information from the site to the desk without creating more risk.

Carriers need more than a licensed adjuster with estimating software. They need someone who can inspect safely, separate storm damage from pre-existing issues, document conditions in a way a desk CAT can act on, and recognize when the assignment calls for a specialist. That is where good field operations protect file quality. It is also where inspection partners such as Fox Claims add real value by taking on steep-slope, high-access, and other skill-sensitive work that should not be improvised in the field.

What competent catastrophe training includes

Strong CAT training covers policy interpretation and estimate writing, but the better programs go further. FEMA’s field guidance on post-disaster operations emphasizes safety awareness, incident conditions, documentation standards, and coordination across multiple responders in unstable environments, all of which mirror the pressures property adjusters face after major events (FEMA disaster field training and operations guidance). For property claims, that translates into roof hazard recognition, moisture and interior damage documentation, scene control, chain-of-information discipline, and clear escalation when conditions are unsafe.

The job also demands technical range. The National Association of Catastrophe Adjusters explains that CAT work often requires adjusters to handle multiple claim types, operate under compressed timelines, and maintain file quality despite surge volume (NACA overview of catastrophe adjuster work). That combination is why experienced CAT managers screen for field judgment as closely as they screen for licensing.

A good deployment model respects those limits. Field CATs gather site facts. Desk CATs convert those facts into decisions, reserves, coverage analysis, and payment activity. Specialized inspection partners handle the dangerous or highly technical portions of the inspection so the file does not depend on guesswork, poor photos, or someone taking a bad fall to finish an assignment.

The trade-offs that shape long-term performance

CAT work pays well because it is hard on people. Long deployment periods, weather exposure, travel, confrontation with stressed policyholders, and repetitive decision-making under volume all wear down performance. The Insurance Information Institute’s catastrophe reporting regularly shows how large weather events create sustained claim surges across entire regions, which means adjusters are often working in disrupted communities for extended periods rather than walking into a normal inspection environment (Insurance Information Institute catastrophe and severe weather resources).

Fatigue changes claim quality fast. Photo sets get thinner. Notes get vague. Safety calls get rushed. The better adjusters know when not to climb, when to ask for better access, and when to assign a specialist inspection instead of forcing a weak field decision into the file.

I have seen the opposite approach create expensive problems. A marginal roof inspection may save an hour today and cost weeks later when the desk adjuster cannot support scope, engineering gets pulled in late, or the carrier has to revisit the property.

A practical qualification check should cover the following:

- Field safety judgment: Ladder handling, fall-risk recognition, electrical awareness, and the discipline to decline unsafe access.

- Damage documentation skill: Photos, annotations, measurements, and notes that let a desk CAT evaluate the loss without filling in gaps.

- Multi-party coordination: The ability to work cleanly with desk adjusters, mitigation vendors, engineers, and specialized field partners.

- Operational discipline: File organization, communication speed, and follow-through under surge conditions.

- Visible professional credentials: On occupied loss sites, clear identification reduces confusion and helps insureds know who is there. That is why practical tools such as full-color personalized field ID badges are part of real CAT readiness.

The best CAT adjusters are not the ones who try to do every part of the job themselves. They are the ones who know their lane, document it well, and bring in the right support before a risky inspection turns into a bad claim outcome.

Working with CAT Adjusters A Guide for All Parties

The best catastrophe claims don't move fast because one person works harder. They move fast because the workflow is built correctly. Field inspection, desk handling, emergency mitigation, documentation, and communication all have to connect cleanly.

For carriers and TPAs

Catastrophe volume exposes bottlenecks quickly. The common failure points are predictable: unsafe access delays, weak photo sets, unclear file notes, lagging emergency service coordination, and a disconnect between what the field saw and what the desk received.

A better operating model uses specialized field support where the risk or technical demand is highest. In high-volume CAT situations, carriers and TPAs that integrate technology such as AI-driven damage assessment and partner with certified field inspectors for emergency tarping and high-risk inspections can reduce cycle times and prevent additional loss, according to NACA's overview of catastrophe adjusting and modern workflows.

In plain terms, that means assigning the dangerous and skill-sensitive work to the people equipped to do it, then feeding desk handling with clear, decision-ready evidence.

For desk CAT adjusters

Desk teams win or lose time based on field input quality. If the file comes in with organized photos, roof elevations identified, mitigation status documented, and clear notes on what was and wasn't accessible, desk review stays efficient. If the file comes in messy, the desk adjuster becomes a detective.

What works:

- Requesting specific evidence upfront: Ask for labeled elevations, interior room mapping, and close-ups that support causation discussions.

- Using a standard field-to-desk handoff: The same categories on every file reduce missed facts.

- Tracking closure pace carefully: Closure rates matter, but only when files are complete enough to stay closed.

What doesn't work is pushing for speed without defining the documentation standard first.

The desk side doesn't need more photos. It needs the right photos, identified correctly, delivered on time.

For homeowners

Homeowners don't need to know claims jargon to help a catastrophe file move. They do need to be organized and realistic about what the first visit is for.

A few practical habits help:

- Be available for contact: Missed scheduling delays everything.

- Share what changed after the storm: New leaks, fallen limbs, and emergency repairs all matter.

- Keep mitigation records: If tarping or temporary repairs were necessary, preserve invoices and photos.

- Don't force unsafe access: No claim is improved by having someone on a roof that shouldn't be walked.

Where specialized partners fit

The field-desk-specialist partnership is the overlooked engine in modern CAT response. The field adjuster may own the inspection assignment. The desk CAT may own the file progression. But when the loss includes a steep roof, tall structure, tree strike, or urgent mitigation need, a specialized inspection partner can remove the friction that slows everything down.

That partnership works best when expectations are narrow and practical:

- The CAT adjuster identifies the need for specialized field support.

- The inspection partner captures safe, thorough documentation and mitigation status.

- The desk adjuster receives organized evidence and can move the file.

Even basic site practices support this chain. Something as simple as carrying durable protective supplies, such as disposable inspection gloves for field handling, speaks to the larger reality that catastrophe response is physical work under imperfect conditions.

When that workflow is respected, claims don't just close faster. They close cleaner.

Conclusion: Bringing Order to Chaos

After a catastrophe, the claim file is only the visible part of the job. Behind it sits a coordinated response between the field CAT adjuster who sees conditions firsthand, the desk CAT who keeps the file moving, and the specialist who handles the dangerous or highly technical inspection work that should not be forced into a standard visit.

That coordination is what keeps storm claims from stalling.

A CAT claims adjuster brings structure to a bad situation. The best ones know how to sort severity, document loss cleanly, set expectations early, and decide when a specialist needs to step in. That decision matters. Sending the wrong person onto a steep roof, into a tree-impact scene, or onto a damaged structure creates risk, weak documentation, and reinspection costs that slow the entire claim.

For carriers, the lesson is straightforward. Build workflows that support clear handoffs between field, desk, and inspection partners. For homeowners, the takeaway is just as practical. Fast, accurate claim handling depends on safe access, timely updates, and records that support what happened at the property. For independent adjusters and TPAs, strong CAT performance often comes down to disciplined communication and knowing when to bring in qualified field support.

Storm chaos does not resolve itself. It gets handled file by file, decision by decision, by people who know their role and respect the handoff to the next one.

For those facing these specific challenges, specialized help is available.

When severe weather leaves you with steep-roof damage, tree impact, ladder-assist needs, or urgent temporary protection issues, Fox Claims Consultants LLC provides the certified field inspection support that helps claims move safely and efficiently. Their national team handles high-risk inspections, storm and tree damage assessments, emergency tarping, temporary repairs, and detailed photo documentation so carriers, desk adjusters, independent adjusters, and homeowners can make sound decisions faster.

Leave a Reply