A wind event hits on a Thursday night. By Friday morning, the desk has a queue full of roof losses, emergency mitigation requests, contractor estimates, and policyholders who want an answer now. Some files are straightforward. Many aren’t. The hard ones usually look the same: conflicting scopes, questionable cause of loss, inaccessible elevations, and a property that can’t be inspected safely by a standard field visit.

That’s where insurance restoration consultants earn their keep. Not as another layer of paperwork, and not as a substitute for the adjuster’s judgment. They step in when the claim needs technical clarity, controlled documentation, and a field process that won’t create more risk than it solves.

When Claims Get Complex You Need a Specialist

The worst claims days are rarely about volume alone. Volume is manageable when losses are simple. Trouble starts when the incoming file load includes steep roofs, tree impacts, partial interior water intrusion, disputed pre-existing damage, and contractors pushing a full replacement before anyone has pinned down what happened.

A carrier can’t move those files well on assumptions. A desk adjuster also can’t make a solid coverage or scope decision from a handful of cellphone photos taken from the driveway. In high-risk losses, the claim slows down because the basic facts are still unsettled.

That problem is getting more common, not less common. The insurance restoration sector has expanded alongside storm-related insured losses, which climbed from a long-term annual average of around $23 billion to $81 billion in 2020, $93.3 billion in 2021, and $98.8 billion in 2022, according to Qualified Remodeler’s report on insurance restoration contractors and AON loss data.

What the consultant changes on day one

A good consultant brings discipline to a chaotic file. That starts with access and evidence.

Instead of relying on secondhand descriptions, the consultant gets on site, documents conditions thoroughly, distinguishes obvious storm damage from age-related deterioration, and reports in a format the adjuster can act on. If the structure is hazardous or the roof is too steep for a routine inspection, the consultant’s value rises fast because safety and technical accuracy become linked.

Field reality: The claim usually doesn’t stall because people aren’t working. It stalls because the wrong people are trying to answer the wrong technical question.

In practical terms, the consultant becomes the party who narrows the dispute. Was the shingle uplift storm-related or long-term wear? Did the tree strike create hidden deck damage? Is that interior staining tied to this loss event or an older moisture path? Those aren’t paperwork questions. They’re inspection questions.

Why this matters to carriers and adjusters

The consultant’s job is to reduce ambiguity before ambiguity becomes cost. That means fewer avoidable reinspections, fewer unsupported line items, and less time spent sorting out competing narratives from contractors, policyholders, and field notes that don’t line up.

Some carriers also need rapid site stabilization support before the scope is finalized. Services associated with emergency property response, such as temporary site equipment and field support, fit into that early phase when the priority is preventing further damage while preserving a clean factual record.

When the file involves a difficult structure or a fast-moving dispute, a specialist isn’t a luxury. It’s how the claim gets back under control.

The Consultant's Role in the Claims Ecosystem

Most claims professionals understand adjusters and contractors. The confusion usually starts with the consultant because the role sits between inspection, technical analysis, and project oversight.

The simplest way to explain it is this. The staff or independent adjuster functions like a general practitioner. They evaluate the claim, apply policy handling judgment, and coordinate resolution. Insurance restoration consultants are the specialists called in when the case needs deeper technical inspection, better documentation, or tighter control over scope and repair execution.

What makes the role different

A consultant is not there to advocate one side’s financial position the way a public adjuster does. A consultant also isn’t there to sell repair work the way a contractor does. The consultant’s value is in technical neutrality, field accuracy, and report quality.

That neutral role matters most when the file has one of these traits:

- Conflicting damage narratives: The contractor says full replacement. The carrier file suggests repair. The photos are weak and nobody has documented the hard elevations properly.

- Access or safety issues: Tall slopes, fragile roofing materials, storm debris, or unstable areas make a routine inspection unreliable or unsafe.

- Scope drift risk: A claim starts as a localized roof issue, then expands into gutters, siding, interior finishes, code questions, and supplemental requests.

- Litigation sensitivity: The report may need to withstand formal scrutiny later, which means conclusions must be factual, documented, and supportable.

The best consultants don’t inflate or minimize damage. They narrow the file to what can be observed, documented, and defended.

Consultant vs. Public Adjuster vs. Contractor

| Role | Primary Allegiance | Core Function | Typical Goal |

|---|---|---|---|

| Consultant | The hiring party’s need for technical, factual evaluation | Inspect, document, analyze cause and scope, monitor work, support claim decisions | Bring clarity, control, and supportable documentation |

| Public Adjuster | Policyholder | Advocate the insured’s claim position | Maximize policyholder recovery within the claim process |

| Contractor | Repair business and project execution | Repair, restore, replace, and estimate work tied to construction scope | Secure and complete the restoration job |

That distinction saves time. If a desk adjuster hires the wrong type of partner for the wrong reason, the file usually gets louder instead of clearer.

Where consultants fit in the handoff chain

A consultant often enters after first notice of loss but before the scope hardens. That’s the sweet spot. Early involvement means the consultant can preserve site conditions, capture better photos, assess causation, and structure the report before outside estimates define the file.

In other cases, the consultant enters later, after supplements pile up or when repair progress raises workmanship or budget concerns. Then the assignment shifts from inspection into monitoring and verification.

A practical example is the use of field tools and site documentation support connected to restoration equipment and application workflows. The point isn’t the product itself. It’s that consultants work close to real repair conditions, not just paper estimates. They understand how the observed damage, proposed scope, and actual execution should line up.

What a good consultant does not do

A consultant shouldn’t replace the adjuster’s authority, write advocacy disguised as technical analysis, or issue conclusions beyond what the inspection supports.

That restraint is what gives the report weight. In difficult claims, a careful “not enough evidence to support that item” is often more useful than a broad opinion that won’t survive challenge later.

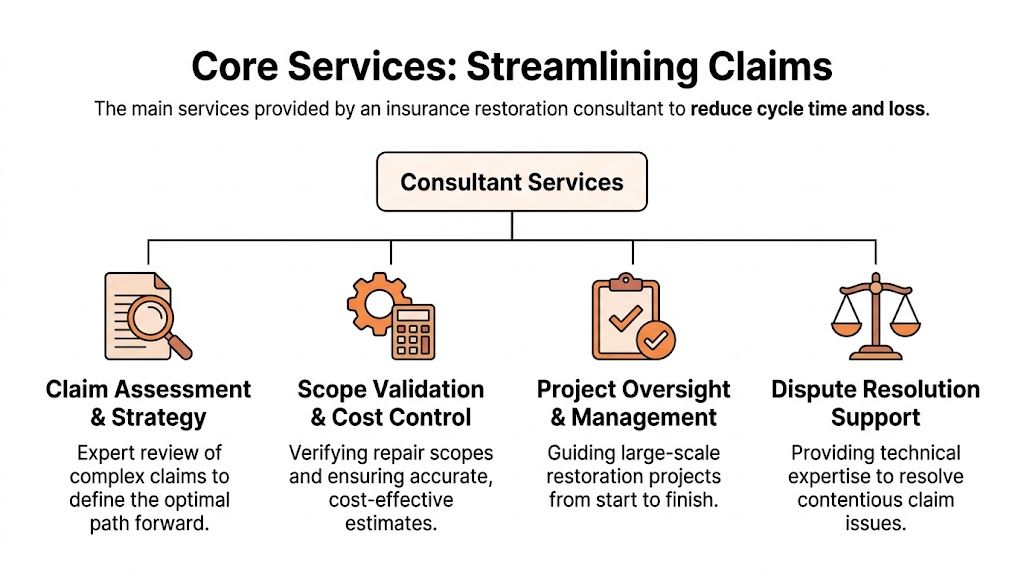

Core Services That Reduce Cycle Time and Loss

The value of insurance restoration consultants becomes obvious when you break the work into functions. Each service solves a different claim problem. Together, they tighten the file.

Here’s the service stack most carriers care about.

Cause of loss analysis

Weak claims handling often goes sideways. This typically happens when no one clearly separates storm-created damage from wear, deferred maintenance, installation defects, or older damage, making every later decision harder. Scope disputes grow from that initial uncertainty.

Consultants handle this by performing detailed inspections and documenting observable evidence tied to the claimed event. In roof losses, that may include ladder assists, slope-by-slope review, examination of ancillary components, and close photo documentation of impact, uplift, or moisture pathways. In interior losses, it often includes tracing the path of intrusion and identifying whether the damage pattern fits the reported cause.

The practical payoff is straightforward. Better cause analysis means fewer unsupported items move downstream as if they were established facts.

Supported estimating

A supported estimate is more than a line-item list. It’s an estimate tied back to field observations, measurements, photographs, and a clear explanation of why each repair element belongs in scope.

That matters because unsupported estimates invite friction from every direction. Contractors challenge them. Adjusters hesitate to approve them. Policyholders lose confidence when the number changes repeatedly. Consultants reduce that instability by building the estimate from the inspection record instead of from assumption.

A field partner may also note adjacent issues that affect proper repair sequencing, site protection, or temporary mitigation. In some assignments, related items like smoke-odor neutralizing materials and mitigation support become relevant when the consultant is evaluating restoration conditions beyond the obvious structural damage.

Photo documentation that actually answers questions

A large percentage of claim delay comes from bad photos. Not too few photos. The wrong photos.

Consultants who understand claim handling don’t just take pictures of damage. They capture context, access conditions, measurement references, and sequence. The report should let the adjuster understand where the damage is, what it affects, what it does not affect, and why the conclusion makes sense.

Practical rule: If the photo set can’t stand on its own without a long explanatory call, the documentation isn’t finished.

That type of documentation cuts back on avoidable follow-up. It also helps when the file changes hands internally and a new adjuster needs to understand the claim quickly.

A short video overview can also help frame the consultant’s role in the broader claims process:

Onsite project monitoring

Consultants transition from inspection into cost control. Once repairs start, a monitored project has someone verifying that the approved scope is followed, workmanship stays on track, and new requests are evaluated against actual site conditions.

That oversight has measurable impact. According to Insurance Restoration Consultants’ expert services overview, expert consultants reduce claim cycle times by 25 to 40 percent through accurate scoping and onsite project monitoring, and monitored projects often complete 15 to 20 percent under budget due to proactive bid analysis and workmanship verification.

That’s not surprising to anyone who has watched a large loss drift. Without oversight, supplement requests can become the default answer to every field surprise, whether justified or not.

Dispute support and technical reporting

Some files won’t settle cleanly no matter how strong the initial inspection is. When that happens, the consultant’s report becomes a stabilizing document. It gives the carrier or adjuster a factual basis for explaining the decision, revisiting a disputed item, or defending the file if it escalates.

The most useful reports are plain, direct, and limited to what the evidence supports. That style holds up better than broad narrative language. In complex claims, credibility is part of cost control.

Specialized Use Cases for High-Risk Claims

General property claims can often be handled with standard field processes. High-risk claims can’t. The inspection itself becomes a source of physical risk, claim error, or both. That’s where insurance restoration consultants bring a different level of value.

Steep and tall roof inspections

This is the niche too many articles treat as a footnote. It isn’t one.

After a hailstorm or wind event, the carrier still needs accurate data from the roof. But a steep or tall structure changes everything. Access points are limited. Eave lines may be unsafe. Tree debris can hide broken surfaces. A quick ladder set and a fast walkover is not a serious plan.

The risk is real. Insurance Restoration Consultants’ consulting areas page notes that steep and tall roofs are involved in 40 percent of roofing-related fatalities, and that post-2025 hurricanes showed a 25 percent increase in steep roof claims. Those claims demand specialists because safety failures and bad documentation usually happen together.

A specialist consultant handles these roofs differently:

- Access planning first: The inspector evaluates ladder placement, roof pitch, surface condition, and fall exposure before deciding how the inspection will be performed.

- Documentation by elevation and slope: Damage is recorded in a way that lets the adjuster understand exactly where findings occurred.

- Evidence over assumptions: On difficult roofs, unsupported statements like “entire roof compromised” are common. A consultant should tie conclusions to specific observations.

A dangerous roof is often a disputed roof. If access is poor, the file fills up with opinions.

Tree impact and hidden damage

Tree claims look simple from the street and turn complicated fast. A branch through a roof opening is obvious. The less obvious issues are what matter later: shifted framing, punctured underlayment, crushed gutters, racked fascia, wet insulation, and interior pathways that don’t show until days later.

A standard inspection may document the hole and miss the load path. A specialist consultant follows the force of impact through the structure. That’s especially important when multiple trades will become involved and each one sees only their portion of the damage.

In that setting, a technically grounded field inspection limits two common problems. First, under-scoping that creates a supplement fight later. Second, over-scoping based on fear rather than evidence.

For assignments involving component-level damage on complicated structures, field teams may also encounter repair questions tied to varied building and mechanical assemblies, including itemized parts and restoration-related components such as specialized rebuild and replacement pieces. The broader point is that high-risk claims often involve detailed parts analysis, not just a simple roof number.

Wildfire smoke and contamination disputes

Smoke claims are increasingly technical because visual inspection alone rarely resolves the file. Odor, residue, HVAC distribution, porous material impact, and habitability concerns all push the claim beyond a basic walk-through.

The challenge isn’t only identifying damage. It’s deciding what level of remediation is supported and how to document it in a way that holds up when the carrier, policyholder, and contractor disagree. In these assignments, the consultant’s role is to impose method. Define affected areas. Separate direct evidence from assumption. Tie recommendations to observed conditions and testing results when available.

That discipline matters because smoke files can expand quickly when nobody defines the boundary of the loss.

Why high-risk claims need a different mindset

The right consultant doesn’t just inspect harder. They inspect differently.

They assume that access may fail, conditions may change, and the first visible damage may not be the controlling issue. On these files, the consultant isn’t just gathering data. They’re protecting the integrity of the decision that follows.

A Consultant's Workflow in a Hail Damage Claim

Take a common assignment. A hailstorm moves through a neighborhood overnight. By the next morning, the carrier has a roof claim on a two-story home with a steep rear slope, dented soft metals, interior staining near a vent stack, and a policyholder who already has two contractor opinions that don’t match.

A good consultant workflow turns that file from reactive to orderly.

First contact and site stabilization

The first priority is speed, but not rushed judgment. The consultant confirms the reported damage, checks whether temporary protection is needed, and coordinates access. If the structure has active leakage or exposed areas, emergency measures come first so the property doesn’t deteriorate while the claim is still being evaluated.

This early phase also sets expectations. The policyholder needs to know what the inspection will cover. The adjuster needs to know when the report is coming and what kind of documentation to expect.

Safe roof access and field inspection

At the property, the consultant doesn’t start by debating replacement versus repair. The first job is to inspect safely and methodically.

On a hail claim with a steep roof, that often means a controlled ladder assist, a slope-by-slope examination, and close documentation of collateral indicators such as soft metals, vents, gutters, and other impact-prone surfaces. The consultant is also looking for non-hail conditions that commonly muddy the file, such as granular loss from age, old mechanical damage, prior repairs, or unrelated foot traffic.

A field partner may rely on practical site equipment and replacement logistics connected to broader property and automotive-adjacent inventories such as direct replacement components used in restoration workflows. What matters in the claim itself is that every observed condition is tied back to location, condition, and likely cause.

Building the file while on site

Strong consultants don’t “inspect now and figure it out later.” They build the file during the inspection.

That means photographs are organized by elevation and component. Notes identify what was seen, what was not seen, and where access was limited. Measurements are captured while the site context is fresh. If the claim includes interior moisture staining, the consultant documents the apparent relationship between roof features and interior damage rather than treating them as separate stories.

The cleanest claim files are built at the property, not reconstructed from memory that night.

This is also the point where the consultant can reduce later conflict by documenting borderline issues with precision. If a mark is not consistent with hail, the report should say why. If a condition supports further invasive evaluation, that should be stated just as clearly.

Estimate, report, and handoff

Once the inspection is complete, the consultant translates field findings into a supported estimate and report package. The best handoffs are concise. The adjuster doesn’t need a long essay. The adjuster needs a reliable answer to practical questions:

- What damage is consistent with the claimed hail event?

- What items fall outside that conclusion?

- Is temporary mitigation needed or already performed?

- What repair scope is supported by the observed conditions?

- Are there any safety, access, or monitoring issues that should affect next steps?

That package gives the adjuster a basis for decision and gives the policyholder a clearer explanation of how the claim is being evaluated.

The real outcome

A well-run hail assignment does more than speed up one estimate. It lowers the chance of supplement disputes, redundant inspections, and contractor-versus-carrier stalemates.

That’s why the consultant workflow matters. It doesn’t replace claims handling. It gives claims handling something solid to work from.

How to Choose and Engage the Right Consultant

A hail file lands on an adjuster’s desk after a contractor says the roof is totaled, the first inspection notes only minor damage, and the building has a six-story elevation with unsafe access from grade. At that point, the question is no longer whether outside help might be useful. The question is whether the file gets a specialist who can sort out scope, causation, and access before the claim slows down further.

High-risk claims need defined trigger points. Carriers that wait for a dispute to mature usually pay for it in reinspections, longer cycle times, and position hardening between the parties. On steep and tall roof losses, delay also creates a safety problem. A routine field visit can turn into an incomplete inspection because the original assignment was given to the wrong resource.

When to bring one in

Use a restoration consultant when the claim has a high chance of producing unsafe access, inconsistent findings, or scope drift.

Common triggers include:

- Steep or tall roof exposure: The inspection requires specialized access planning, ladder assist, or a field partner trained for work at heights.

- Competing damage narratives: The contractor, insured, and carrier are looking at the same property and reaching very different conclusions.

- Tree strike or structural impact: Visible exterior damage may not explain hidden moisture paths, displaced components, or interior effects.

- Commercial or large-loss conditions: Multiple trades, sequencing issues, and code-driven repair questions need tighter field documentation.

- Litigation-sensitive files: The report may need to stand up to close review months later, so the first inspection has to be disciplined.

What to verify before assignment

Technical knowledge matters. Process matters just as much.

A consultant can be excellent in the field and still create delay if reporting is inconsistent, estimating is weak, or dispatch is unreliable after a storm event. The carrier should know exactly how the consultant handles access, documents findings, and returns the file.

| What to check | Why it matters |

|---|---|

| Safety protocols for roof access | High-risk inspections break down fast when access planning is improvised |

| Clear photo reporting standards | The adjuster should not need multiple follow-up calls to understand the findings |

| Experience with cause-of-loss analysis | A good scope starts with a defensible damage conclusion |

| Estimating fluency | Field observations must convert into a repair scope the desk can review and act on |

| Project monitoring capability | Large or disputed losses often need oversight after the initial inspection |

| Geographic reach and dispatch discipline | Storm claims require response capacity and consistent field coverage |

Ask direct questions before sending the assignment. Who performs the inspection. What deliverables are included. How quickly the report is returned. Whether the consultant can handle steep and tall roof conditions without handing the file off again.

Cost should be judged against file outcome

Consultant fees make sense or do not make sense based on what happens to the claim after the assignment.

A low-cost inspection that misses access limits, fails to separate covered damage from unrelated wear, or produces a weak photo set usually creates more work later. A stronger assignment can reduce reinspection, narrow supplement disputes, and give the adjuster a cleaner basis for coverage and scope decisions. On high-risk roof claims, that difference is often larger than the fee gap between vendors.

Cheap field work often becomes expensive claim handling.

How to engage them well

A clear assignment produces a better report.

Send the claimed cause of loss, date of loss, prior estimates if they exist, known dispute points, access concerns, and the exact deliverables needed. If the carrier needs a causation opinion, say so. If the file may require ongoing repair monitoring, define that scope at the start. If the roof is steep, tall, or both, note that plainly so the consultant dispatches the right field resource on day one.

The right consultant brings more than inspection capacity. They bring control to the part of the claim where control is easiest to lose.

A Strategic Partner in Claims Management

When claims get crowded, technical, or hazardous, the underlying issue isn’t just damage. It’s uncertainty. Unclear cause of loss, weak documentation, unsafe access, and drifting scopes all make the file more expensive and harder to resolve.

That’s why insurance restoration consultants matter. They bring order to the point in the process where order has usually broken down. In high-risk scenarios, especially steep and tall roofs, they also protect the claim from a common failure point: trying to force a routine inspection into a non-routine loss.

The best way to view a consultant is not as an added layer between the adjuster and the claim. They are a strategic partner who improves the quality of the information the adjuster relies on. Better information leads to better decisions, faster movement, and fewer avoidable disputes.

When the next difficult file hits the desk, the question usually isn’t whether the claim is complex. It’s whether the team has the right specialist involved early enough to control it.

If your team needs a field partner for steep and tall roof inspections, storm and tree damage assessments, ladder assists, emergency tarping, or detailed estimating support, Fox Claims Consultants LLC provides national property inspection services built for difficult, high-risk claims.

Leave a Reply