The storm has moved on, but the claim has just begun.

For many, the first hours after a hurricane feel less like a paperwork problem and more like controlled disorder. Shingles are missing. A ceiling stain is spreading. Tree limbs are down across driveways and fences. Phones are full of photos, but nobody is sure which ones matter. The carrier wants prompt notice. The adjuster needs access. The homeowner wants to stop further damage before the next rain band arrives.

That is where hurricane insurance claims often go off track. Not because the damage is imaginary, but because the early decisions are rushed, incomplete, or based only on what is easy to see from the ground.

On straightforward losses, that may be enough. On steep roofs, tall elevations, and structures with complex rooflines, it usually is not. Hidden damage after a hurricane is one of the biggest reasons claims become underpaid, disputed, or delayed. If the first inspection misses uplift damage, broken seals, displaced flashing, or water entry paths, the file starts with a flawed picture of the loss.

Order comes from process. Good claims handling starts with accurate cause analysis, disciplined documentation, safe access, and timely mitigation. Carriers need reliable field information. Adjusters need usable evidence. Homeowners need a path that makes sense when everything around them does not.

After the Storm: Hurricane Claims Uncovered

At first light after a hurricane, a three-story home with a steep roof can look surprisingly manageable from the driveway. A few shingles are in the yard. Gutters are bent. Water shows on an upstairs ceiling. The visible damage feels contained.

The harder problem is often above the line of sight.

On tall elevations, steep slopes, and complex roof systems, hurricane damage rarely stays limited to what a ground-level walkaround can confirm. Wind can lift roofing materials just enough to break seals, shift fasteners, crease membranes, or open small pathways around flashing and penetrations. Those conditions may not stand out in early photos, but they can change the valuation of the loss and the repair scope in a material way.

That is where underpaid claims often start. A file built around visible debris and interior staining, without a safe and qualified inspection of difficult-to-access roof areas, can miss the actual point of failure. The result is a repair estimate that addresses symptoms instead of cause. Months later, the property owner is dealing with recurring leaks, deteriorated decking, mold concerns, or a dispute over whether the later damage ties back to the storm.

Carriers, adjusters, and homeowners all face different pressures in those first days. Carriers need defensible field information. Adjusters are triaging heavy volume and making decisions quickly. Homeowners are trying to protect the property before the next rain arrives. On high-risk properties, speed still matters, but speed without the right inspection method creates avoidable exposure.

At Fox Claims Consultants, we see this pattern most often on properties where safe access is the limiting factor. If the roof is too steep to walk, too tall for a basic ladder setup, or too complex for a quick exterior check, the inspection plan has to change. Drone imagery, ladder assist, rope-and-harness access, and close review of flashing lines, seal strips, vents, ridges, valleys, and water entry points are often what separates a clean claim file from an incomplete one.

Practical takeaway: Start with safety, stabilize the structure, then document the full loss with an inspection method that matches the property, not just the schedule.

Basic emergency supplies still matter while the claim gets moving. Even temporary site support can help families and crews work more safely in damaged conditions, including simple items like emergency thermal blankets used in storm response kits.

Understanding Your Hurricane Coverage

A hurricane claim starts with the policy, not the damage.

If the policy language is misunderstood, every decision afterward gets harder. Homeowners often assume “hurricane damage” is one category. It is not. The policy usually separates causes of loss, deductibles, coverage parts, and exclusions. Adjusters know this, but even experienced claim professionals see disputes grow when that rulebook is not explained clearly at the start.

Wind coverage and flood coverage are not the same

Most hurricane insurance claims involve at least one early causation question. Did wind damage the structure? Did water enter because wind opened the building envelope? Or did rising water cause the loss?

That distinction matters because windstorm damage is typically handled under the property policy, while flood damage is usually handled under separate flood coverage if the insured has it. In practice, many disputes begin when both happened close together.

A simple example helps. If hurricane winds tear shingles from a roof and rain enters through the opening, that usually points to a wind-driven opening issue. If water rises from the ground and enters at the base of the structure, that points to flood. Actual losses can contain both, and separating them requires disciplined documentation.

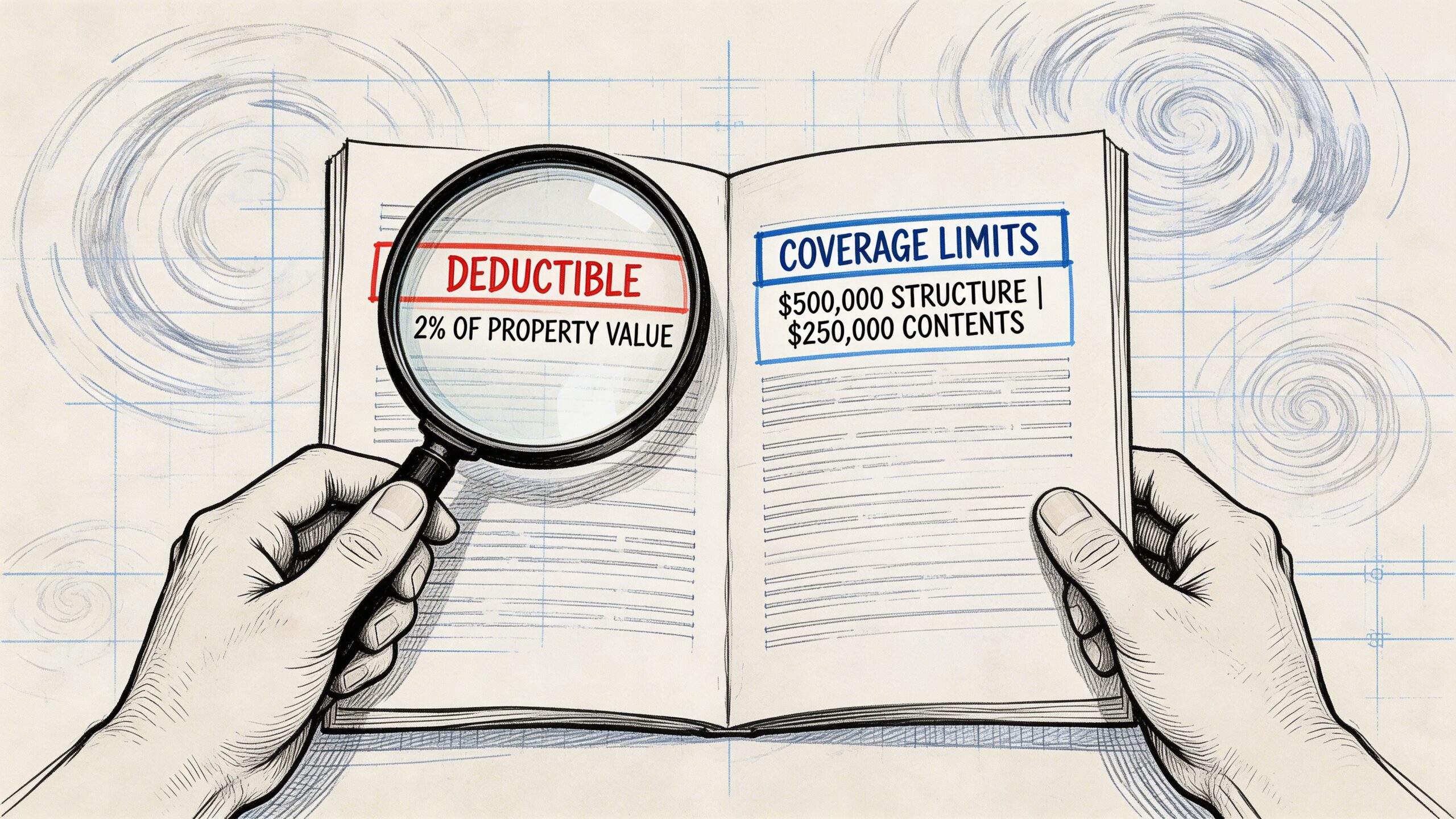

The deductible that surprises people most

The largest shock in many Florida claims is not whether the loss is covered. It is the size of the deductible.

Hurricane percentage deductibles, mandated in Florida under Statute 627.701(5)(a), apply to wind damage claims during specific warning periods. They are calculated as 2%, 5%, or 10% of the dwelling’s insured value. A 5% deductible on a $250,000 home is $12,500, according to this explanation of hurricane percentage deductibles.

That deductible is very different from a standard flat deductible. It changes how people view the claim, especially when the damage is meaningful but not obviously above the threshold.

Tip: Before arguing over scope, confirm which deductible applies and whether the storm date falls inside the warning period that triggers it.

What each coverage bucket is trying to do

Policies usually divide recovery into separate parts. The names vary by form, but the function is familiar.

| Coverage area | What it generally addresses |

|---|---|

| Dwelling | The main structure, including roofing, walls, attached components, and built-in elements |

| Other structures | Detached garages, sheds, fences, and similar property |

| Personal property | Contents damaged by a covered cause of loss |

| Additional living expense | Temporary living costs if the home cannot be safely occupied |

These categories matter because a strong hurricane insurance claim separates the damage by location and by coverage type. A roof issue, soaked contents, and hotel expenses should not be blended into one vague narrative.

What works and what does not

What works is reading the declarations page and policy language before the inspection fight begins. What does not work is assuming every part of hurricane-related water damage falls under one coverage bucket.

For homeowners, the practical move is to gather the policy, deductible information, and any endorsements before speaking in detail about the loss. For adjusters, the practical move is to explain coverage boundaries early, in plain language, so expectations stay grounded in the contract.

The Hurricane Insurance Claim Lifecycle Explained

At 7:30 the morning after landfall, a carrier has a new file, a homeowner has water in two rooms, and the steep rear roof nobody can safely see from the driveway may be the difference between a clean adjustment and a disputed claim six months later.

Major storm volume strains every part of the process. As noted earlier, catastrophic property claims made up an unusually large share of personal lines property activity in 2023. Under that kind of pressure, the files that move best are the ones built on a clear sequence, solid field notes, and inspections that match the risk of the property.

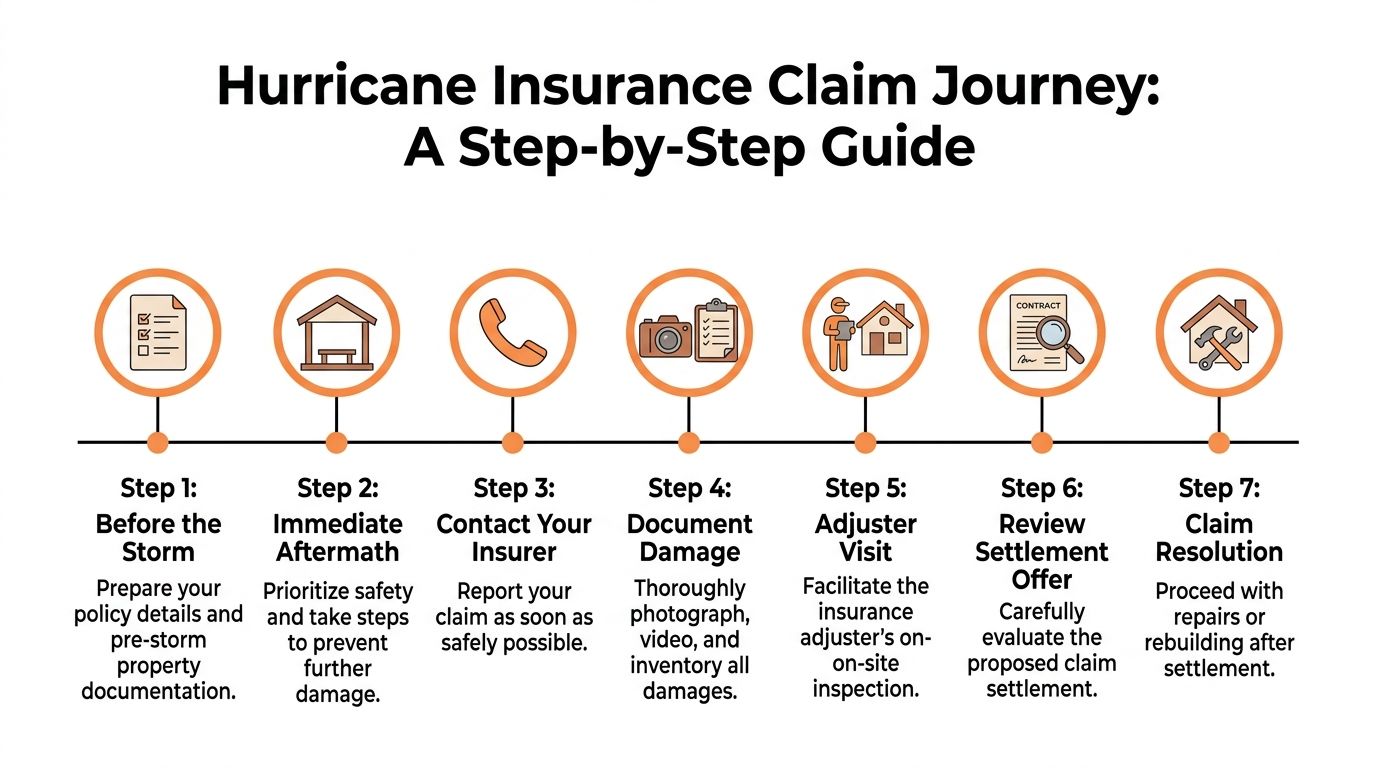

First notice sets the tone

The claim starts at first notice of loss, or FNOL. At this stage, the insured reports the date of loss, location, visible conditions, emergency needs, and any immediate safety concerns.

Good FNOL reporting stays factual. Shingles observed in the yard. Ceiling staining in the upstairs hall. Tree contact at the garage corner. Active water entry in the guest room.

That discipline matters. If the first report guesses at engineering conclusions or skips over urgent mitigation needs, the file starts with noise instead of usable facts.

Mitigation comes before full repair

The next step is to stop further damage without destroying evidence. Tarping, board-up, water extraction, and debris removal usually belong here. Full replacement of damaged materials usually does not.

That line gets missed all the time after hurricanes.

On high roofs and complex structures, early repairs can erase the very conditions needed to evaluate wind-created openings, displaced flashing, or impact points. Temporary protection preserves both the property and the claim. On water-heavy losses, crews may also need simple site equipment to keep drainage and extraction organized, including a lay-flat water discharge hose for storm cleanup and mitigation work.

Inspection is where underpayment risk usually begins

The inspection stage drives the rest of the file. If the inspection misses damage, the estimate misses damage. If the estimate misses damage, the settlement starts in the wrong place.

That problem is sharper on steep-slope roofs, tall homes, and other high-risk properties. A standard walkaround and a few ground photos may confirm that a storm passed through. They do not reliably identify lifted tabs, fractured seal strips, shifted ridge components, damaged accessories, or water paths entering at upper transitions. Those are the losses that later show up as interior staining, mold complaints, decking deterioration, or repair disputes.

From a claims handling standpoint, the trade-off is straightforward. A basic inspection is faster and cheaper at the front end. A specialized roof inspection costs more up front, but it often prevents missed scope, reopened files, supplements, and future liability tied to concealed structural damage.

The working sequence is simple:

Stabilize unsafe or active loss conditions

Stop ongoing water entry and address immediate hazards.Record the original condition

Photograph and note conditions before materials are moved, dried out, or covered.Inspect the full building envelope

Exterior findings need to be checked against interior moisture patterns, attic conditions, elevations, and transitions.Match observations to supportable conclusions

A creased shingle, displaced flashing, or punctured underlayment is an observed condition. The repair conclusion should follow the full inspection record, not assumption.

Estimating and scope review

Once inspection data is in, the file shifts to scope and estimate review. Many disputes are framed as pricing fights. In practice, the bigger issue is often missing scope.

A hurricane estimate can look orderly and still understate the loss if it omits detached roof accessories, wet insulation, damaged vents, flashing replacement, code-triggered work, or repairs tied to steep-access requirements. On taller structures, access method alone can affect what gets seen and what gets priced. If nobody safely inspected the upper slopes, valleys, or wall intersections, the estimate may reflect convenience rather than actual damage.

That is where experienced adjusters and inspection partners earn their keep. The goal is not to inflate a file. The goal is to build one that matches observed damage, probable hidden damage, and the repair method the structure requires.

Key takeaway: Hurricane claim disputes often start with incomplete inspection scope, then show up later as payment disputes.

Settlement and repair

After scope review, the claim moves into coverage position, payment, and repair coordination. More parties touch the file at this stage, including the carrier, adjuster, insured, contractor, and sometimes a mortgage holder. Clarity matters.

The smoother files usually share a few traits:

- Written repair reasoning that explains why items were included, limited, or deferred

- Clear deductible treatment so net payment is understood early

- Supplement procedures for damage discovered after safe access or material removal

- Repair sequencing that preserves evidence if causation questions are still open

Hurricane claims rarely follow a clean line from notice to payment. The ones that resolve well usually have one thing in common. Each stage leaves the next stage better information than it started with.

Documenting Damage The Key to a Successful Claim

If I had to narrow hurricane insurance claims down to one variable that consistently changes outcomes, it would be documentation.

Not volume of paperwork. Quality of evidence.

Many claim files contain dozens of photos that prove very little. They show wet carpet, missing shingles, ceiling stains, and debris piles. Those images confirm that something happened, but they do not always prove how it happened, how far it extends, or what is likely to fail next. On steep roofs and taller structures, that gap becomes costly.

Visible damage is only the first layer

The common approach after a storm is understandable. People photograph what they can see from the ground, take a few interior shots, save a receipt for tarping, and wait for the adjuster.

That approach is better than doing nothing, but it is often not enough on complex buildings. A steep roof can hide storm-created issues that do not announce themselves with dramatic openings. Small seal failures, shifted components, and water intrusion behind finished surfaces may not present clearly until days or weeks later.

That problem is not minor. A documented gap in claims processing is hidden structural damage on steep roofs, where unfamiliar inspections can undervalue claims by 20% to 50% because loosened seals, frame breaks, and similar issues are missed, according to this discussion of underpaid hurricane damage claims.

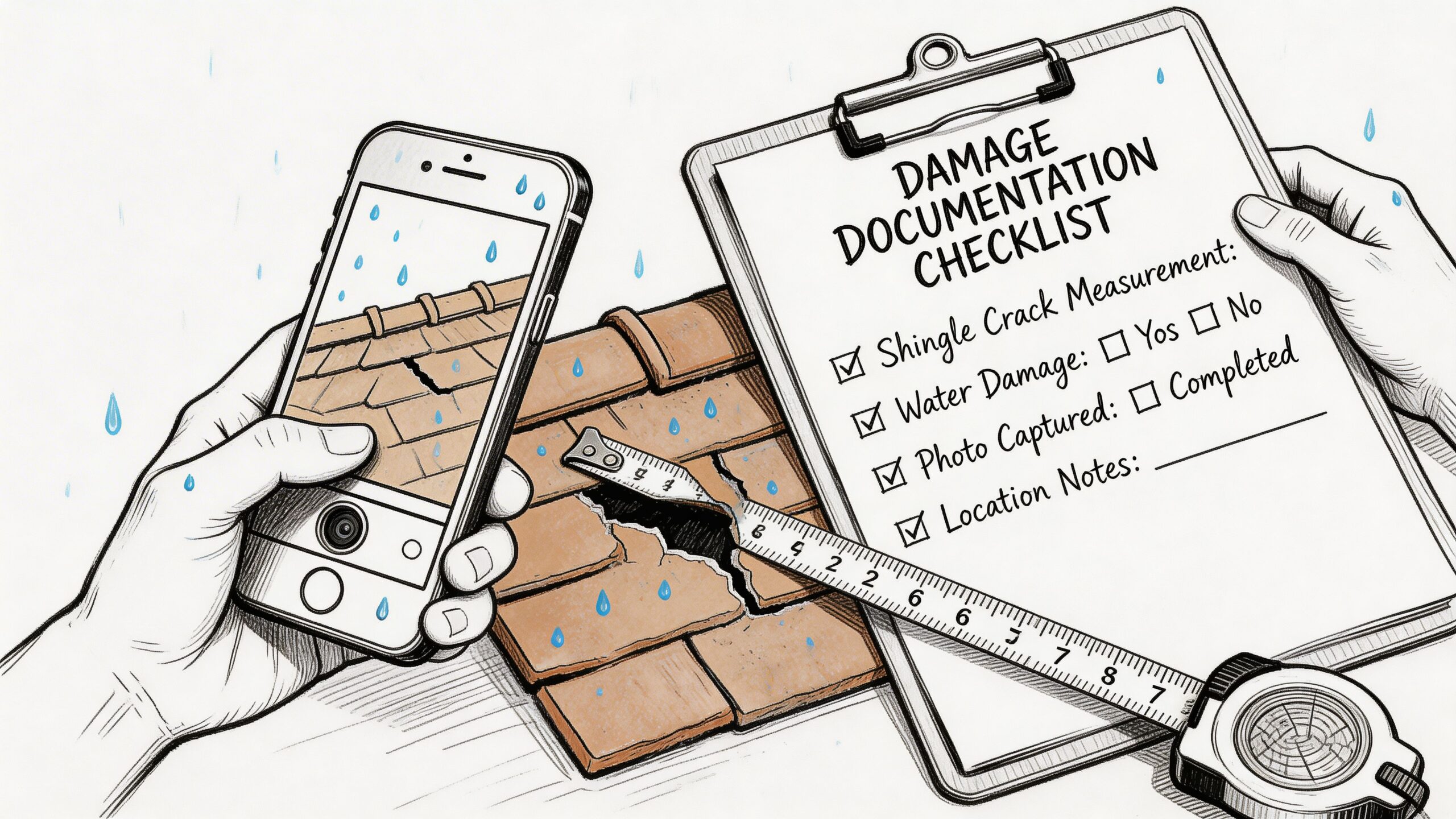

What strong documentation looks like

Strong documentation creates a chain. It should allow someone who was not present at the property to understand the loss without guessing.

That usually includes:

- Wide shots first that place each damaged area in context

- Mid-range photos that connect the damaged component to the structure

- Close-ups showing the actual failure, not just the general area

- Interior-to-exterior matching so water staining is tied to likely entry locations

- Date-organized records of temporary mitigation, contractor visits, and insurer communications

A good file also distinguishes between pre-existing wear and fresh storm effects. Blending those together weakens credibility.

Hidden damage on high-risk roofs

Steep and high roofs create two problems at once. They are more dangerous to access, and they are easier to under-document.

On these properties, adjusters and carriers should be particularly careful about:

| Often missed condition | Why it matters in the claim |

|---|---|

| Broken or loosened seals | Can support wind-related distress even when the roof covering remains in place |

| Displaced flashing or edge metal | Often creates the actual water entry path |

| Subtle uplift or creasing | May indicate damage that is not visible from the ground |

| Moisture behind exterior finishes | Can expand the scope beyond what the first interior stain suggests |

Tip: A photo of damage is not enough. The claim needs a photo that answers location, extent, and likely sequence.

Record the administrative side too

Some of the strongest evidence in hurricane insurance claims is not visual. It is procedural.

Keep:

All receipts for emergency work

Tarping, drying, board-up, debris handling, and temporary supplies.A communication log

Date, time, who called, what was discussed, what was promised.Every version of every estimate

Initial scope, revised scope, supplemental requests, and contractor comparisons.A room-by-room contents list

If personal property is involved, broad descriptions are weaker than itemized records.

For field teams, organized forms help keep this clean. Even something as basic as a job packet with estimate, invoice, and receipt forms can prevent small administrative misses that later become claim friction.

What does not work

What does not work is relying on memory. It does not work to clean up first and document later. It does not work to assume the visible leak stain tells the whole roof story.

The most expensive damage on a hurricane loss is often the damage that did not look important on day one.

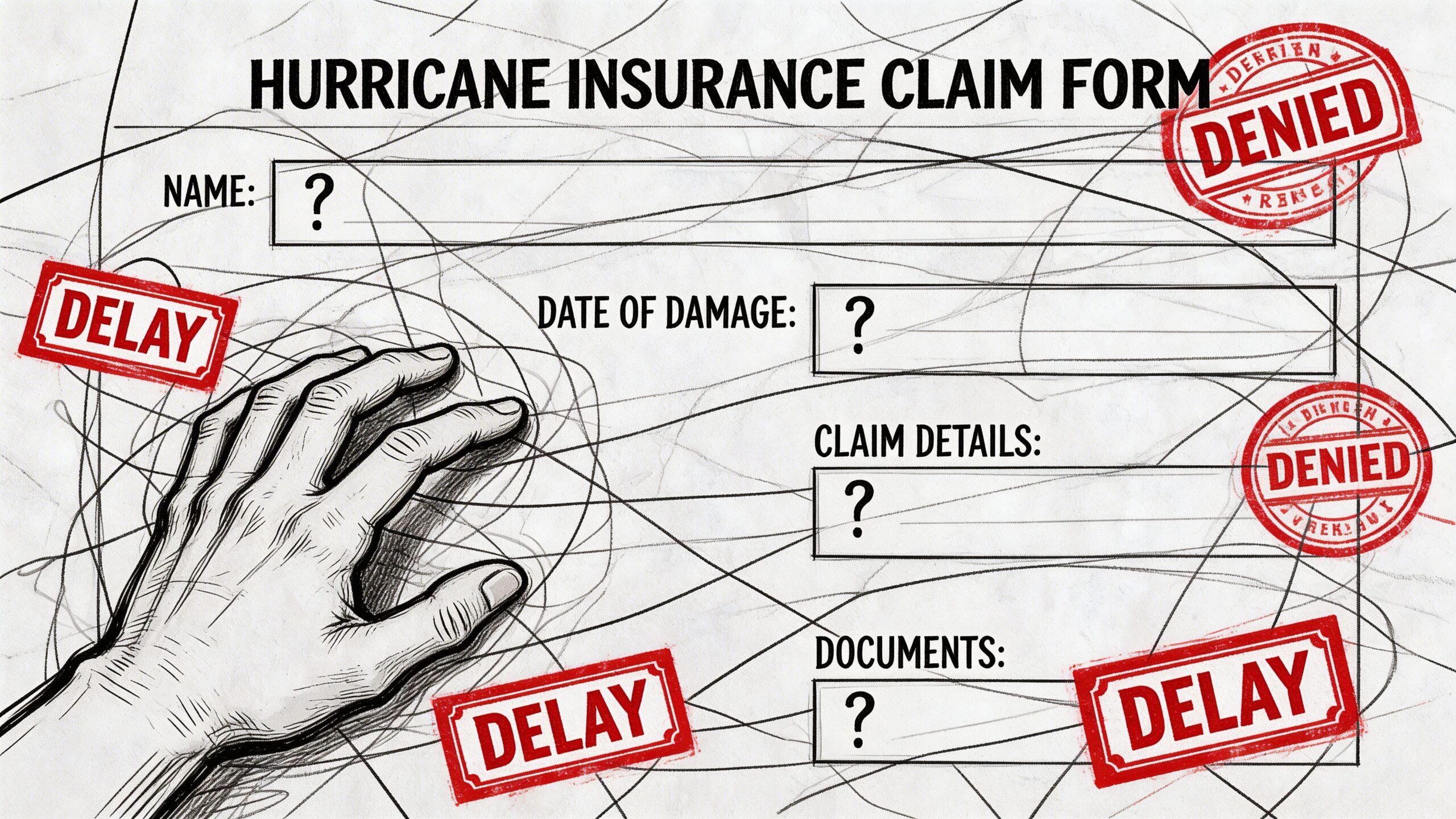

Why Hurricane Claims Get Delayed or Denied

Most delayed or denied hurricane insurance claims follow a familiar pattern. The file lacks clear causation, the damage documentation is thin, or the estimate does not match what the property needs.

Policyholders often experience that as silence, repeated requests, or a narrow coverage position. Adjusters experience it as a file that cannot be comfortably closed because the facts are incomplete. Carriers experience it as rework.

The biggest trouble spot is often causation

Hurricanes rarely damage a property in one clean, isolated way. Wind acts first. Rain follows. Trees fall. Water migrates. Ground conditions change.

That creates the most common conflict in these claims: wind versus flood.

For Hurricane Helene, 20.3% of all unpaid claims were related to flood issues, according to this analysis of denied or underpaid Helene claims. The practical problem is that wind-driven rain through a storm-damaged roof is typically covered, while flood exclusions are often raised when water damage is involved.

When the file does not clearly show how water entered, someone fills that gap with an assumption. That is how denials and underpayments start.

What the file usually lacks

In my experience, delayed claims are often missing one of these elements:

- A documented opening in the roof or building envelope

- A sequence of loss that places wind damage before rain intrusion

- Access to the right elevations, especially on steep or tall roofs

- Consistent descriptions between the homeowner, contractor, and adjuster

- Temporary mitigation records showing prompt efforts to prevent worsening damage

Any one of those can create drag. Several together can stall the file.

The wind-driven rain problem

A lot of frustration comes from using the word “flood” loosely. Homeowners often mean “there was a lot of water.” Claims handling requires more precision.

If wind damages roofing or flashing and rain enters from above or through a storm-created opening, that points in one direction. If rising water enters from the ground or outside grade, that points in another. If both happened, each path needs to be documented separately.

That is why roof access matters so much. Without it, the file may show interior water but not the exterior failure that explains it.

A short overview can help frame that issue before a coverage decision hardens:

Delay causes that are avoidable

Some delays are built into catastrophe conditions. Heavy volume slows everyone. But many delays are preventable.

| Delay trigger | Better practice |

|---|---|

| Late reporting | Give notice as soon as conditions are safe |

| Cleanup before documentation | Photograph and record conditions first whenever possible |

| One-sided estimates | Match the estimate to site evidence and damaged components |

| Unsafe or incomplete roof access | Use proper inspection methods for steep and high areas |

Practical takeaway: The strongest way to reduce denial risk is to make the causation story visible, not verbal.

The trade-off nobody likes

Carriers want speed after a catastrophe. Policyholders want speed too. But speed without accuracy creates supplements, disputes, and reopened files.

A rushed ground inspection on a complex roof can feel efficient in the moment. It often becomes expensive later. The better trade-off is a disciplined inspection early, especially where roof geometry, height, or hidden moisture paths make a simple walkaround unreliable.

Tips for a Smoother Claims Process

Smooth hurricane insurance claims rarely happen by accident. They happen because each party handles its part of the file with discipline.

The best practices differ depending on who you are. A homeowner’s job is not the same as a desk adjuster’s, and a carrier’s operational decisions are not the same as a field inspection decision. Still, the goal is shared: reduce confusion, shorten cycle time, and make the file defensible.

For homeowners

Start with the basics and do them thoroughly.

- Report the loss promptly: Give notice as soon as you can do so safely and accurately.

- Protect the property: Use temporary measures to stop additional damage, but avoid full repairs before the loss is documented.

- Keep a single claim file: Store photos, receipts, emails, estimates, and notes in one place.

- Be precise in descriptions: Report what you observed, not what you assume the policy covers.

- Use temporary protection materials when needed: If an opening exists, items like a heavy-duty storm tarp for temporary covering can help reduce additional intrusion until a formal inspection occurs.

For field and desk adjusters

Claims handling gets better when the file tells a coherent story.

A practical adjuster workflow looks like this:

Confirm the claimed cause of loss without adopting it blindly

Listen first. Verify second.Match interior effects to exterior conditions

A stain on a ceiling is not a roof conclusion by itself.Separate wear, prior issues, and storm-related conditions

Mixed-condition files need careful notation.Escalate difficult roof access early

Waiting too long to get safe access usually means weaker evidence.

A key legal tool in difficult causation files is the efficient proximate cause doctrine. In hurricane claims, it means that if a covered peril such as wind sets the chain of events in motion, resulting damage may still be covered even when a later event is otherwise excluded. Proper analysis can resolve 20% to 30% of contested claims, according to Hunton’s discussion of hurricane causation and coverage issues.

Tip: In a mixed-peril file, do not ask only “What touched the property last?” Ask “What set the loss sequence in motion?”

For carriers and catastrophe teams

Carriers usually see the same operational weak points after a major storm. Inspection capacity tightens. Communication lags. Desk teams receive inconsistent field packages.

Three habits help:

- Standardize early field reporting so every inspection package includes the same core evidence set

- Triage high-risk structures differently instead of assigning every roof loss the same response model

- Use specialized inspection partners when the roof is unsafe, unusually steep, or likely to contain hidden damage

In this context, one focused third-party option can make sense. Fox Claims Consultants LLC performs steep and tall roof inspections, ladder assist, storm assessments, emergency tarping, and photo-documented field reporting for complex property losses. In the right file, that kind of support helps carriers and adjusters obtain safer access and cleaner documentation without forcing a generalist inspection approach onto a specialist problem.

When to Engage Professional Inspection Partners

Not every hurricane claim needs a specialized inspection partner. Some losses are visible, accessible, and straightforward.

But some properties raise immediate red flags. The roof is too steep for a routine walk. The structure is tall enough that ground photos are weak. Water has appeared inside, but the entry point is unclear. A contractor, adjuster, and homeowner all agree there is damage, yet nobody can confidently document the full mechanism.

That is when bringing in a professional inspection partner stops being an extra step and starts being the efficient step.

The right time is earlier than commonly thought.

The biggest mistake is waiting until the file is already disputed.

Specialized inspection support is useful when:

- Access is unsafe for a standard roof inspection

- Damage appears limited at first glance but interior conditions suggest a broader problem

- The roof geometry is complex, with multiple transitions, elevations, or concealed paths for water

- Causation matters because wind and water may be competing explanations

- Temporary stabilization is needed before evidence disappears

A good partner should not merely take more photos. The value is in getting the right photos, from the right elevations, with observations that help the carrier and adjuster make decisions.

What useful support looks like

On complex hurricane insurance claims, the most practical outside support usually includes ladder assist, drone-supported overview where appropriate, emergency tarping, temporary repairs, and reporting that ties exterior findings to interior effects.

For hidden moisture or concealed access points, even basic building components matter. Something as simple as understanding concealed entry or service areas can affect the inspection path, especially on properties with enclosed spaces and utility runs. In those settings, tools and materials like an inspection access panel for walls or service areas can be relevant to how hidden conditions are safely reviewed during repair or further evaluation.

Key takeaway: Use a specialist when the cost of missing damage is higher than the cost of getting the inspection right the first time.

The strongest claims files are not always the biggest. They are the ones built on complete, defensible field evidence.

Bringing Order to Chaos A Final Word

Hurricanes create physical damage fast. Claim problems develop more slowly.

A missed roof condition, a weak photo set, an unclear water entry path, or a rushed inspection can shape the entire file long after the wind is gone. That is why hurricane insurance claims demand more than prompt reporting. They demand accurate causation, careful documentation, and a process that respects both coverage limits and field realities.

For homeowners, the practical path is to stabilize the property, preserve evidence, and keep records tight. For adjusters, it is to separate observation from assumption and avoid forcing complex roofs into simple inspection models. For carriers, it is to recognize where specialized field support reduces rework rather than adding it.

The most important point is this: chaos after a storm is normal. Disorder in the claim file does not have to be.

When the right people document the right conditions early, hurricane claims become easier to evaluate, easier to explain, and easier to resolve fairly. That is true whether the issue is a torn roof covering, hidden uplift on a steep slope, or water damage that depends on proving how the storm opened the structure.

Recovery starts with facts. Good claims handling turns those facts into decisions people can trust.

When a hurricane loss involves steep roofs, tall structures, hidden damage, or urgent mitigation, Fox Claims Consultants LLC can support carriers, adjusters, and property owners with field inspections, ladder assist, emergency tarping, and photo-documented reporting that helps move complex claims toward clear resolution.

Leave a Reply