After a hailstorm rolls through, the first question on every property owner's mind is always the same: what’s this going to cost me?

In 2026, the average hail damage roof repair cost is about $4,250. That number can swing wildly, from as little as $375 for a few quick fixes to $7,500 or more when the damage is severe. But that's just a starting point. Let's break down what really goes into the final number.

Your Quick Guide to 2026 Hail Repair Costs

The stress of figuring out the finances can be almost as bad as seeing the damage itself. Getting a clear financial baseline is the first step toward getting things back in order. The numbers might seem intimidating at first, but they make a lot more sense once you understand what's driving them—starting with your roofing material.

Estimated Costs by Material

Let's be clear: not all roofs are created equal, and their repair costs show it. The material protecting your home is the single biggest factor in what you'll pay per square foot for repairs. Fixing a few asphalt shingles is a completely different ballgame than repairing specialized materials like slate or metal.

To give you a quick reference, here’s a look at the estimated repair costs for common roofing materials in 2026. Think of this as your financial map to get a sense of the potential expense before we dive into the specifics of your property.

Estimated Hail Damage Repair Costs by Roofing Material (2026)

This table gives a quick overview of estimated repair costs per square foot for the most common types of roofing materials after hail damage.

| Roofing Material | Average Repair Cost per Square Foot |

|---|---|

| Asphalt Shingles | $1.20 – $4.00 |

| Metal Roofing | $4.50 – $7.00 |

| Wood Shakes | $5.00 – $10.00 |

| Slate/Tile | $5.00 – $30.00 |

These numbers aren't just estimates; they reflect the realities of the market and the skills required for each material.

Understanding the National Averages

These figures aren't pulled out of thin air. They come from real-world data in markets where hailstorms are a regular event. In 2026, we see homes in the Midwest and Plains states with repair bills often falling between $4 to $7 per square foot for materials and labor alone.

For example, fixing a handful of standard asphalt shingles might run you $1.20 to $4 per square foot. But if that same storm battered a metal roof, you're looking at $4.50 to $7 per square foot. For high-end materials like slate, the cost of hail damage roof repair can jump to a staggering $30 per square foot, which shows just how wide the cost spectrum can be. You can find more general information about roofing repair costs on resources like Angi.com.

Key Factors That Drive Your Final Repair Bill

The type of shingles on your roof is just the starting point. Several other critical variables will influence the final hail damage roof repair cost. Think of it like a car accident—a small fender bender is one thing, but a bent frame changes everything.

Understanding these factors helps explain why one repair quote can be thousands of dollars different from another.

The biggest cost driver is, without a doubt, the extent and severity of the damage. A few cosmetic dings are minor. But widespread impacts that crack, puncture, or strip away the protective granules from your shingles have compromised your roof's entire defense system against water. That level of damage demands a much more extensive—and costly—response.

A roof with just 5-10 hail hits per 100 square feet might be a candidate for simple repairs. But once that number jumps to over 10-12 hits in the same area, most insurance carriers and roofing pros will start treating it as a total loss, triggering a full replacement.

This difference between cosmetic and functional damage is what truly matters. A few dents might not look urgent, but they create weak points that can lead to major leaks and structural problems months or even years down the road. A professional assessment is the only way to know if the damage is just on the surface or if the roof's core integrity is shot.

Your Roof’s Unique Design and Layout

Not all roofs are created equal. The complexity of your roof’s architecture plays a huge role in the labor costs. It's like painting a single, flat wall versus painting a room with alcoves, windows, and built-in shelving. The second job takes more time, more precision, and more skill.

The same logic applies to roofing. A roof's pitch, or its steepness, is a major factor.

- Low-Pitch Roofs (Walkable): A roof with a gentle slope is faster and safer for crews to work on. They can move efficiently with less safety gear, which keeps labor costs down.

- High-Pitch Roofs (Steep): A steep roof is a whole different ballgame. It demands extensive safety equipment like harnesses, ropes, and anchor points. The work is slower, more dangerous, and requires a more experienced crew, driving the cost up significantly.

Beyond the pitch, other common features add complexity and hours to the job:

- Dormers and Valleys: Every corner, valley, and junction needs intricate flashing and sealing work.

- Skylights and Vents: Cutting and sealing around penetrations has to be perfect to prevent leaks, and perfection takes time.

- Multiple Stories: A two- or three-story home means more setup, more equipment for lifting materials, and greater safety precautions than a single-story ranch.

Each of these elements adds labor hours and material costs, turning what seems like a simple repair into a much more complex project.

External Market and Regional Forces

Your final bill isn't just about your roof—it's also about where you live and what’s happening in the market. Two major external forces can have a massive impact on your hail damage roof repair cost.

First, regional labor rates vary a lot across the country. Skilled labor simply costs more in a major city than it does in a small town. That's just a fact of local economics.

Second, the "demand surge" after a major hailstorm is very real. When an entire city gets hit, thousands of homeowners all need repairs at once. This creates a huge backlog for contractors, and the sudden scarcity of both qualified labor and materials drives prices up, sometimes by 20-30%. It’s a premium you pay for urgent, widespread need in a concentrated area.

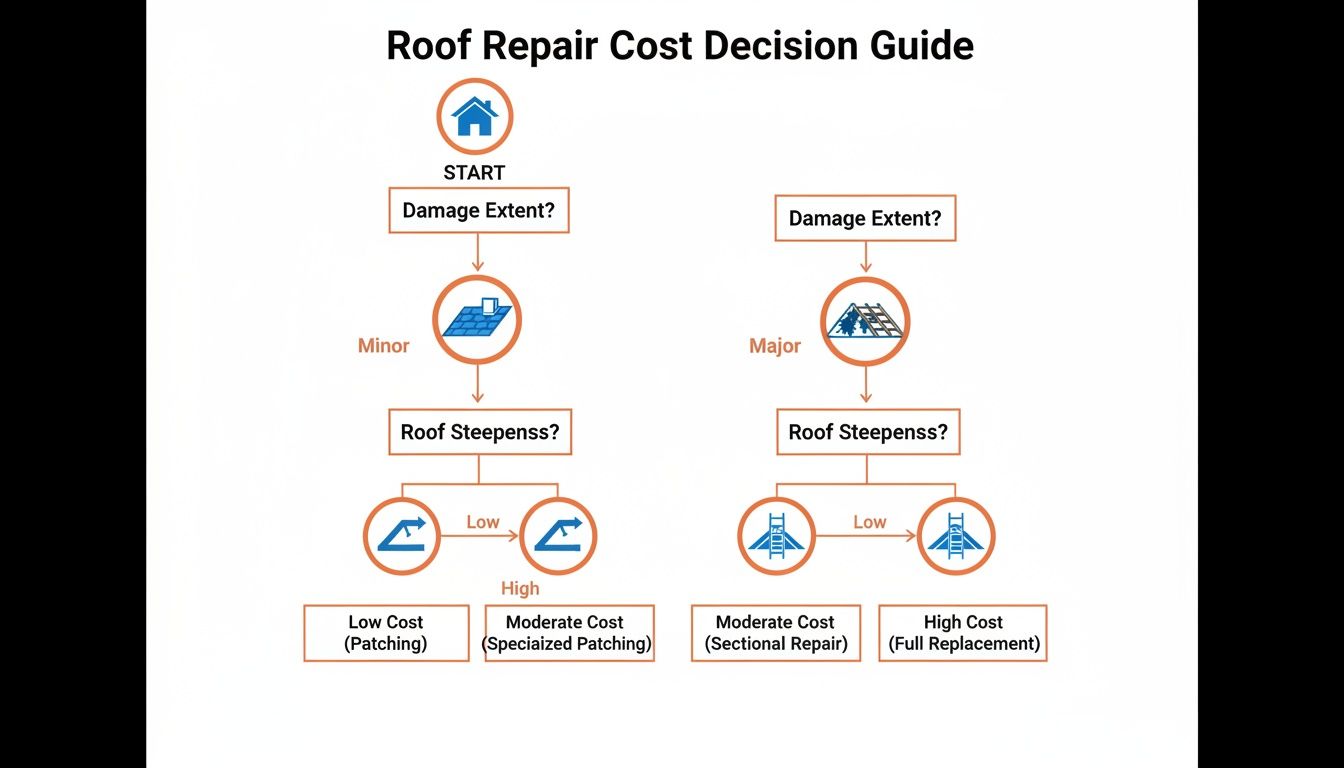

To Patch or Replace? Making the Right Call After a Hailstorm

After a hailstorm rolls through, the biggest question homeowners face is a tough one: do you get by with a simple patch job, or is it time for a full roof replacement? This isn't just a minor decision. Making the wrong choice can cost you thousands in wasted money and lead to major headaches down the road.

A patch is a quick fix for a small, isolated problem—a few cracked or missing shingles. A replacement, on the other hand, is a complete overhaul. It's what's needed when the damage is widespread, the roof is getting on in years, or the storm has fundamentally compromised its integrity. The hail damage roof repair cost for these two paths couldn't be more different.

When a Few Patches Will Do the Trick

Opting for a minor repair is like putting a spare on a tire. It makes perfect sense when the damage is contained and the rest of your roof is in great shape. You wouldn't replace all four tires for a single puncture, and the same logic applies here.

A simple repair is usually the right move if your roof checks these boxes:

- The Damage is Localized: The hail impacts are concentrated in one or two small areas, not scattered across every slope.

- Your Roof is Still Young: It’s less than 10-12 years old and the shingles still have a lot of life left in them.

- No Hidden Problems: A good inspection shows no signs of old leaks, water-stained decking, or widespread granule loss that would cause a new patch to fail.

In these cases, a targeted repair can get your roof back in fighting shape without the expense of a full replacement. But it all hinges on getting an honest, thorough assessment first.

The Tipping Point for a Full Roof Replacement

Deciding on a full replacement is a much bigger commitment, but it's often the smartest financial move you can make. Trying to patch an old, failing roof is like putting a brand-new transmission in a car with a rusted-out frame. You’re just throwing good money after bad, because the rest of the roof is likely to fail soon anyway.

Hail damage is notorious for pushing a roof past the point of no return. This is where the scope of work shifts from a simple repair to a necessary replacement.

As you can see, factors like widespread damage and a steep roof pitch dramatically change the math, often making replacement the only logical choice.

When hail damages large sections of an older roof, a simple repair just won't cut it. Data shows that while small repairs average around $940, widespread damage quickly sends the project cost soaring to $10,000 or more. As a This Old House report notes, with rising labor costs, even small fixes are becoming more expensive, making a full replacement a better value for roofs over 15 years old.

A key rule we use in the field is the "age plus damage" factor. If a roof is over 15 years old and has moderate to severe hail damage across multiple sections, a full replacement is almost always the right call.

Why You Need a Professional Inspection to Decide

You simply can’t make this call from the ground. What looks like a few dings from your driveway could be hiding a much bigger problem. Hail often causes "bruising"—subtle damage beneath the shingle that fractures the matting and creates a future leak—that's completely invisible to an untrained eye.

This is where a professional, unbiased inspection is non-negotiable.

An expert inspector gives you the hard data needed to make an informed choice. They document not just the obvious hits, but the "functional damage" that justifies a proper insurance claim. This detailed assessment ensures you aren’t talked into a cheap patch when a replacement is what’s truly needed. By delivering a clear, evidence-backed scope of work, professional estimating services give you the power to secure the right fix and avoid a costly mistake. That detailed report is the foundation of an accurate hail damage roof repair cost and a claim that gets approved.

Understanding the High Cost of a Full Roof Replacement

When repairs aren’t enough and you’re staring down a full roof replacement, the five-figure price tag can be a shock. But that number isn’t just for a pile of shingles. It’s a mix of skilled labor, raw materials, and powerful market forces that all come together after a storm.

Understanding what’s behind the hail damage roof repair cost is the first step to navigating a total replacement.

The single biggest line item is almost always labor. Replacing a roof isn't like putting together furniture from a box. It's a high-stakes construction project happening stories above the ground, requiring a coordinated team to tear everything off, fix the underlying structure, and install a new system flawlessly.

This is tough, skilled work, and it's why labor alone can make up 60% of the total bill.

The Labor and Material Cost Breakdown

Have a steep roof? That’s going to drive your labor costs up—a lot. It’s all about safety. Crews need specialized gear like harnesses, roof jacks, and scaffolding just to work without incident. This equipment slows down the job and requires more experienced—and more expensive—roofers.

On top of that, material prices have been on a steady upward march for years. Asphalt shingles, the go-to for most homes, have seen a consistent annual price hike of 3-5%. If you’re looking at specialty materials like metal or slate, costs can be even more volatile, jumping based on supply chain issues or raw material shortages.

When a big storm hits, skilled roofers and the materials they need become scarce commodities. This is why everyone—from contractors to homeowners—has to be ready for inflated prices after a major weather event.

It’s this one-two punch of rising material prices and huge demand for skilled labor that really drives the final cost. It isn’t just one thing; it’s how they work together that pushes prices higher every year.

The Post-Storm Price Surge

Beyond the usual costs, a massive hail event introduces another factor: the post-storm price surge. When a storm carves a path through an entire region, thousands of property owners are suddenly looking for a good roofer. This creates an instant and massive backlog for qualified contractors.

Basic supply and demand takes over from there. With far more demand than available crews, prices for both labor and materials can spike by 20-30% almost overnight. A job that might have cost $15,000 last month could easily be quoted at $18,000 or more after the storm. It’s not price gouging; it’s the reality of a strained market.

We’re seeing this play out right now. Moving into 2026, the cost for a full roof replacement after major hail is already up 15-25% from 2024 levels. That's pushing jobs for typical homes into the $9,500 to $46,000 range nationally.

The jump is especially sharp in areas that get hit often, where a complete tear-off on a standard-sized home can run anywhere from $9,000 to $28,000. As roofing pros explain in this deep dive into 2026 roofing costs, a huge part of that increase is labor, which now accounts for about 60% of the project’s total expense.

Knowing about these forces—the complex labor, material inflation, and post-storm demand—gives you the context you need. It helps you see past the sticker shock on an estimate and recognize the true value and skill required to get the job done right.

Navigating Your Insurance Claim for Hail Damage

Finding a roofer is one thing. Getting your insurance company to pay for the damage is another battle entirely. This is where things can get complicated, but understanding the rules of the game makes the whole process feel less overwhelming.

Your insurance policy is the playbook. It lays out exactly what’s covered, how much you’ll pay out-of-pocket, and how your insurer will calculate the value of your damaged roof. Let’s break down the key terms that will dictate how much you actually receive.

Decoding Your Insurance Policy

The language buried in your policy document determines the size of the check your insurer cuts. The two most critical concepts are Replacement Cost Value (RCV) and Actual Cash Value (ACV). They might sound similar, but the difference can mean thousands of dollars out of your pocket.

Replacement Cost Value (RCV): This is the policy you want. RCV pays the full amount to replace your damaged roof with brand-new materials of similar quality. There's no deduction for age or wear and tear. Think of it like trading in your 10-year-old hail-damaged car and getting the cash to buy this year's model.

Actual Cash Value (ACV): This is a much tougher pill to swallow. An ACV policy pays for the replacement cost minus depreciation. If your roof is 15 years old, the insurer calculates its remaining lifespan and pays you that depreciated value. You’re left to cover the rest of the cost for a new roof yourself.

Then there’s your deductible. This is simply the amount you have to pay before your insurance coverage kicks in. If your approved repair cost is $12,000 and your deductible is $2,000, you pay the first $2,000. The insurance company covers the remaining $10,000.

The Claims Journey From Start to Finish

The moment you suspect hail damage, the clock starts ticking. The claims process follows a predictable path, and knowing the steps is the best way to stay in control and avoid mistakes that could cost you. Your mission is simple: provide undeniable proof of damage.

Document Everything, Immediately: After the storm passes, grab your phone. Take clear pictures of hailstones next to a coin or ruler for scale. Then, photograph any visible damage to your roof, gutters, siding, and windows. Make a note of the storm's date and time.

Contact Your Insurer: Call your insurance company to report the damage and get a claim number. They will assign an adjuster to your case.

Get a Professional Inspection (Crucial Step): This is the most important move you can make. Before the insurance adjuster shows up, have a trusted, independent inspector perform a thorough assessment. Their detailed report becomes your unbiased evidence.

Meet the Adjuster: Be on-site when the insurance adjuster arrives for their inspection. Hand them a copy of your independent report. This ensures they see all the "functional damage," not just the obvious cosmetic issues.

Review the Settlement Offer: The insurer will send a settlement offer based on their adjuster’s findings. Compare it line-by-line against your independent report and contractor's estimate. If the numbers don't match, you now have the evidence to push back.

Thorough documentation is your most powerful tool. A claim backed by a professional inspection report with clear photos and precise measurements is much more likely to be approved quickly and for the correct amount.

This evidence-based approach takes the guesswork and arguments out of the equation. It gets the homeowner, contractor, and insurer all working from the same undisputed facts.

If you need help building that rock-solid case, professional insurance claims assistance ensures every detail is captured correctly. A well-documented claim moves faster, minimizes delays, and gets that new roof over your head sooner.

How Professional Inspections Ensure Accurate Estimates

After a hailstorm hits, your first move determines everything. A quick look from the driveway just won’t do—it’s the fastest route to an underpaid claim, surprise out-of-pocket expenses, and long, frustrating disputes with the insurance carrier. This is where your hail damage roof repair cost can spiral out of control.

A professional, third-party inspection isn't just a good idea; it's your most powerful tool. It’s the difference between guessing what’s broken and knowing with complete certainty. A certified inspector delivers an unbiased, evidence-based report that paves the way for a fair and efficient claims process.

Beyond a Surface-Level Check

A real inspection is a forensic analysis of the entire roof, not just a quick count of dents. An expert isn’t just looking for the obvious damage. They're hunting for the functional damage that truly compromises your roof's ability to shed water and keep the elements out.

This means knowing the difference between:

- Cosmetic Damage: Minor pockmarks or surface scrapes that look bad but don't actually break the shingle's seal.

- Functional Damage: The critical stuff—cracks, punctures, and "bruises" that fracture the shingle mat and destroy its watertight integrity, even if you can't see it from the ground.

It takes a trained eye to tell the difference between normal aging and legitimate storm damage. By methodically documenting every single impact, inspectors create a bulletproof scope of work that leaves no room for arguments. If you want to get ahead of the game, you can learn to spot the common signs of hail damage on a roof with our in-depth guide.

An inspector’s report becomes the single source of truth for the claim. It gets the homeowner, the contractor, and the insurance adjuster on the same page, ensuring the repair is funded correctly right from the start.

This alignment kills the all-too-common problem where a roofer's estimate and the insurer’s offer are thousands of dollars apart. The inspection report bridges that gap with cold, hard data.

Safely Inspecting Difficult Roofs

What about those tall, steep, or complex rooflines? They pose a serious challenge and a significant safety risk for anyone not properly equipped. A professional inspection service has the gear and the training to tackle these structures safely and thoroughly.

Our crews arrive with the right tools for high-risk jobs:

- Safety Harnesses and Ropes: Absolutely essential for preventing falls on steep pitches.

- Specialized Ladders and Lifts: To get to multi-story or complicated roof sections without issue.

- High-Resolution Cameras and Drones: For capturing crystal-clear images of hard-to-reach areas without putting anyone in harm's way.

Using the right equipment means inspectors can meticulously document every square foot of the roof, no matter the height or pitch. Damage on a steep dormer or a high ridge gets cataloged with the same precision as damage on a flat, walkable section. This exhaustive process guarantees a complete and accurate estimate, preventing costly surprises and ensuring your final hail damage roof repair cost is fully justified and covered.

When a hailstorm hits, the questions start piling up almost as fast as the dents. Homeowners are often left wondering what to do next and what it's all going to cost. Let's clear up the confusion and give you straight answers to the most common questions we hear about hail damage and the claims process.

How Long Do I Have to File a Hail Damage Claim?

Most insurance policies give you one year from the date of the storm to file a claim, but don't take that for granted. This deadline can change depending on your state and your specific policy.

The best advice? Report the damage the moment you suspect it's there. If you wait, you’re giving the insurance carrier a reason to push back. They might argue that any water leaks or mold that appeared months later were due to your delay, not the original storm. Acting fast and getting a professional inspection is how you protect yourself.

Will My Insurance Premium Go Up if I File a Hail Claim?

It’s the question every homeowner asks, and for a good reason. But here's the reality: filing a single claim for storm damage—what insurers call an "Act of God"—should not raise your individual premium. You didn't cause the hailstorm, so you generally won't be penalized for it.

Now, here’s the catch. If a massive storm causes widespread damage across your entire zip code, the insurer might raise rates for the whole area to cover their new level of risk. This rate hike is based on the location's risk profile, not your personal claims history.

A single "Act of God" claim for hail is unlikely to affect your individual rates. But if your entire area gets hit hard and often, everyone's premiums could eventually go up.

What Is the First Thing I Should Do After a Hailstorm?

Safety first. Always. Never climb on a wet or potentially unstable roof. Your first look should be from the ground, checking for obvious signs of trouble like big holes or entire sections of missing shingles. If you see water actively leaking into your home, your first call should be to a roofer for emergency tarping.

Once you know the immediate situation is stable, it's time to start documenting.

- Note the date and time the storm rolled through.

- Take photos of the hailstones. Place a coin or a ruler next to them for scale—this is critical evidence.

- Photograph all visible damage. Get pictures of your roof (from the ground), gutters, siding, windows, and anything else that took a hit.

With this initial evidence in hand, contact your insurance company to open a claim and get a claim number. Your very next call should be to schedule a professional roof inspection to get an expert assessment of what you're dealing with.

When you need a clear, unbiased assessment to move your claim forward, Fox Claims Consultants LLC provides the expert inspections that get you answers. Our detailed reports give you the hard data you need to ensure your repair is estimated correctly. Learn more at https://foxclaimsconsultants.com.

Leave a Reply